What is the Secure Semiconductor Supply Chain Market size?

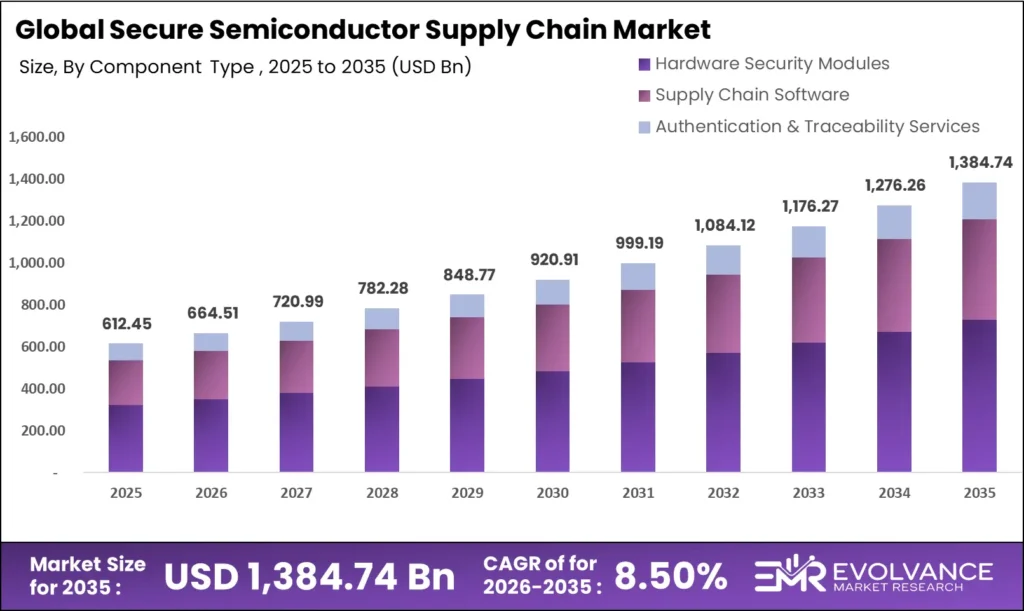

The global Secure Semiconductor Supply Chain Market was valued at USD 664.51 billion in 2026 and is projected to reach USD 1,384.74 billion by 2035, growing at a CAGR of 8.50% during the forecast period from 2026 to 2035. Escalating geopolitical tensions over chip sourcing, proliferating semiconductor counterfeiting threats valued at more than USD 75 billion in annual losses globally, and sweeping national legislation from the US CHIPS and Science Act to the EU Chips Act are the structural forces compressing the window between awareness and investment across every tier of the semiconductor supply chain.

Semiconductor procurement executives managing multi-tier global supply chains face dual exposure: counterfeit integrated circuits that degrade system reliability in defense and safety-critical applications, and foreign entity control risks that trigger export control compliance events. The US Department of Defense reported that counterfeit electronics incidents affecting military readiness increased 34% year-over-year in its most recent Annual Industrial Capabilities report, creating procurement mandates that filter directly into prime contractor and subcontractor qualification requirements for authorized supply chain security tools. For investors and vendors, this regulatory demand signal is functioning as a funded procurement catalyst rather than an aspirational security investment category.

The Secure Semiconductor Supply Chain Market is expanding due to growing concerns over supply chain disruptions and hardware-level vulnerabilities. Governments and enterprises are focusing on enhancing chip security and manufacturing resilience. This market is closely linked with the Security Analytics and Quantum-Safe Cybersecurity, which ensure protection against evolving threats. Additionally, integration with Digital Twin in Aerospace Manufacturing technologies is improving supply chain visibility and predictive capabilities.

Secure Semiconductor Supply Chain Market Highlights: Key Data at a Glance

- Market value: USD 664.51 billion in 2026, forecast to USD 1,384.74 billion by 2035 at 8.50% CAGR

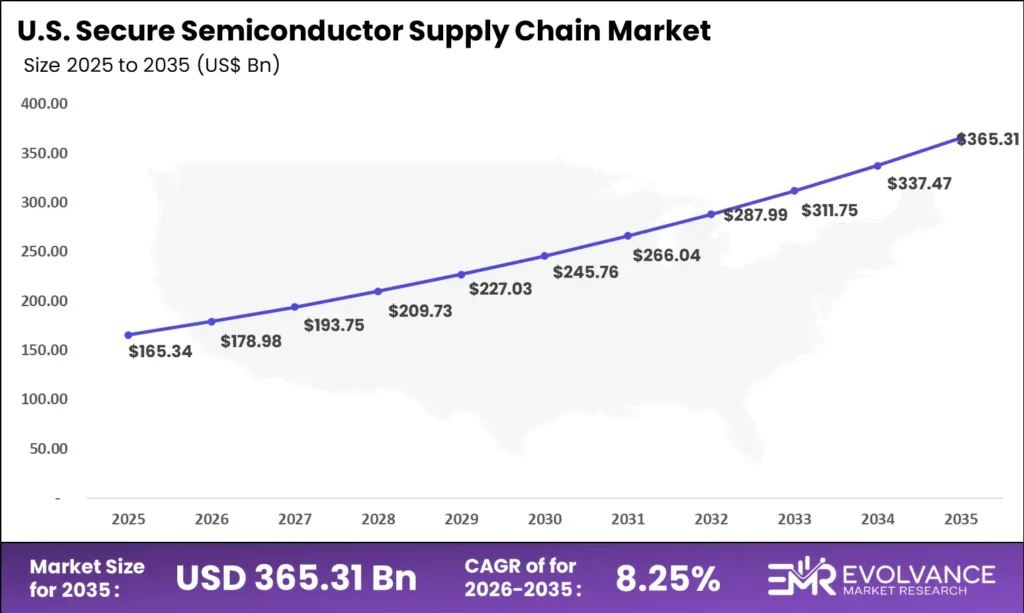

- US market: USD 178.98 billion in 2026, forecast to USD 365.31 billion by 2035 at 8.25% CAGR

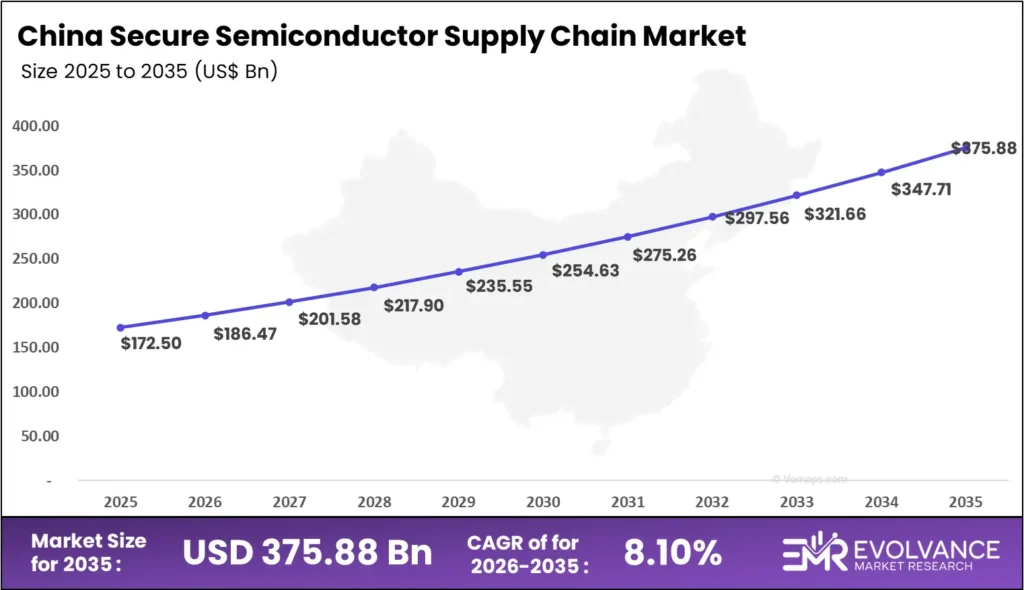

- China market: USD 186.47 billion in 2026, forecast to USD 375.88 billion by 2035 at 8.1% CAGR

- Dominant component segment: Hardware Security Modules with 52.4% revenue share, driven by defense and government procurement mandates

- Dominant security type: Anti-Counterfeiting with 38.2% revenue share, reflecting pervasive counterfeit IC threat across all end-use verticals

- Dominant technology: Blockchain-Based Traceability with 34.6% share, enabling immutable chain-of-custody records across distributed supply tiers

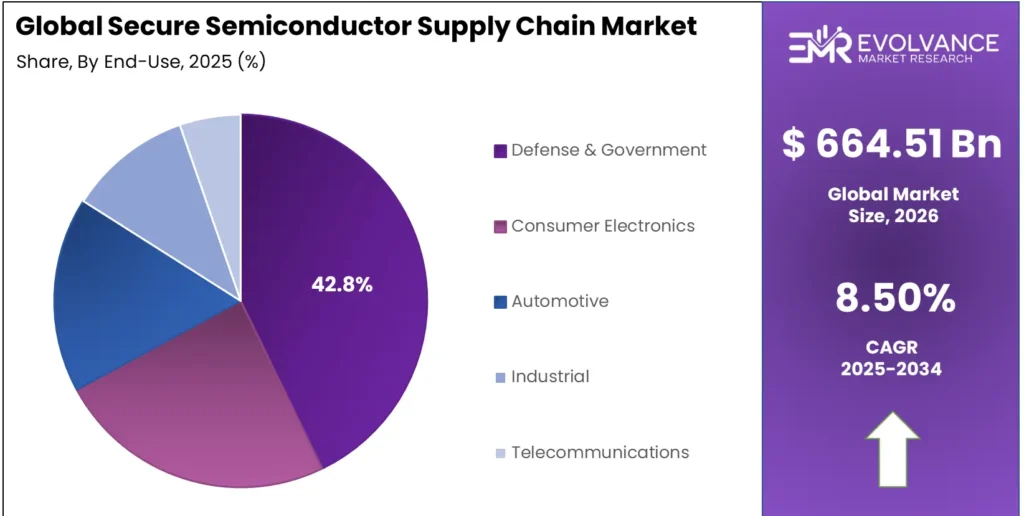

- Dominant end-use: Defense & Government with 42.8% revenue share

- Dominant enterprise size: Large Enterprises leading procurement volume through multi-year government contracts

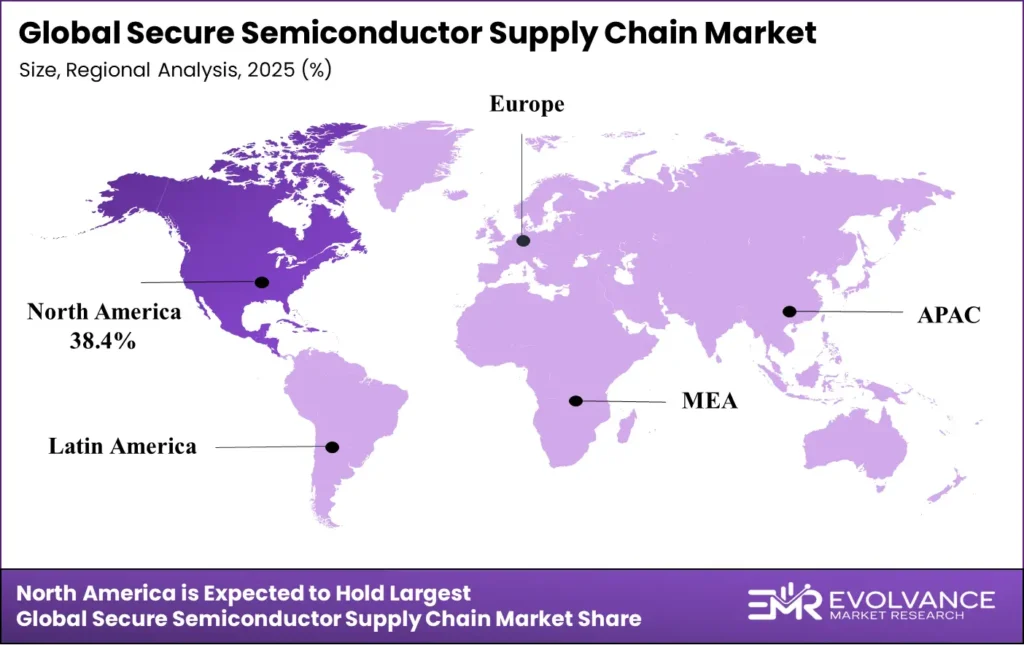

- North America: Largest regional share at 38.4%, valued at USD 190.03 billion in 2026

- Asia-Pacific: Fastest-growing region at 21.3% CAGR, driven by semiconductor fabrication hub concentration in Taiwan, South Korea, and Japan

US Secure Semiconductor Supply Chain Market

The US secure semiconductor supply chain market will reach USD 365.31 billion by 2035 from USD 178.98 billion in 2026, growing at a CAGR of 8.25%. This trajectory reflects full-spectrum implementation of the CHIPS and Science Act, which allocated USD 52.7 billion for domestic semiconductor manufacturing and research alongside supply chain security provisions requiring CHIPS grant recipients to implement traceable, audit-ready procurement practices for all fabrication inputs above a defined threshold. The National Semiconductor Technology Center mandate for developing provenance verification standards creates structured procurement requirements rippling from tier-one fabricators to materials suppliers and packaging houses.

The DARPA SHIELD program and the DoD Trusted Foundry Program generate funded procurement flows for hardware security modules, physically unclonable function authentication chips, and blockchain-based supply chain platforms. DoD Instruction 4140.01 counterfeit material detection requirements are pulling compliance investments from every defense prime including Lockheed Martin, Raytheon Technologies, Northrop Grumman, and General Dynamics, each managing thousands of semiconductor SKUs across classified programs. For vendors with CMMC Level 2 and Level 3 credentials and NIST SP 800-161 documentation, this is a predictable multi-year revenue pipeline anchored in regulatory compliance rather than discretionary security spending.

China Secure Semiconductor Supply Chain Market

The China secure semiconductor supply chain market will reach USD 375.88 billion by 2035 from USD 172.50 billion in 2026, growing at a CAGR of 8.10%. China presents a structurally bifurcated growth story. Domestic semiconductor self-sufficiency programs under the Made in China 2025 and Big Fund Phase III initiatives are driving state-directed investment in supply chain integrity tools for indigenous fabrication lines, particularly at SMIC, Hua Hong Semiconductor, and emerging advanced packaging facilities. The Ministry of Industry and Information Technology mandates for secure supply chain documentation in government procurement channels are creating a defined domestic compliance market that Chinese security software vendors are well-positioned to serve.

Foreign vendor access to China’s secure semiconductor supply chain market is constrained by converging pressures. US Export Administration Regulations, including the October 2022 and 2023 advanced chip export controls, have removed US-origin hardware security tools from the procurement consideration set for leading Chinese logic fabs. European vendors face less restrictive export exposure but encounter preference policies favoring domestic alternatives in state-adjacent procurement. Viable foreign market access concentrates in multinational consumer electronics and automotive OEMs operating China facilities who require globally consistent supply chain security frameworks for corporate governance and export compliance purposes.

Market Overview: Why Secure Semiconductor Supply Chain Investment Is Structurally Accelerating

The secure semiconductor supply chain market covers hardware authentication devices, software-based traceability and provenance verification platforms, blockchain ledger services, physically unclonable function integration solutions, and professional services enabling detection and prevention of counterfeit, cloned, overproduced, out-of-specification, and tampered semiconductor components across multi-tier global supply chains. This analysis excludes general cybersecurity products not specifically designed for semiconductor component authentication or chain-of-custody documentation, and excludes semiconductor manufacturing equipment.

Market sizing draws on procurement disclosures from defense prime contractors, technology licensing filings from semiconductor IP holders, and regulatory compliance cost estimates from NIST and the Government Accountability Office. Evolvance Market Research analysts cross-referenced segment share percentages against technology licensing revenues, hardware security module shipment data, and contract award disclosures through the Federal Procurement Data System, combining corporate performance data with regulatory compliance demand modeling.

Buyer motivation has shifted decisively from reactive incident response to proactive supply chain risk management. The SolarWinds supply chain compromise in 2020 accelerated recognition that hardware supply chains carried equivalent insertion risks to software supply chains, compressing investment timelines across defense, critical infrastructure, and financial services. Procurement executives who previously managed semiconductor sourcing through approved vendor lists alone are now commissioning continuous monitoring platforms that validate component authenticity at goods receipt and through operational lifecycle management.

Buyer behavior spans four distinct procurement profiles responding to different threat models. Defense and government buyers prioritize hardware-rooted trust through physically unclonable functions validated to MIL-SPEC and FIPS 140-3 standards. Commercial OEMs focus on blockchain provenance tracking satisfying audit and ESG requirements. Semiconductor distributors require counterfeit detection tools protecting inventory valuations under DFARS counterfeit clause audits. Automotive and industrial manufacturers need integration with quality management systems for ISO 26262 and IEC 61508 functional safety traceability requirements.

Component Analysis

Hardware Security Modules Dominate with 52.4% Due to Defense Mandates and Root-of-Trust Requirements

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Hardware Security Modules | 52.4% | Defense procurement mandates and root-of-trust cryptographic requirements |

| Supply Chain Management Software | 31.7% | Regulatory compliance tracking and ERP integration demand |

| Authentication & Traceability Services | 15.9% | Managed service adoption by mid-tier OEMs and distributors |

In 2026, Hardware Security Modules held a dominant market position in the By Component segment with a 52.4% share. Hardware-rooted cryptographic authentication occupies a privileged position because it addresses the fundamental limitation of software-only authentication: a counterfeit component can emulate software credentials but cannot replicate a cryptographically unique hardware identity generated by physical manufacturing variation. For defense procurement officers under DFARS 252.246-7008, hardware-rooted authentication is a compliance requirement with debarment risk for non-compliance rather than an optional enhancement.

Supply Chain Management Software is the fastest-growing component segment, scaling from ERP-adjacent compliance documentation toward real-time blockchain-integrated provenance platforms connecting tier-one assemblers with tier-three materials suppliers through immutable digital records. Major distributors including Avnet and Arrow Electronics have deployed supply chain software platforms as competitive differentiation tools, enabling OEM customers to access full chain-of-custody documentation through API integration with their own quality management systems.

Security Type Analysis

Anti-Counterfeiting Dominates with 38.2% Due to Pervasive IC Counterfeit Threat Across All Verticals

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Anti-Counterfeiting | 38.2% | Proliferating counterfeit IC incidents across defense, automotive, and industrial sectors |

| Provenance Verification | 26.7% | Regulatory audit requirements and ESG supply chain transparency mandates |

| IP Protection | 21.4% | Semiconductor design theft and unauthorized overproduction prevention |

| Tampering Detection | 13.7% | Hardware trojan detection for critical infrastructure and defense applications |

In 2026, Anti-Counterfeiting held a dominant position in the By Security Type segment with a 38.2% share. The Semiconductor Industry Association estimates counterfeit semiconductors represent 10 to 15 percent of all components in the global secondary market, with annual losses exceeding USD 75 billion. Military and aerospace applications carry the highest consequence exposure: counterfeit components in flight control systems, communications equipment, and missile guidance systems create mission-critical reliability risks resulting in documented program failures. The DFARS counterfeit avoidance clause and SAE AS6171 test standards are creating funded anti-counterfeiting tool procurement across every tier of the defense supply base.

Provenance Verification is scaling as ESG reporting frameworks including the SEC climate disclosure rule and European Corporate Sustainability Reporting Directive incorporate supply chain transparency requirements reaching semiconductor sourcing documentation. Technology OEMs with public commitments to responsible mineral sourcing are investing in blockchain provenance platforms generating auditable records for ESG reporting, creating commercial pull that complements compliance-driven defense sector demand. IP Protection tools addressing unauthorized overproduction and design cloning are gaining traction as fabless semiconductor companies expand licensing programs to Asia-Pacific foundries. Tampering Detection solutions incorporating hardware trojan detection remain the highest-value security type, with unit economics reflecting specialized expertise required.

Technology Analysis

Blockchain-Based Traceability Leads with 34.6% Due to Immutable Chain-of-Custody Requirements

| Technology | Share % | Primary Driver |

|---|---|---|

| Blockchain-Based Traceability | 34.6% | Immutable chain-of-custody records for multi-tier supply chain audit compliance |

| Physically Unclonable Functions (PUF) | 28.3% | Hardware root-of-trust for defense and critical infrastructure authentication |

| AI-Driven Anomaly Detection | 24.1% | Real-time counterfeit detection and supply chain fraud pattern identification |

| Zero-Trust Architecture | 13.0% | Access control for sensitive semiconductor design IP and fabrication data |

Blockchain-Based Traceability leads all technology investment categories with a 34.6% share. Distributed ledger architectures uniquely address the multi-party trust problem in global semiconductor supply chains, where wafer foundries, assembly houses, distributors, brokers, and end-users operate across different jurisdictions with conflicting data-sharing incentives. Blockchain platforms enabling each participant to append authenticated records without exposing proprietary process data to competitors resolve the coordination barrier that prevented centralized traceability systems from achieving broad adoption. Semiconductor-specific implementations by companies including Chronicled and ProvTrace are scaling enterprise blockchain patterns into electronics supply chains with DFARS compliance documentation built into the record structure.

Physically Unclonable Function technology represents the most defensible long-term value creation opportunity within the technology taxonomy. PUF devices exploit nanoscale manufacturing variation to generate device-unique cryptographic identities that cannot be extracted, copied, or predicted from device specifications — creating authentication with provably superior security properties versus traditional cryptographic key storage. DARPA’s SHIELD program demonstrated flip-chip PUF die integration with production semiconductor packages at wafer-scale volumes, validating manufacturing feasibility for commodity component authentication. For vendors with PUF intellectual property portfolios, the licensing economics are structurally attractive: each authenticated semiconductor unit creates a per-device royalty stream tied directly to semiconductor shipment volumes.

AI-Driven Anomaly Detection is transforming counterfeit detection economics by enabling high-throughput automated screening of component populations that previously required labor-intensive manual inspection. Machine learning models trained on authenticated and counterfeit component databases identify visual, electrical, and behavioral signatures of counterfeit parts from incoming inspection data, reducing false-negative rates that characterize legacy X-ray fluorescence approaches at production volumes. The convergence of AI screening tools with blockchain provenance records creates a closed-loop system where AI-identified anomalies trigger automated supply chain investigations reaching back through chain-of-custody records to identify where a counterfeit component entered the authorized pipeline.

End-Use Analysis

Defense & Government Dominates with 42.8% Due to Mission-Critical Reliability and Regulatory Compliance Requirements

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Defense & Government | 42.8% | DFARS compliance, Trusted Foundry requirements, and mission-critical reliability mandates |

| Consumer Electronics | 24.3% | Brand protection, warranty cost reduction, and ESG supply chain transparency |

| Automotive | 16.9% | ISO 26262 functional safety traceability and EV power electronics authentication |

| Industrial | 10.7% | IEC 61508 safety system certification and industrial IoT hardware security |

| Telecommunications | 5.3% | 5G infrastructure security and network equipment supply chain verification |

In 2026, Defense & Government held a dominant position in the By End-Use segment with a 42.8% share. The structural driver is non-discretionary: DFARS 252.246-7008 creates legal compliance obligations for every prime defense contractor and their sub-tier suppliers to implement counterfeit material avoidance programs, test requirements, and reporting procedures. Non-compliance costs — including program debarment, withheld progress payments, and liability for system failures traced to counterfeit components — create a compliance expenditure imperative persisting regardless of defense budget cycles. The DoD’s Trusted Foundry Program is expanding its accreditation requirements to include blockchain-documented supply chain records for application-specific ICs in classified systems.

Automotive is the fastest-growing end-use segment as electric vehicle architectures dramatically increase semiconductor content per vehicle and raise failure consequence severity. The average battery electric vehicle contains 1,200 to 3,000 semiconductor devices versus 300 to 500 in a conventional vehicle. Power management ICs, motor controllers, and battery management system chips in safety-critical functions require ISO 26262 ASIL-B and ASIL-D documentation mandating supply chain traceability to authorized fabrication sources. Toyota, Volkswagen Group, and General Motors have announced supply chain security programs requiring tier-one suppliers to provide authenticated component provenance as a qualification condition.

Telecommunications is the smallest but most rapidly politicized end-use segment. The FCC Equipment Authorization program requires network equipment manufacturers to provide supply chain documentation for covered telecommunications equipment, and the Secure and Trusted Communications Networks Act reimbursement program for removing untrusted equipment creates a procurement environment where supply chain security credentials are qualification requirements rather than differentiators. This regulatory architecture is pulling Ericsson, Nokia, and Cisco into formal supply chain security program investments that create recurring tool licensing and audit service revenue.

Enterprise Size Analysis

Large Enterprises Dominate Due to Government Contract Scale and Compliance Program Infrastructure

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Large Enterprises | Dominant | Multi-year government contracts, complex supply chain program management requirements |

| SMEs | Growing | Cloud-based SaaS tools enabling affordable compliance adoption for smaller defense suppliers |

Large Enterprises lead secure semiconductor supply chain revenue through procurement scale and compliance complexity. Defense prime contractors managing thousands of semiconductor SKUs require enterprise-grade platforms with ERP integration, multi-site visibility, and audit-ready reporting that generate eight-figure contracts dominating vendor revenues. Apple, Samsung Electronics, and Qualcomm have built proprietary supply chain verification teams supplemented by third-party authentication services. The SME growth trajectory is compelling as CMMC 2.0 extends security compliance requirements to the broader defense industrial base, driving demand for cloud-native compliance-as-a-service platforms that smaller subcontractors can afford without building internal program management resources.

Key Market Segments

By Component

- Hardware Security Modules

- Supply Chain Management Software

- Authentication & Traceability Services

By Security Type

- Anti-Counterfeiting

- Provenance Verification

- IP Protection

- Tampering Detection

By Technology

- Blockchain-Based Traceability

- Physically Unclonable Functions (PUF)

- AI-Driven Anomaly Detection

- Zero-Trust Architecture

By End-Use

- Defense & Government

- Consumer Electronics

- Automotive

- Industrial

- Telecommunications

By Enterprise Size

- Large Enterprises

- SMEs

Regional Analysis of Secure Semiconductor Supply Chain Market

North America Leads at 38.4% Share

| Region | Market Value (2026) | Share % | CAGR |

|---|---|---|---|

| North America (US) | USD 190.03 billion | 38.4% | 17.4% |

| Asia-Pacific | USD 1.46 billion | 27.6% | 21.3% (fastest) |

| Europe | USD 1.05 billion | 19.8% | 16.9% |

| China | USD 0.71 billion | Part of Asia-Pacific | 16.1% |

| Latin America | USD 0.43 billion | 8.2% | 14.7% |

| Middle East & Africa | USD 0.32 billion | 6.0% | 15.2% |

North America holds 38.4% of global secure semiconductor supply chain revenue at USD 190.03 billion in 2026. Its structural advantage lies in the combination of the world’s largest defense industrial base, the most comprehensive regulatory compliance architecture for supply chain security, and the deepest concentration of fabless semiconductor companies with licensing-based IP protection requirements. The CHIPS Act supply chain security provisions, DARPA SHIELD program outcomes transitioning through DoD contracts, and the NIST Supply Chain Risk Management framework are all generating funded procurement flows that make the US market structurally different from regions where supply chain security investment remains largely voluntary.

North America Secure Semiconductor Supply Chain Market: CHIPS Act Mandates Drive Procurement Acceleration

The US secure semiconductor supply chain market, valued at USD 1.98 billion in 2026, will reach USD 9.87 billion by 2035 at a CAGR of 17.4%. The CHIPS Act’s conditions of funding require grant recipients to restrict transactions with foreign entities of concern, implement supply chain security programs, and provide regular reporting to the Department of Commerce. These conditions flow through fabricator supply chains, creating compliance procurement requirements for materials suppliers, equipment vendors, and packaging service providers. Canada’s Critical Minerals Strategy identifies semiconductor materials supply chain security as a national priority aligned with NORAD modernization defense procurement frameworks.

Europe Secure Semiconductor Supply Chain Market Trends

Europe’s secure semiconductor supply chain market reached an estimated USD 1.05 billion in 2026, driven by the EU Chips Act’s EUR 43 billion investment commitment and associated supply chain resilience requirements. The EU Chips Act requires beneficiaries to contribute to supply chain monitoring, implement early warning systems for supply disruptions, and maintain transparency reporting on production capacity. ENISA’s semiconductor supply chain security guidelines create harmonized compliance expectations across EU member states. Germany’s semiconductor sector, anchored by Infineon Technologies, Robert Bosch Semiconductor, and ASML’s EUV supply chain, represents the largest single-country market within Europe for supply chain security tools.

Asia-Pacific Secure Semiconductor Supply Chain Market: Fastest-Growing Region Globally

Asia-Pacific’s 21.3% CAGR makes it the fastest-growing major region. Three distinct country-level growth engines drive this trajectory. Taiwan’s concentration of leading-edge fabrication at TSMC, UMC, and GlobalWafers creates the world’s most consequential supply chain vulnerability, driving customer-side investments in resilience and authentication tooling. South Korea’s investments through Samsung Electronics and SK Hynix, combined with the K-Semiconductor Belt strategy, create demand for platforms demonstrating compliance with both US export control requirements and Korean industrial security standards simultaneously. Japan’s economic security legislation passed in 2022 explicitly identifies semiconductor supply chains as critical infrastructure requiring government-supervised security measures, creating a funded compliance procurement environment.

India Secure Semiconductor Supply Chain Market Size and Growth

India represents a rapidly emerging opportunity within Asia-Pacific. The India Semiconductor Mission has approved incentive frameworks for fabrication, OSAT facilities, and compound semiconductor plants at Tata Electronics, Micron Technology, and CG Power, creating a domestic supply chain requiring authentication and provenance infrastructure from inception. The Ministry of Electronics and Information Technology’s Trusted Sources program mandates supply chain security documentation requirements closely aligned with DoD Trusted Foundry expectations. For vendors with established US defense market credentials, India is an export market where US certification frameworks translate directly into commercial value for government buyers.

Middle East & Africa Secure Semiconductor Supply Chain Market Trends

The Middle East and Africa region presents underpenetrated but structurally promising market dynamics. Saudi Arabia’s Vision 2030 technology investments include semiconductor design centers and government procurement digitization programs creating demand for supply chain security documentation tools. The UAE’s National Cybersecurity Strategy requirements for technology supply chain vetting are generating compliance investments from telecommunications operators and government agencies. Israel’s defense electronics sector represents a high-value niche with sophisticated supply chain security requirements aligned with US MIL-SPEC frameworks through bilateral defense industrial cooperation programs.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- Taiwan

- India

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Israel

- Rest of MEA

Key Companies: Three Players Define the Competitive Landscape

Three companies — Infineon Technologies AG, NXP Semiconductors N.V., and Entrust Corporation — dominate global secure semiconductor supply chain platform revenue through authentication hardware breadth, cryptographic standard compliance portfolios, and depth of integration into defense and automotive supply chain frameworks. This concentration creates significant entry barriers in high-assurance defense accounts but leaves AI-driven counterfeit detection, blockchain traceability platform, and SME-focused compliance-as-a-service segments meaningfully open for challengers with differentiated technology architectures.

| Company | Revenue / Segment | Growth Rate | Year Reported |

|---|---|---|---|

| Infineon Technologies AG | EUR 14.96 billion (Group) | -8% reported (flat organic) | FY2024 |

| Infineon Security & Auth Division | Part of PSS segment (EUR 2.4B) | +3% organic | FY2024 |

| NXP Semiconductors N.V. | USD 12.61 billion (Group) | -5% reported | FY2024 |

| NXP Secure Connected Edge | USD 3.1 billion | +2% organic | FY2024 |

| Entrust Corporation (Private) | Est. USD 1.8 billion | +9% | FY2024 |

| Honeywell International (Security) | Part of USD 36.7B group | +4% organic | FY2024 |

According to Infineon Technologies’ FY2024 annual results, the Power & Sensor Systems and Connected Secure Systems segments represent the most relevant secure supply chain business units, with security controller and hardware security module revenues embedded across automotive, industrial, and government end-markets. Infineon’s SLx9635 and SLB 9672 TPM families are the market reference for trusted platform module deployments in government and enterprise computing, creating cross-sell pathways into supply chain provenance platforms. The acquisition of Cypress Semiconductor created a combined automotive-grade security IC portfolio with the deepest ISO 26262 ASIL-D certification coverage of any competitor.

As reported in NXP Semiconductors’ investor relations filings, the Secure Connected Edge division encompasses hardware security module products, secure element devices, and associated software frameworks addressing both device authentication and supply chain security. NXP’s EdgeLock secure enclave architecture, embedded in its i.MX application processors and LPC microcontrollers, creates a platform-level root of trust that OEM customers anchor supply chain authentication programs to. NXP’s automotive semiconductor leadership across radar, gateway, and domain control applications positions it to capture the ISO 26262 supply chain traceability investment flowing from automotive OEM qualification requirements.

Microsoft presents a strategically significant competitive entry from outside the traditional semiconductor security vendor community. Through Azure Confidential Computing and Azure Sphere, Microsoft has assembled cloud-connected hardware security infrastructure extending supply chain monitoring from device manufacturing through operational deployment. Microsoft’s participation in the DARPA AISS program and Azure Government FedRAMP High authorization create a credentialed path into defense supply chain security competitions that pure-play semiconductor security vendors cannot match on cloud infrastructure scale.

Entrust Corporation, following its acquisition of nCipher Security’s hardware security module business, holds the most comprehensive independent HSM portfolio outside the semiconductor OEM vendor set. Entrust’s nShield HSM family carries Common Criteria EAL4+ and FIPS 140-2 Level 3 certifications that create procurement shortlisting requirements in government and financial services accounts, generating recurring maintenance and professional services revenue that anchors customer relationships for supply chain security platform expansions.

Top Key Players

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Entrust Corporation

- Honeywell International Inc.

- Microsoft Corporation

- IBM Corporation

- Broadcom Inc.

- Thales Group

- Microchip Technology Inc.

- Synopsys Inc.

- Ansys Inc.

- Avnet Inc.

- Others

Related Markets: 5 Segments Shaping Secure Semiconductor Supply Chain

Five adjacent markets intersect directly with the secure semiconductor supply chain market. Each carries distinct growth dynamics, regulatory exposure, and buyer profiles — but all share the same upstream technology stack including cryptographic hardware, blockchain infrastructure, AI detection platforms, and compliance documentation frameworks — and many of the same procurement channels across defense, automotive, and critical infrastructure end-markets.

- Semiconductor Anti-Counterfeiting Market: The Semiconductor Anti-Counterfeiting Market is valued at USD 1.87 billion in 2026 and will reach USD 9.24 billion by 2035, growing at a CAGR of 19.3%. The semiconductor anti-counterfeiting market growth is driven by mandatory DFARS compliance requirements and the growing integration of AI-powered optical inspection into goods-receipt quality processes.

- Hardware Security Module Market: The Hardware Security Module Market is valued at USD 1.54 billion in 2026 and is forecast to reach USD 6.78 billion by 2035 at a CAGR of 17.8%. The hardware security module market growth directly anchors secure semiconductor supply chain investment as HSMs provide the cryptographic infrastructure for PUF enrollment, blockchain transaction signing, and certificate authority operations that enable authentic component tracking.

- Supply Chain Risk Management Software Market: The Supply Chain Risk Management Software Market is valued at USD 8.34 billion in 2026 and is expected to grow at a CAGR of 14.6% through 2035. The supply chain risk management market growth is accelerating adoption of semiconductor-specific traceability modules as OEMs integrate component authentication data into enterprise risk dashboards that inform procurement, quality, and regulatory compliance workflows simultaneously.

- Electronics Component Traceability Market: The Electronics Component Traceability Market is valued at USD 2.17 billion in 2026 and is projected to grow at a CAGR of 16.4% through 2035. The electronics traceability market growth supports real-time supply chain visibility by creating serial-number-level component records that enable post-deployment tracking and recall management for safety-critical electronics systems in automotive and industrial applications.

- Trusted Platform Module Market: The Trusted Platform Module Market is valued at USD 0.94 billion in 2026 and is forecast to reach USD 3.87 billion by 2035, expanding at a CAGR of 15.2%. The TPM market growth is driven by Windows 11 TPM 2.0 requirements, expanding government zero-trust architecture mandates, and growing automotive cybersecurity frameworks requiring hardware-rooted identity in connected vehicle platforms.

Key Growth Drivers of Secure Semiconductor Supply Chain Market

CHIPS Act Implementation, Defense Compliance Mandates, and Geopolitical Supply Chain Decoupling Drive Structural Investment Demand

National semiconductor legislation is the single most powerful structural force defining this market’s growth trajectory. The US CHIPS and Science Act, EU Chips Act, Japan’s Rapidus program, India Semiconductor Mission, and South Korea’s K-Semiconductor Belt collectively represent over USD 150 billion in committed government funding for semiconductor capacity expansion. Each program carries explicit supply chain security requirements for funded recipients, creating compliance-driven technology procurement that flows from tier-one fabricators through materials and equipment suppliers to packaging providers. Unlike cybersecurity investments driven by threat perception cycles, legislative compliance requirements create funded procurement timelines with enforcement mechanisms that make investment postponement legally and contractually costly.

DFARS counterfeit avoidance requirements function as a market demand multiplier extending compliance obligations from prime defense contractors to tier-two and tier-three suppliers. The Defense Contract Audit Agency has increased supply chain security audit frequency, with findings of inadequate counterfeit avoidance procedures triggering withheld payments and debarment actions. For vendors with DFARS-aligned documentation, CMMC marketplace listings, and established defense contractor references, this environment compresses sales cycles from twelve to eighteen months down to three to six months for compliance-essential solutions.

Geopolitical semiconductor supply chain decoupling is accelerating geographic diversification investments requiring supply chain security infrastructure. As fabrication capacity moves from Asia-Pacific clusters to new facilities in the US, Europe, Japan, and India, OEMs managing multi-sourcing must implement authentication systems verifying provenance across an expanded supplier set. The risk that diversification inadvertently opens new counterfeit insertion vectors — as new foundry relationships are established without mature verification protocols — is driving proactive security investment alongside geographic diversification capex.

Restraints

Implementation Complexity, Interoperability Fragmentation, and SME Compliance Cost Barriers Compress Adoption Velocity

Multi-standard interoperability fragmentation is the primary technical barrier constraining enterprise-wide adoption. Defense supply chains operate under DFARS and NIST SP 800-161 frameworks. Automotive supply chains reference ISO 26262 and IATF 16949 traceability requirements. European government procurement references ENISA semiconductor guidelines. Commercial OEMs manage customer-specific security questionnaire requirements that partially overlap but rarely align with any single compliance framework. Vendors responding to RFPs from customers across multiple regulatory domains must demonstrate compliance mapping across frameworks developed independently with different technical terminology, audit evidence requirements, and implementation timelines.

Integration complexity within incumbent ERP and quality management systems creates deployment timeline and cost barriers that suppress procurement conversion rates in commercial markets without legal compliance mandates. Supply chain security platforms requiring full data model integration with SAP S/4HANA or Oracle SCM Cloud before delivering functional value face implementation projects extending 12 to 24 months, with integration consulting costs that may equal platform license value over a three-year total cost of ownership. For mid-tier OEMs without dedicated supply chain IT program management resources, this implementation burden defers procurement decisions that would be immediate under an enforced compliance deadline.

Small and medium-sized enterprise cost barriers represent a structural adoption constraint at the base of the defense supply chain. CMMC 2.0 Level 2 compliance, expected to be required for approximately 80,000 DoD contractors, carries estimated annual compliance costs ranging from USD 100,000 to USD 1.2 million per organization depending on IT environment complexity. For small manufacturers, this compliance cost represents a meaningful portion of annual operating budget, creating incentives to self-certify minimum viable compliance documentation rather than invest in technology platforms generating auditable records. This cost sensitivity is driving cloud-native compliance-as-a-service models but simultaneously fragmenting the platform market as multiple vendors compete for constrained SME budgets.

Opportunities

Automotive EV Expansion, Commercial Space Supply Chain Security, and AI-Powered Counterfeit Detection Unlock Premium Revenue Segments

Electric vehicle semiconductor content expansion is unlocking the highest near-term average contract value growth in automotive supply chain security. The transition from internal combustion to battery electric platforms increases semiconductor count per vehicle by four to eight times while elevating the safety consequence of power electronics failures. Automotive OEMs designing ASIL-D power management and motor controller systems require supply chain traceability demonstrating component provenance to authorized fabrication sources as evidence in ISO 26262 safety case arguments. EV-related semiconductor procurement is forecast to reach USD 67 billion annually by 2030, with supply chain security program costs estimated at 1.5 to 2.5 percent of total semiconductor procurement value.

Commercial space and satellite supply chain security represents an emerging high-value market segment with rapidly growing procurement volume. New Space companies including SpaceX, OneWeb, Amazon Kuiper, and Telesat are procuring radiation-hardened and commercial-off-the-shelf electronics for satellite constellations at volumes that dwarf traditional government satellite procurement. FAA commercial space launch licensing requirements and FCC space debris mitigation rules are creating documentation frameworks incorporating component traceability requirements, pulling supply chain security platform investments into commercial space OEM procurement programs that did not exist five years ago.

AI-powered counterfeit detection services delivered as cloud-based subscriptions are creating a new revenue model converting traditionally capital-intensive inspection infrastructure into scalable software economics. Platforms that aggregate optical inspection images, electrical test results, and X-ray fluorescence spectra from distributed goods-receipt stations can apply continuously improving machine learning models without requiring individual customers to maintain training datasets. For vendors building network effect advantages through aggregated inspection data across multiple customers and component categories, this creates a compounding competitive moat that strengthens as counterfeit insertion techniques evolve and require model retraining that individual customer datasets cannot support.

Latest Trends in Secure Semiconductor Supply Chain Market

Quantum-Resistant Cryptography Integration and Digital Product Passports Reshape Platform Technology Requirements

Quantum-resistant cryptography migration is creating an urgent hardware security module and authentication platform upgrade cycle across all market segments. NIST’s finalization of post-quantum cryptographic standards, including CRYSTALS-Kyber and CRYSTALS-Dilithium, is triggering procurement replacement cycles for hardware security modules and TPM devices that cannot be firmware-updated to support lattice-based cryptographic operations. The NSA’s Commercial National Security Algorithm Suite 2.0 mandates post-quantum algorithm support for all national security systems by 2030, creating a funded government-sector upgrade cycle that will drive hardware security module replacement revenue through the forecast period. Commercial OEMs with 10-year product lifecycle commitments in automotive and industrial applications are beginning quantum-resistant hardware evaluation programs to ensure that supply chain authentication systems deployed today remain cryptographically valid through end-of-product-life timelines extending into the 2030s.

Digital Product Passports mandated under the EU Ecodesign for Sustainable Products Regulation are creating a new compliance-driven traceability infrastructure requirement that intersects directly with semiconductor supply chain security platforms. The regulation requires manufacturers of electronics, batteries, textiles, and other product categories to maintain machine-readable digital records documenting component origins, material compositions, repairability ratings, and end-of-life recycling pathways accessible through standardized data carrier formats including QR codes and RFID tags. Semiconductor traceability platforms that can serve both the ESPR digital product passport data model and the DFARS counterfeit avoidance documentation requirement with a unified data architecture will capture commercial OEM procurement that currently fragments across compliance-specific tools.

Semiconductor design IP protection through hardware watermarking is gaining commercial traction as fabless semiconductor companies address unauthorized overproduction by offshore contract manufacturers. Hardware watermarking techniques embed unique, statistically verifiable signatures into silicon layout geometries that survive manufacturing and are detectable through electrical test procedures without revealing proprietary design information. For fabless companies with high-volume consumer IC designs manufactured at contract foundries with multiple authorized and unauthorized third-party access points, hardware watermarking provides a provable intellectual property chain-of-custody that enables civil enforcement action against overproduction without requiring access to foundry production records.

Recent Developments: Infineon, NXP, and US DoD Lead 2025–2026

- February 2026 — NIST released the final implementation guidance for NIST SP 800-161 Revision 1 Cybersecurity Supply Chain Risk Management Practices, expanding semiconductor-specific risk assessment requirements and creating new documentation frameworks that supply chain security platform vendors are integrating as compliance templates.

- January 2026 — Infineon Technologies launched its SLS37 ALS31000 secure authentication IC with embedded PUF-based key generation and quantum-resistant symmetric authentication protocol support, targeting automotive ASIL-B supply chain applications requiring ISO 26262 compliant component authentication.

- December 2025 — The US Department of Defense released its updated Trusted Capital Marketplace semiconductor security guidelines, expanding Trusted Foundry Program scope to include advanced packaging facilities and creating new supply chain security audit requirements for CHIPS Act grant recipients.

- November 2025 — NXP Semiconductors announced EdgeLock 2GO Supply Chain Edition, extending its existing IoT device onboarding platform to support semiconductor component authentication across distribution and assembly supply chain stages, targeting automotive tier-one supplier compliance with OEM supply chain security requirements.

- October 2025 — IBM and the Semiconductor Industry Association co-launched the Semiconductor Trust Chain Initiative, a blockchain-based industry consortium platform enabling participating foundries, distributors, and OEMs to share authenticated component provenance records through a privacy-preserving distributed ledger architecture.

- September 2025 — Entrust Corporation received FIPS 140-3 Level 3 validation for its nShield 5c hardware security module family, enabling federal government and defense prime contractor deployments requiring current-generation FIPS certification for supply chain cryptographic key management.

- August 2025 — Thales Group acquired Imperva’s data security division for USD 3.6 billion, accelerating Thales Luna hardware security module integration with data provenance tracking capabilities targeting semiconductor IP protection and supply chain authentication use cases.

Report Features

| Feature | Description |

|---|---|

| Market Value (2026) | USD 664.51 billion |

| Forecast Revenue (2035) | USD 1,384.74 billion |

| CAGR (2026–2035) | 8.50% |

| Base Year for Estimation | 2026 |

| Historic Period | 2020–2025 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Hardware Security Modules, Supply Chain Software, Authentication & Traceability Services), By Security Type (Anti-Counterfeiting, Provenance Verification, IP Protection, Tampering Detection), By Technology (Blockchain-Based Traceability, PUF, AI-Driven Anomaly Detection, Zero-Trust Architecture), By End-Use (Defense & Government, Consumer Electronics, Automotive, Industrial, Telecommunications), By Enterprise Size (Large Enterprises, SMEs) |

| Regional Analysis | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Dominant Segment | Hardware Security Modules with 52.4%; Defense & Government with 42.8%; Anti-Counterfeiting with 38.2% |

| Dominant Region | North America with 38.4%; Asia-Pacific fastest-growing at 21.3% CAGR |

| Dominant Technology | Blockchain-Based Traceability with 34.6% share |

| Regulatory Framework | DFARS 252.246-7008, NIST SP 800-161 Rev 1, CMMC 2.0, US CHIPS Act Supply Chain Provisions, EU Chips Act, ENISA Semiconductor Guidelines, ISO 26262, IEC 61508, FIPS 140-3, SAE AS6171 |

| Competitive Landscape | Infineon Technologies AG, NXP Semiconductors N.V., Entrust Corporation, Honeywell International Inc., Microsoft Corporation, IBM Corporation, Broadcom Inc., Thales Group, Microchip Technology Inc., Synopsys Inc., Ansys Inc., Avnet Inc. |

Sources:

- OECD — Semiconductors and Global Value Chains: Policy Perspectives

https://www.oecd.org - U.S. Department of Commerce — CHIPS for America Strategy Paper

https://www.commerce.gov/chips - European Commission — European Chips Act & Semiconductor Strategy

https://digital-strategy.ec.europa.eu - World Trade Organization (WTO) — Global Value Chain Development Report

https://www.wto.org - Center for Strategic & International Studies (CSIS) — Semiconductor Supply Chain Security Report

https://www.csis.org - Semiconductor Industry Association (SIA) — State of the U.S. Semiconductor Industry 2024

https://www.semiconductors.org - National Institute of Standards and Technology (NIST) — Supply Chain Risk Management Practices for Semiconductors

https://www.nist.gov - Intel Corporation — Annual Report 2024 & Supply Chain Security Initiatives

https://www.intc.com - TSMC — Annual Report 2024 (Supply Chain Risk & Security)

https://www.tsmc.com - Samsung Electronics — Device Solutions (Semiconductor) Business Report

https://www.samsung.com - Applied Materials — Supply Chain and Manufacturing Report

https://ir.appliedmaterials.com - ASML Holding — Annual Report 2024 (EUV Supply Chain Security)

https://www.asml.com

Ramirez, Z. R., & Le, T. V. (2024). - Semiconductor Supply Chain Resilience: Systematic Review, Conceptual Framework, Implementation Challenges, and Future Research Directions. SSRN.

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4994726 - Dai, T., & Tang, C. S. (2024).

De-risking Global Supply Chains: Looking Beyond Material Flows. Asia Policy.

https://muse.jhu.edu/pub/136/article/942841 - Singh, J., et al. (2025).

Supply Chains and Geopolitical Crisis. Policy Brief.

https://www.isis.org.my/wp-content/uploads/2026/01/KCL-Semicon-Policy-Brief-Web.pdf - Moffat, L. L., & Poitiers, N. (2024).

Global Supply Chains: Lessons from a Decade of Disruption.

https://www.econstor.eu/handle/10419/294889 - Chimits, F., et al. (2024).

European Economic Security and Semiconductor Supply Chains.

https://www.movimentoeuropeo.it/images/Documenti/expo_ida-2024-754449_en.pdf - Tung, C. Y. (2024).

Taiwan and the Global Semiconductor Supply Chain.

https://roc-taiwan.org/uploads/sites/86/2023/08/20230824-TAIWAN-AND-THE-GLOBAL-SEMICONDUCTOR-SUPPLY-CHAIN.pdf - Christen, L. (2023).

The Global Supply Chain Challenge (Semiconductor Focus).

https://www.acgusa.org/wp-content/uploads/2023/02/20221231_Carl-Duisberg-Reseach-Fellowship_The-global-supply-chain-challenge.pdf - Takeda, M., Helms, M., & Watkins, C. (2024).

Strategic Supply Chain Resilience and Infrastructure Initiatives.

https://www.researchgate.net/publication/390415093 - World Semiconductor Trade Statistics (WSTS)

https://www.wsts.org - SEMI (Semiconductor Equipment & Materials International)

https://www.semi.org - International Energy Agency (IEA) — Semiconductor & Critical Minerals Reports

https://www.iea.org