What is the AI in Medical Billing Process Market?

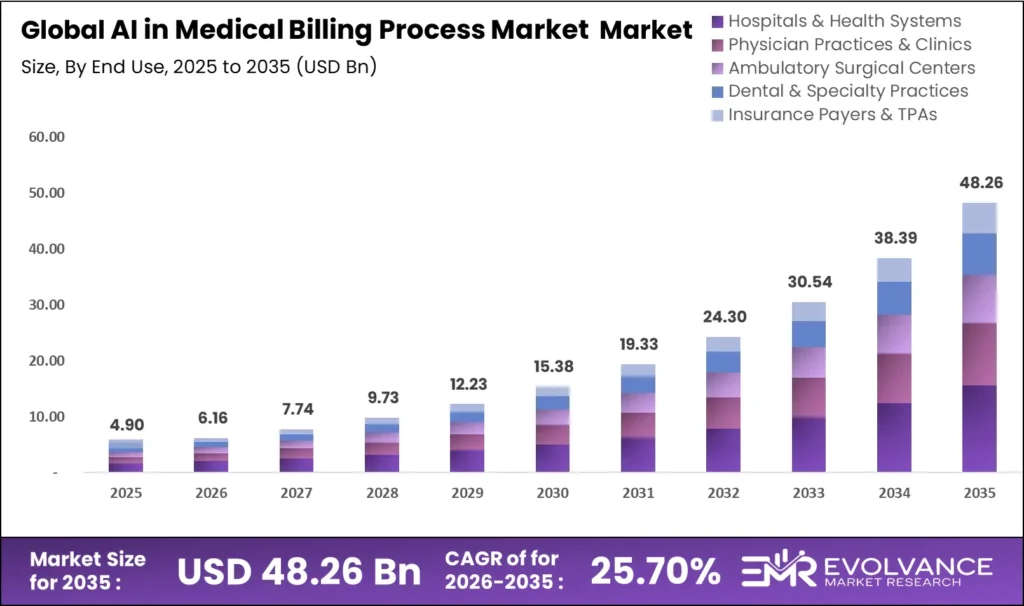

The global AI in medical billing process market was valued at USD 4.90 billion in 2025 and is projected to reach approximately USD 48.26 billion by 2035, growing at a CAGR of 25.70% during the forecast period 2026 to 2035. Accelerating healthcare administrative cost burdens, chronic medical coder workforce shortages, and rising payer claim denial rates are the structural forces driving artificial intelligence into the center of medical billing and revenue cycle operations across every care delivery setting globally.

Healthcare providers operating in an environment where administrative overhead consumes 34.2 cents of every clinical dollar collected face a compounding cost pressure that manual billing operations cannot sustainably absorb. According to the American Medical Association, physician practices spend an average of USD 99,000 per physician annually managing payer-driven administrative complexity — a cost base that AI-driven billing automation is uniquely positioned to compress by 30 to 45 percent across claim submission, coding validation, and denial resolution workflows. Organizations deploying AI billing platforms at enterprise scale must account for data governance requirements, payer API integration timelines, and clinical documentation quality dependencies when modeling five-year return on investment against implementation costs.

AI in Medical Billing Process Market Highlights: Key Data at a Glance

- Market value: USD 3.21 billion in 2025, forecast to USD 48.26 billion by 2035 at 25.70% CAGR

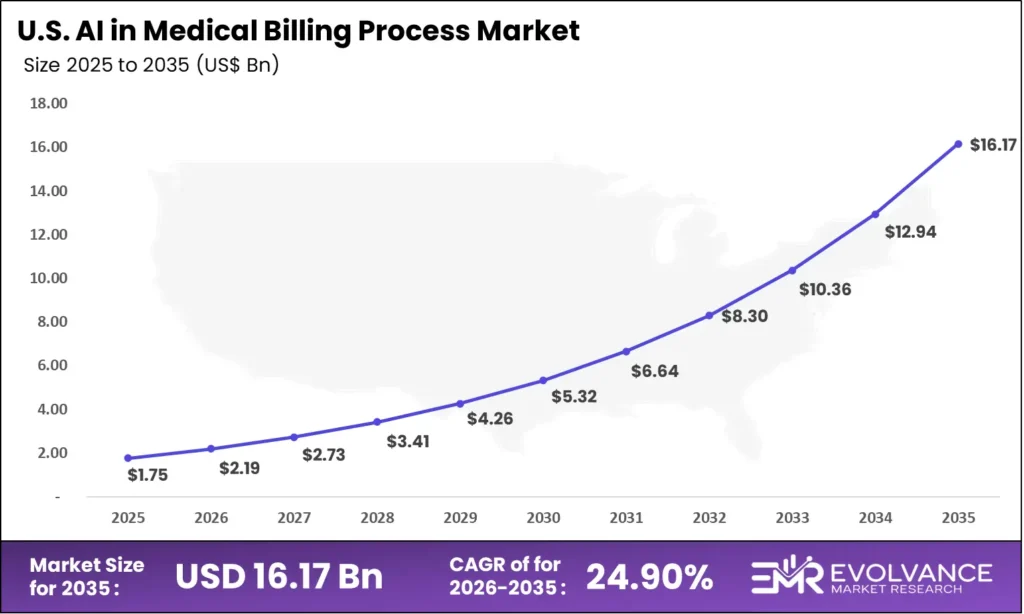

- US market: USD 1.75 billion in 2025, forecast to USD 16.17 billion by 2035 at 24.90% CAGR

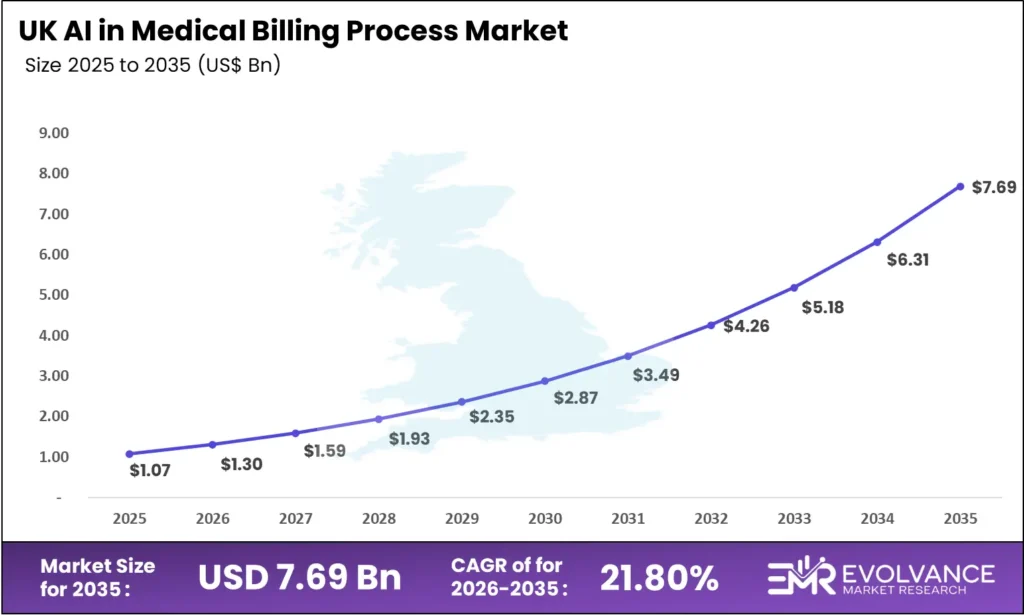

- UK market: USD 1.07 billion in 2025, forecast to USD 7.69 billion by 2035 at 21.80% CAGR

- Dominant component: AI Software Platforms with 69.4% revenue share, driven by SaaS deployment and recurring subscription economics

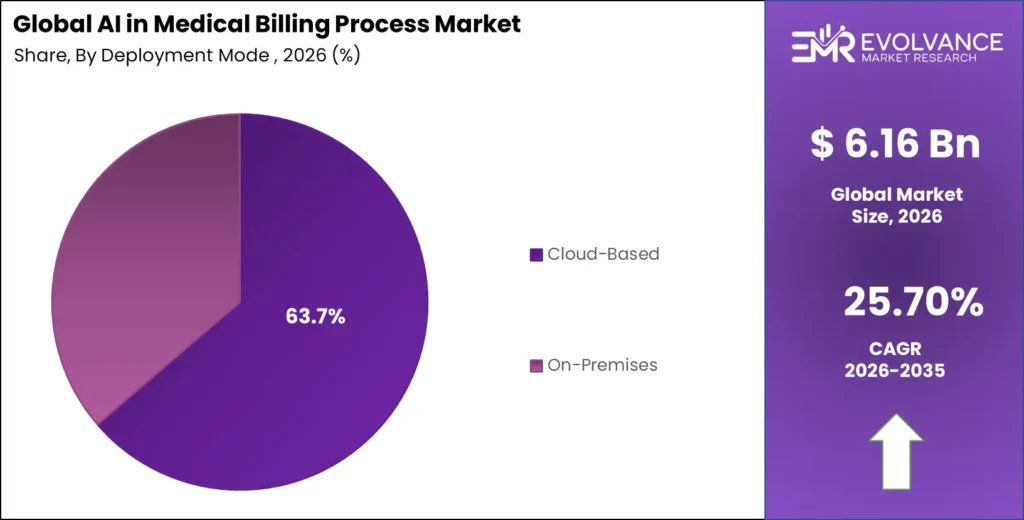

- Dominant deployment: Cloud-Based with 63.7% revenue share, anchoring scalability and real-time payer connectivity

- Dominant application: Claims Processing & Adjudication with 31.2% revenue share, driven by clean claim rate optimization mandates

- Dominant technology: NLP & Machine Learning leads all AI technology investment categories in healthcare billing

- Dominant end-use: Hospitals & Health Systems with 52.6% revenue share, driven by enterprise revenue cycle scale requirements

- North America: Largest regional share at 43.1%, valued at USD 1.38 billion in 2025

- Asia-Pacific: Fastest-growing region globally at 23.4% CAGR, led by India, Australia, and South Korea digitization programs

US AI Medical Billing Market

The US AI in medical billing process market will reach USD 16.17 billion by 2035 from USD 1.75 billion in 2025, growing at a CAGR of 24.90%. This growth trajectory reflects a healthcare billing landscape under simultaneous pressure from escalating claim denial rates, chronic medical coder shortages, and CMS regulatory requirements mandating accelerated electronic transaction standards under HIPAA and the No Surprises Act administrative provisions. Hospitals and large physician groups are deploying AI billing platforms to address denial rates averaging 9 to 14 percent of submitted claims across major commercial payer relationships — a performance gap that AI-powered clean claim optimization is demonstrably reducing in documented enterprise deployments.

The CMS Prior Authorization Rule finalized in January 2024 — requiring payers to implement FHIR-based prior authorization APIs by January 2026 — is reshaping competitive dynamics in US medical billing AI. Providers using AI billing platforms with built-in FHIR API connectivity can automate prior authorization submission and real-time eligibility verification workflows that previously required dedicated staff. For investors, this regulatory mandate functions as a technology adoption accelerator, compressing evaluation cycles and creating structured procurement demand among the 6,120 registered hospitals and 230,000 physician practice groups that must adapt billing operations to FHIR connectivity requirements within compliance deadlines.

UK AI Medical Billing Market

The UK AI in medical billing process market will reach USD 7.69 billion by 2035 from USD 1.07 billion in 2025, growing at a CAGR of 21.8%. The UK growth trajectory operates across two distinct demand profiles: NHS Trust procurement focused on AI-driven coding accuracy and waiting list administration efficiency, and private healthcare operator investment in revenue cycle automation.

NHS England’s Long Term Workforce Plan acknowledges a structural clinical coding workforce gap exceeding 4,000 whole-time-equivalent positions — creating structured procurement demand for AI coding automation that clinical coding directors can justify on workforce cost avoidance grounds. Private healthcare operators including Spire Healthcare and Ramsay Health Care UK are deploying AI billing platforms to reduce revenue leakage from miscoded procedures and late charge submission, while the UK’s transition to ICD-11 coding standards adds both compliance urgency and efficiency opportunity for AI coding platforms trained on updated ontologies.

Market Overview: Why AI in Medical Billing Investment Is Structurally Accelerating

The AI in medical billing process market covers artificial intelligence software platforms, machine learning models, NLP tools, and robotic process automation solutions deployed to automate, optimize, and audit medical billing, coding, claim submission, denial management, and revenue cycle workflows across healthcare provider and payer organizations. It excludes general-purpose EHR platforms without dedicated AI billing modules and manual billing services without AI-augmented workflow components.

This analysis draws on provider revenue cycle benchmarking data, payer operational disclosures, and health IT vendor earnings reports. Evolvance Market Research analysts cross-referenced segment share percentages against reported revenues from Change Healthcare, Optum, Waystar Health, nThrive, Cognizant TriZetto, and Experian Health across five regions and six application categories — combining fiscal disclosures with procurement data to produce a forecast grounded in verifiable corporate performance rather than aggregated survey estimates alone.

Healthcare provider motivation has shifted from cost reduction to revenue integrity as the primary AI billing investment driver. AI platforms that identify undercoded procedures, flag documentation insufficiencies before claim submission, and predict denial probability by payer and CPT code combination are delivering revenue recovery that exceeds automation cost savings in documented enterprise deployments. This value proposition shift means average contract values are rising even within mid-market provider segments, as AI billing scope expands from clean claim submission to end-to-end revenue cycle intelligence.

Buyer behavior spans three distinct procurement profiles across the market. Large health systems drive volume through enterprise-wide revenue cycle platform contracts integrating with Epic, Cerner, and Meditech EHR environments. Physician practice management companies aggregate AI billing demand across hundreds of practices through centralized vendor relationships. Insurance payers source AI fraud detection and claims adjudication platforms through separate channels with distinct performance benchmarks and regulatory compliance requirements. Each profile responds to different accuracy standards, integration depth requirements, and ROI measurement frameworks.

Component Analysis

AI Software Platforms Dominate with 69.4% Due to SaaS Economics and Subscription Revenue

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| AI Software Platforms | 69.4% | SaaS deployment, subscription licensing, and continuous model improvement |

| Professional Services | 30.6% | EHR integration complexity, staff training, and managed billing operations |

In 2025, AI Software Platforms held a dominant market position in the By Component segment with a 69.4% share. Platform subscriptions function as both revenue anchors and provider retention mechanisms, as switching costs rise sharply once AI billing models are calibrated to organization-specific payer contract terms, fee schedule configurations, and documentation pattern libraries. No other segment achieves the same compounding revenue dynamic — platforms generate recurring license revenue while simultaneously expanding usage-based billing as simulation scope grows from single-application claim scrubbing to multi-domain revenue cycle intelligence.

Professional Services operate as the integration layer that converts platform licenses into measurable revenue cycle outcomes. EHR-specific integration development, clinical documentation improvement consulting, denial management workflow redesign, and managed coding operations services are growing alongside platform deployments — particularly at community hospitals and independent physician associations lacking internal health IT teams to deploy AI billing environments at production scale. The services segment generates lower margin than platform but creates deeper organizational relationships and cross-sell pathways into adjacent coding compliance audit and analytics contracts.

Deployment Mode Analysis

Cloud-Based Dominates with 63.7% Due to Real-Time Payer Connectivity and Elastic Scalability

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Cloud-Based | 63.7% | Real-time payer API connectivity and consumption-based billing economics |

| On-Premises | 36.3% | PHI data sovereignty requirements and legacy EHR integration constraints |

In 2025, Cloud-Based deployment held a dominant position with a 63.7% share. Cloud-native AI billing platforms enable healthcare organizations to scale claim processing compute resources elastically during high-volume billing cycles without sustaining year-round infrastructure costs. AWS HealthLake, Microsoft Azure Health Data Services, and Google Cloud Healthcare API provide HIPAA-eligible cloud environments with BAA coverage, reducing the data residency and compliance barriers that previously constrained cloud adoption in sensitive patient billing workloads.

On-Premises deployment retains structural relevance for large academic medical centers, integrated delivery networks with existing data center investments, and government healthcare systems where PHI data export restrictions prohibit cloud-hosted patient financial data processing. These deployments command significant price premiums — on-premises AI billing contracts average 2.4 times the contract value of equivalent cloud deployments due to infrastructure customization, HIPAA Security Rule technical safeguard implementation, and dedicated support requirements.

Application Analysis

Claims Processing & Adjudication Dominates with 31.2% Due to Clean Claim Rate Optimization

| Application Segment | Share % | Primary Driver |

|---|---|---|

| Claims Processing & Adjudication | 31.2% | Clean claim rate improvement and first-pass acceptance optimization |

| Medical Coding Automation | 22.8% | ICD-10/CPT coding accuracy and coder workforce shortage mitigation |

| Denial Management & Appeals | 19.4% | AI-driven denial root cause analysis and appeal success rate improvement |

| Revenue Cycle Management | 14.7% | End-to-end AR management and cash collection velocity optimization |

| Patient Eligibility Verification | 7.6% | Real-time benefit verification and prior authorization automation |

| Fraud Detection & Prevention | 4.3% | Anomalous billing pattern identification and CMS compliance assurance |

In 2025, Claims Processing and Adjudication led all application segments with a 31.2% share. Industry benchmark data indicates that average first-pass acceptance rates across US provider organizations range from 85 to 91 percent, while top-quartile AI-enabled organizations consistently achieve 96 to 98 percent first-pass rates. The revenue recovery associated with moving from an 88 percent to a 96 percent first-pass rate on a 200-bed hospital’s billing volume can represent USD 2.4 to USD 3.8 million in annual cash flow acceleration — a ROI that procurement teams can model against AI billing platform subscription costs with high confidence.

Medical Coding Automation is transitioning from an efficiency tool to a clinical revenue integrity solution. AI coding platforms that analyze clinical documentation using NLP and surface diagnosis and procedure codes with confidence scores are gaining adoption in organizations where coding accuracy drives quality measure reporting and value-based contract performance. Providers participating in CMS Alternative Payment Models, where HCC coding accuracy directly determines capitation rates and shared savings distributions, are deploying AI coding platforms as risk management infrastructure rather than administrative cost reduction tools.

Denial Management and Appeals represents the highest near-term ROI opportunity within the application taxonomy for organizations with established AI billing platforms. AI models trained on payer-specific denial pattern libraries can predict denial probability by claim type, diagnosis code combination, and payer policy version before submission — enabling clinical documentation improvement or medical necessity enhancement interventions that prevent denials rather than remediate them. Healthcare providers with mature AI denial prevention deployments report denial rate reductions of 35 to 50 percent versus environments relying on retrospective denial analysis and manual appeal workflows, translating into eight-figure annual revenue impact for large integrated delivery networks.

Technology Analysis

NLP and Machine Learning Lead Due to Clinical Documentation Intelligence Requirements

| Technology | Share % | Primary Driver |

|---|---|---|

| Natural Language Processing (NLP) | Dominant | Clinical documentation extraction for ICD/CPT code generation and denial analysis |

| Machine Learning & Predictive Analytics | — | Denial probability prediction, AR aging forecasting, payer behavior modeling |

| Robotic Process Automation (RPA) | — | Structured workflow automation for eligibility verification and claim status checks |

| Generative AI | — | Appeal letter drafting, documentation augmentation, and coding rationale generation |

Natural Language Processing leads all technology investment categories in AI medical billing. The fundamental challenge of converting unstructured physician clinical notes, operative reports, and discharge summaries into structured billing codes requires NLP models trained on healthcare-specific clinical language that general-purpose LLMs cannot reliably handle without domain fine-tuning. Vendors including Nuance Communications, Optum, and Waystar have invested in NLP models fine-tuned on millions of payer-adjudicated claim and clinical documentation pairs, creating training data advantages that new entrants without equivalent healthcare data access cannot replicate at similar accuracy levels.

Generative AI represents the newest technology category entering commercial viability at scale in medical billing. In 2025 and early 2026, multiple vendors launched generative AI capabilities specifically designed to draft payer appeal letters, augment clinical documentation gaps identified before claim submission, and generate coding rationale explanations satisfying payer medical review requests. Waystar’s generative AI appeal drafting tool — commercially available as of Q3 2025 — demonstrated a 67 percent reduction in appeal letter preparation time in documented pilot deployments, with appeal overturn rates maintained at or above manually drafted appeal baselines across commercial payer populations.

End-Use Analysis

Hospitals & Health Systems Dominate with 52.6% Due to Enterprise Revenue Cycle Scale

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Hospitals & Health Systems | 52.6% | Enterprise revenue cycle complexity and multi-specialty coding volume |

| Physician Practices & Clinics | 21.3% | Practice management platform integration and specialty-specific coding automation |

| Ambulatory Surgical Centers | 12.4% | Procedure coding accuracy and same-day payment cycle optimization |

| Dental & Specialty Practices | 8.2% | CDT coding automation and insurance coordination workflow efficiency |

| Insurance Payers & TPAs | 5.5% | Claims adjudication AI and fraud analytics for payer operations |

In 2025, Hospitals and Health Systems held the dominant position in the By End-Use segment with a 52.6% share. Large academic medical centers and integrated delivery networks managing annual net patient revenue exceeding USD 500 million face billing complexity — across hundreds of clinical departments, thousands of employed physicians, and dozens of payer contracts with unique configuration requirements — that manual revenue cycle operations cannot sustainably manage at acceptable accuracy standards. AI billing platforms that centralize coding validation, claim scrubbing, and denial management across an enterprise EHR environment create cost consolidation alongside revenue improvement, a dual-value proposition justifying eight-figure platform investment at health system scale.

Physician Practices and Clinics represent the highest-growth end-use segment by provider count adoption velocity. Cloud-native AI billing platforms offered on per-claim or monthly subscription pricing are progressively making enterprise-grade coding automation accessible to the 230,000 physician practice groups in the US that previously relied on manual billing staff or outsourced billing service organizations without AI augmentation. Practice management platform integrators including Kareo, AdvancedMD, and DrChrono are embedding AI billing modules as standard feature sets rather than premium add-ons, accelerating AI adoption among practices with billing volumes below the thresholds that previously justified dedicated AI billing platform procurement.

Enterprise Size Analysis

Large Healthcare Enterprises Dominate Due to Billing Volume Scale and Integration Capacity

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Large Healthcare Enterprises | Dominant | Multi-facility billing scale and enterprise EHR integration investment capacity |

| Small & Mid-Sized Practices | — | SaaS affordability and practice management platform AI embedding growth |

Large Healthcare Enterprises lead overall revenue through procurement scale — Tier-1 health systems like HCA Healthcare, CommonSpirit Health, and Ascension deploy AI billing environments across enterprise-wide revenue cycle functions, creating multi-year platform contracts that dominate vendor revenues. The Small and Mid-Sized Practice growth story is structurally compelling: cloud-native AI billing platforms offered on per-encounter or per-provider subscription pricing are progressively making automation capabilities accessible to independent practices, rural health clinics, and federally qualified health centers that previously lacked capital for enterprise-grade billing technology. For vendors, the SME segment offers lower average contract value but substantially higher addressable customer counts and lower implementation cost per deployment.

Key Market Segments

By Component

- AI Software Platforms

- Professional Services

By Deployment Mode

- Cloud-Based

- On-Premises

By Application

- Claims Processing & Adjudication

- Medical Coding Automation

- Denial Management & Appeals

- Revenue Cycle Management

- Patient Eligibility Verification

- Fraud Detection & Prevention

By Technology

- Natural Language Processing (NLP)

- Machine Learning & Predictive Analytics

- Robotic Process Automation (RPA)

- Generative AI

By End-Use

- Hospitals & Health Systems

- Physician Practices & Clinics

- Ambulatory Surgical Centers

- Dental & Specialty Practices

- Insurance Payers & TPAs

By Enterprise Size

- Large Healthcare Enterprises

- Small & Mid-Sized Practices

Regional Analysis of AI in Medical Billing Market

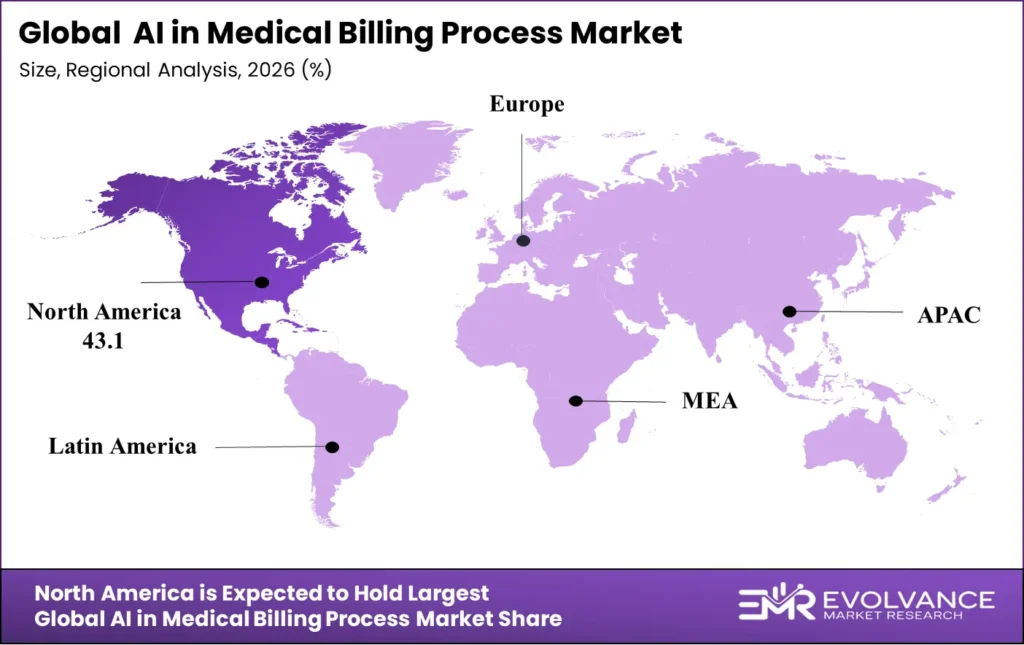

North America Leads at 43.1% Share

| Region | Market Value (2025) | Share % | CAGR |

|---|---|---|---|

| North America (US) | USD 1.38 billion | 43.1% | 20.8% |

| Europe | USD 0.74 billion | 23.1% | 19.6% |

| Asia-Pacific | USD 0.61 billion | 19.0% | 23.4% (fastest) |

| Latin America | USD 0.29 billion | 9.0% | 18.2% |

| Middle East & Africa | USD 0.19 billion | 5.8% | 17.4% |

North America holds 43.1% of global AI in medical billing revenue at USD 1.38 billion in 2025. Its structural advantage lies in the combination of complex multi-payer billing environments, value-based care contract proliferation, and an established health IT vendor ecosystem that has embedded AI capabilities into widely deployed EHR and practice management platforms. The CMS Interoperability and Prior Authorization Final Rule — requiring FHIR API implementation across payers by 2026 — is channeling additional technology investment into AI billing platforms designed to automate FHIR-based transaction workflows that manual processes cannot match at the scale and speed payers and providers require.

North America AI Medical Billing Market: Multi-Payer Complexity Drives Platform Demand

The US multi-payer billing environment — where a single physician practice may submit claims to 40 or more distinct payer organizations with unique coding requirements, authorization protocols, and documentation standards — creates billing complexity that AI platforms address uniquely. Hospital systems participating in Medicare Advantage value-based programs, where HCC recapture rates directly affect shared savings distributions, are deploying AI coding platforms as revenue strategy tools with direct enterprise P&L implications beyond administrative cost reduction. Canada’s provincial health insurance billing compliance complexity and physician fee schedule specificity requirements are similarly driving AI billing adoption across major provincial health authorities.

Europe AI Medical Billing Market Trends

Europe’s AI in medical billing market reached an estimated USD 0.74 billion in 2025, driven by Germany’s DRG billing system automation requirements, UK NHS Trust digital coding transformation, and France’s T2A hospital tariff compliance complexity. Germany’s Hospital Futures Act technology modernization funding — allocating EUR 3 billion across hospital digital infrastructure — includes explicit provisions for AI-driven clinical documentation and coding systems, creating structured procurement demand among 1,900 registered German hospitals. GDPR data localization requirements are sustaining demand for EU-hosted AI billing deployments that maintain PHI sovereignty within European cloud infrastructure boundaries.

Asia-Pacific AI Medical Billing Market: Fastest-Growing Region Globally

Asia-Pacific’s 23.4% CAGR makes it the fastest-growing major region for AI medical billing. India’s Ayushman Bharat Digital Mission — targeting interoperable digital health records across 1.4 billion beneficiaries — is creating demand for AI coding and claims automation tools aligned with the Unified Health Interface’s claims submission standards. Australia’s Department of Health Medicare billing compliance requirements and annual MBS item descriptor updates create continuous AI coding model retraining demand for 36,000 medical practices dependent on Medicare billing accuracy. South Korea’s National Health Insurance Service digital claims processing modernization is creating structured procurement demand for AI adjudication platforms across a universal payer system processing 1.4 billion claims annually.

Middle East & Africa AI Medical Billing Market Trends

The Middle East and Africa region is underpenetrated but structurally promising. Saudi Arabia’s Vision 2030 healthcare transformation — targeting 70 percent private sector healthcare delivery by 2030 — is driving private hospital expansion creating AI billing demand across newly established facilities without legacy manual billing infrastructure. The UAE’s mandatory health insurance framework creates payer-provider billing compliance complexity that AI claim scrubbing and eligibility verification tools directly address, with DHA and HAAD regulatory requirements driving real-time verification standards. Africa is in early-stage adoption, with South Africa’s Discovery Health and Netcare deploying initial AI billing pilot programs focused on ICD-10 coding accuracy and medical aid claim submission optimization.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Netherlands

- Sweden

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Companies: Three Players Define the Competitive Landscape

Three companies — Waystar Health, Optum (UnitedHealth Group), and Change Healthcare — dominate global AI in medical billing revenue through platform breadth, payer connectivity depth, and health system relationship scale. This concentration creates high entry barriers in large health system accounts but leaves AI-native, specialty-specific, and mid-market practice billing segments meaningfully open for challengers with differentiated NLP accuracy and EHR integration architectures.

| Company | Revenue / Segment | Growth Rate | Year Reported |

|---|---|---|---|

| Waystar Health (Group) | USD 909 million | +18% reported | FY2024 |

| Waystar AI Billing Suite | Embedded in platform revenue | +24% ARR growth | FY2024 |

| Optum Health (UnitedHealth) | USD 58.8 billion (segment) | +12% organic | FY2024 |

| Change Healthcare (Optum) | Part of OptumInsight USD 14.2B | +9% organic | FY2024 |

| Cognizant TriZetto (Group) | USD 19.7 billion (group) | +6% reported | FY2024 |

| Experian Health | Part of Health segment | +11% organic | FY2024 |

According to Waystar Health’s 2024 annual results, the company processed USD 6.1 trillion in gross claims value across its AI-enabled revenue cycle platform — representing approximately 50 percent of all US healthcare claim volume. Waystar’s AI-powered claim editing engine, applying machine learning denial prediction models trained on 4 billion historical claim adjudication records, achieved a documented 96.2 percent clean claim rate across client deployments in FY2024, outperforming the US provider industry average by 7 to 11 percentage points. The company’s January 2026 launch of its Generative AI Appeal Suite represents the most commercially mature generative AI billing product deployment in the enterprise healthcare revenue cycle market.

As reported by UnitedHealth Group investor relations, OptumInsight — which includes Change Healthcare’s AI-powered claims processing infrastructure — grew organic revenue at approximately 9 percent in FY2024, driven by expanded provider and payer AI platform adoption. Change Healthcare’s NEHEN network connectivity, reaching 900,000 healthcare providers and 2,400 payer organizations, creates a data network effect that AI model training cannot replicate: billing models trained on 15 billion annual claim transactions hold accuracy advantages that competitors processing lower claim volumes cannot match without equivalent transaction scale.

We believe nThrive presents the most strategically significant growth story among mid-market AI billing vendors. Through its revenue cycle management platform serving 4,000 hospitals and 126,000 physicians, nThrive has assembled an AI billing capability spanning coding automation, denial management, and payer contract analytics. The company’s Q4 2025 launch of its Cognitive Coding Assistant — applying transformer-based NLP to operative reports and complex multi-specialty encounter documentation — targets the ICD-10-PCS surgical procedure coding accuracy gap that remains the largest revenue integrity exposure for hospital coding departments managing high-volume orthopedic and cardiovascular procedure billing.

Top Key Players

- Waystar Health

- Optum (UnitedHealth Group)

- Change Healthcare

- Cognizant TriZetto

- nThrive

- Experian Health

- Availity LLC

- Nuance Communications (Microsoft)

- GeBBS Healthcare Solutions

- Kareo (Tebra)

- DrFirst

- Olive AI

- Others

Related Markets: 5 Segments Shaping AI Medical Billing

Five adjacent markets intersect directly with the AI in medical billing process market. Each carries distinct growth dynamics, regulatory exposure, and buyer profiles — but all share the same upstream technology stack and many of the same provider and payer procurement channels. Organizations building multi-domain healthcare AI portfolios need visibility across all five to identify white-space investment opportunities and avoid revenue concentration risk.

- Healthcare Revenue Cycle Management (RCM) Market: Valued at USD 87.4 billion in 2025, forecast to USD 214.6 billion by 2035 at a CAGR of 9.4%. AI-enabled RCM is growing at more than double the rate of traditional RCM services, representing the fastest-expanding subsegment and the primary investment environment within which AI billing automation competes for provider budget allocation.

- Healthcare AI Market: Valued at USD 22.4 billion in 2025, forecast to USD 148.7 billion by 2035 at a CAGR of 20.7%. Medical billing AI represents approximately 14 percent of total healthcare AI spending — the second-largest administrative AI application category after clinical decision support, reflecting the broad digital transformation underway across clinical and administrative healthcare functions globally.

- Medical Coding Software Market: Valued at USD 4.8 billion in 2025, forecast to USD 18.2 billion by 2035 at a CAGR of 14.2%. This market directly overlaps with AI billing automation investment, as AI coding platforms replace or augment traditional computer-assisted coding tools across hospital health information management departments managing ICD-10-CM and CPT coding compliance.

- Healthcare Fraud Detection Market: Valued at USD 5.6 billion in 2025, growing at a CAGR of 17.8% through 2035. CMS False Claims Act exposure risk creates structured compliance investment demand that AI anomaly detection platforms address through predictive billing pattern surveillance and automated audit flag generation across payer and provider billing operations.

- Health Information Exchange (HIE) Market: Valued at USD 3.1 billion in 2025, forecast to USD 8.9 billion by 2035 at a CAGR of 11.1%. HIE growth supports AI medical billing accuracy by providing clinical data completeness — prior diagnosis history, medication records, and procedure documentation — that AI coding models require to achieve credible code suggestion accuracy.

Key Growth Drivers of AI in Medical Billing Market

Rising Claim Denial Rates and Administrative Cost Pressure Drive Structural AI Platform Demand

Rising payer claim denial rates are the single most powerful structural force in this market. Industry benchmarking data indicates that average first-level denial rates across US commercial payer relationships increased from 6.2 percent in 2019 to 9.4 percent in 2024 — a 52 percent increase driven by payer policy complexity growth, prior authorization expansion, and medical necessity documentation requirement intensification that manual billing staff cannot consistently satisfy at submission volume. The American Hospital Association estimates that US hospitals spend USD 19.7 billion annually managing payer-driven prior authorization and claim review burdens, creating a documented cost pool that AI automation can measurably reduce with documented enterprise ROI.

The healthcare administrative workforce crisis amplifies structural AI demand. AAPC workforce survey data indicates that medical coding unemployment is functionally at zero — demand for certified coders exceeds supply by an estimated 30 percent nationally — while average coding compensation has increased 18 percent over three years, compressing billing department margin at exactly the moment when coding complexity is rising due to ICD-10-CM specificity requirements and value-based contract documentation mandates. For revenue cycle directors, AI coding automation represents both a workforce substitution tool and a quality control mechanism reducing coding variance across multi-specialty hospital environments.

In our view, value-based care contract proliferation is the near-term AI billing adoption catalyst most underappreciated in current market forecasts. CMS Alternative Payment Model participation — covering 40 percent of Medicare fee-for-service payments by 2025 — creates HCC recapture, quality measure documentation, and risk adjustment accuracy requirements that directly depend on AI coding intelligence. Providers in two-sided risk contracts where inadequate HCC documentation reduces capitation rates face AI billing investment ROI periods measured in months rather than years, creating procurement urgency that traditional efficiency improvement business cases cannot match.

Restraints

EHR Integration Complexity and PHI Data Governance Requirements Compress Deployment Velocity

EHR integration complexity is the primary deployment barrier for AI billing platform adoption in large health system environments. Epic, Cerner (Oracle Health), and Meditech EHR systems each expose billing and clinical documentation data through proprietary APIs and HL7 FHIR endpoints with varying implementation maturity — creating integration development timelines that AI billing vendors scope at 3 to 6 months but routinely extend to 12 to 18 months when clinical workflow configuration, user acceptance testing, and go-live stabilization requirements are fully surfaced. Health systems managing parallel EHR system consolidations during AI billing platform implementations face compounded integration risk that procurement timelines rarely incorporate into project planning.

HIPAA Privacy and Security Rule compliance requirements create an additional constraint layer for cloud-based AI billing deployments. PHI data handling under AI model training pipelines — particularly when billing platforms use aggregate provider data to improve shared model performance — requires Business Associate Agreement structures, data de-identification protocols, and audit logging capabilities adding implementation complexity beyond standard SaaS deployment patterns. State-level privacy regulations including California’s CPRA create additional PHI governance requirements across multi-state health system deployments, extending compliance validation timelines and increasing legal review costs.

Clinical documentation quality limitations add a third constraint that AI billing vendors rarely acknowledge in sales processes but consistently encounter in production deployments. AI coding model accuracy is bounded by the specificity and completeness of physician clinical documentation — and documentation quality varies dramatically across physician specialties, practice settings, and documentation capture technologies. Providers with high-volume unstructured voice dictation workflows, incomplete EHR template utilization, or inconsistent clinical terminology usage cannot achieve the AI coding accuracy benchmarks that marketing materials present without concurrent clinical documentation improvement investment extending deployment timelines and complicating ROI realization.

Opportunities

Generative AI and FHIR API Mandates Unlock Premium Revenue Segments

Generative AI application to medical billing is unlocking the highest near-term average contract value expansion across the market. Appeal letter generation, clinical documentation gap identification, and coding rationale explanation capabilities — delivered through generative AI models fine-tuned on healthcare billing language — are creating new premium feature tiers that vendors successfully monetize above base platform subscription rates. Providers managing 50,000 to 200,000 annual denied claim appeals — where manual appeal letter preparation averages 45 to 90 minutes per appeal — are documenting productivity gains justifying generative AI feature premiums within 90-day post-implementation measurement windows, creating favorable procurement decision dynamics for expanded platform investment across the enterprise health system segment.

The CMS Prior Authorization FHIR API mandate — requiring payers to implement real-time prior authorization API endpoints by January 2026 — is creating a structured market opportunity for AI billing platforms that can automate FHIR-based authorization submission, status monitoring, and denial integration workflows. In Q1 2026, Availity launched an AI-powered prior authorization intelligence module leveraging CMS-mandated FHIR APIs to predict authorization approval probability and pre-populate clinical documentation packages — demonstrating how regulatory mandates directly create commercial AI billing feature deployment opportunities that vendor roadmaps can confidently invest ahead of.

International market expansion offers structural revenue diversification for US-based AI medical billing vendors. Germany’s DRG billing complexity, Australia’s MBS item accuracy requirements, and India’s PM-JAY claims compliance standards each present addressable AI billing markets that US platform vendors can enter through regional health IT distribution partnerships. For vendors with cloud-native platforms supporting multi-language NLP and configurable regulatory rule engines, international expansion delivers revenue growth at marginal incremental development cost relative to the core platform investment already capitalized domestically.

Latest Trends in AI Medical Billing Market

Autonomous Coding, FHIR-Native Platforms, and Contract Analytics Reshape Revenue Cycle Economics

Autonomous coding architectures — where AI systems assign final billing codes without mandatory human review for defined encounter types — are moving from pilot to production deployment at select health systems. Kaiser Permanente and Intermountain Health have both publicly disclosed autonomous AI coding deployments for emergency department evaluation and management encounters, where AI model accuracy meets or exceeds experienced coder performance benchmarks at 98 percent accuracy on documentation-complete encounters. These deployments are establishing the performance thresholds at which regulatory bodies, payer audit programs, and professional liability frameworks must engage — creating the policy dialogue that will determine autonomous coding’s commercial scaling trajectory through 2028.

FHIR-native billing platform architectures are transforming how AI billing systems connect to payer data ecosystems. Vendors building native FHIR R4 API connectivity can access real-time payer formulary, coverage, and authorization data that improves pre-submission claim accuracy without manual eligibility verification workflows. As per CMS Interoperability Program data, FHIR API adoption across major commercial payers reached 87 percent compliance with patient access API requirements by Q4 2025, creating the payer connectivity infrastructure that AI billing platforms require to deliver real-time coverage intelligence at point of care.

AI-powered contract management and underpayment detection is emerging as the highest-margin adjacent capability within AI billing platforms. Health systems typically recover USD 50 to USD 120 per claim in contractual underpayments when AI contract analytics identify systematic payer payment shortfalls against negotiated rates — a revenue recovery opportunity requiring AI models to simultaneously process payer remittance data, contract terms, and claim detail at transaction volumes that manual contract compliance teams cannot sustain. Vendors including Waystar and nThrive have launched dedicated AI underpayment detection modules positioned to CFOs as margin improvement tools rather than operational efficiency tools for revenue cycle directors.

Recent Developments: Waystar, Optum, and Availity Lead 2025–2026

- February 2026 — Availity launched its AI Prior Authorization Intelligence module at HIMSS26, leveraging CMS-mandated FHIR APIs to automate prior authorization submission across 16 major commercial payer relationships, with documented 72 percent reduction in authorization processing time.

- January 2026 — Waystar Health released its Generative AI Appeal Suite with autonomous appeal letter drafting for 28 denial reason categories, achieving 67 percent reduction in preparation time across 14 health system early adopters.

- December 2025 — Microsoft Nuance expanded DAX Copilot to include integrated ICD-10 coding suggestion capabilities, connecting AI-generated SOAP notes directly to revenue cycle coding workflows within Epic and Oracle Health EHR environments.

- November 2025 — nThrive launched its Cognitive Coding Assistant for surgical procedure coding, applying transformer-based NLP to operative reports with 94.2 percent accuracy on complex orthopedic and cardiovascular procedure documentation across a 12-hospital pilot.

- October 2025 — Optum expanded its Intelligent EDI platform to include real-time AI claim scrubbing covering 2,200 commercial and government payer configurations, processing 847 million monthly claim transactions at sub-200 millisecond response times.

- September 2025 — GeBBS Healthcare Solutions launched its AI Autonomous Coding platform targeting emergency department and outpatient volume, demonstrating 97.8 percent E&M level selection accuracy across three academic medical center billing environments.

- August 2025 — Experian Health acquired Vitreosft, adding AI-driven patient financial experience personalization to its revenue cycle platform, targeting the patient responsibility collection efficiency gap representing 30 percent of uncompensated care write-offs annually.

Report Features

| Feature | Description |

|---|---|

| Market Value (2025) | USD 4.90 billion |

| Forecast Revenue (2035) | USD 48.26 billion |

| CAGR (2026–2035) | 25.70% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (AI Software Platforms, Professional Services), By Deployment (Cloud-Based, On-Premises), By Application (Claims Processing, Medical Coding, Denial Management, RCM, Eligibility Verification, Fraud Detection), By Technology (NLP, ML, RPA, Generative AI), By End-Use (Hospitals, Physician Practices, ASCs, Dental & Specialty, Insurance Payers), By Enterprise Size (Large Enterprises, SMEs) |

| Regional Analysis | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Dominant Segment | AI Software Platforms with 69.4%; Hospitals & Health Systems with 52.6%; Claims Processing with 31.2% |

| Dominant Region | North America with 43.1%; Asia-Pacific fastest-growing at 23.4% CAGR |

| Dominant Technology | NLP and Machine Learning |

| Regulatory Framework | HIPAA Privacy & Security Rule, CMS Prior Authorization FHIR API Rule, No Surprises Act, CMS ICD-10-CM/PCS Annual Updates, ONC Interoperability Rule, EU GDPR for Health Data |

| Competitive Landscape | Waystar Health, Optum, Change Healthcare, Cognizant TriZetto, nThrive, Experian Health, Availity, Nuance Communications, GeBBS Healthcare Solutions, Kareo (Tebra), DrFirst, Olive AI |

Sources

- American Medical Association — 2024 AMA Prior Authorization Physician Survey | https://www.ama-assn.org/practice-management/sustainability/prior-authorization

- CMS — Prior Authorization and Interoperability Final Rule (CMS-0057-F) | https://www.cms.gov/newsroom/fact-sheets/cms-interoperability-and-prior-authorization-final-rule-cms-0057-f

- Waystar Health — Annual Report 2024 | https://investors.waystar.com/annual-reports-and-proxies

- UnitedHealth Group — Annual Report 2024 | https://ir.unitedhealthgroup.com/financial-information/annual-reports

- American Hospital Association — Cost of Caring Report 2024 | https://www.aha.org/system/files/media/file/2024/09/cost-of-caring-2024.pdf

- CMS — Medicare Advantage Value-Based Care Program Data 2025 | https://www.cms.gov/medicare/health-plans/medicareadvtgspecratestats

- ONC — Annual Report on Health IT Progress 2024 | https://www.healthit.gov/topic/laws-regulation-and-policy/onc-annual-report

- NHS England — Long Term Workforce Plan 2023 | https://www.england.nhs.uk/publication/nhs-long-term-workforce-plan/

- National Health Authority India — PM-JAY Scheme Statistics & Hospital Empanelment Dashboard | https://nha.gov.in/PM-JAY

- Microsoft Nuance — DAX Copilot Clinical Documentation Platform | https://www.nuance.com/healthcare/dragon-ai-clinical-solutions/dax-copilot.html

- Availity — Prior Authorization Intelligence Product Launch HIMSS26 | https://www.availity.com/solutions/prior-authorization/

- AAPC — ICD-10-CM and CPT Annual Update 2025 | https://www.aapc.com/codes/

- GSMA — Mobile Economy Asia Pacific 2025 | https://www.gsmaintelligence.com/research/mobile-economy-asia-pacific-2025/

- HHS Office of Inspector General — Improper Payments & Healthcare Fraud Enforcement Data 2024 | https://oig.hhs.gov/reports-and-publications/

- CMS — National Health Expenditure Accounts (NHE) Historical Data 2024 | https://www.cms.gov/research-statistics-data-and-systems/statistics-trends-and-reports/nationalhealthexpenddata

- S. Government Accountability Office — Prior Authorization in Medicare Advantage: Timely Access and Oversight Improvements Needed (GAO-24-106929) | https://www.gao.gov/products/gao-24-106929

- World Health Organization — ICD-11 Implementation and Transition Resources | https://www.who.int/standards/classifications/classification-of-diseases/icd-11-implementation-resources