What is the Smart Polymers Chemical Market Size?

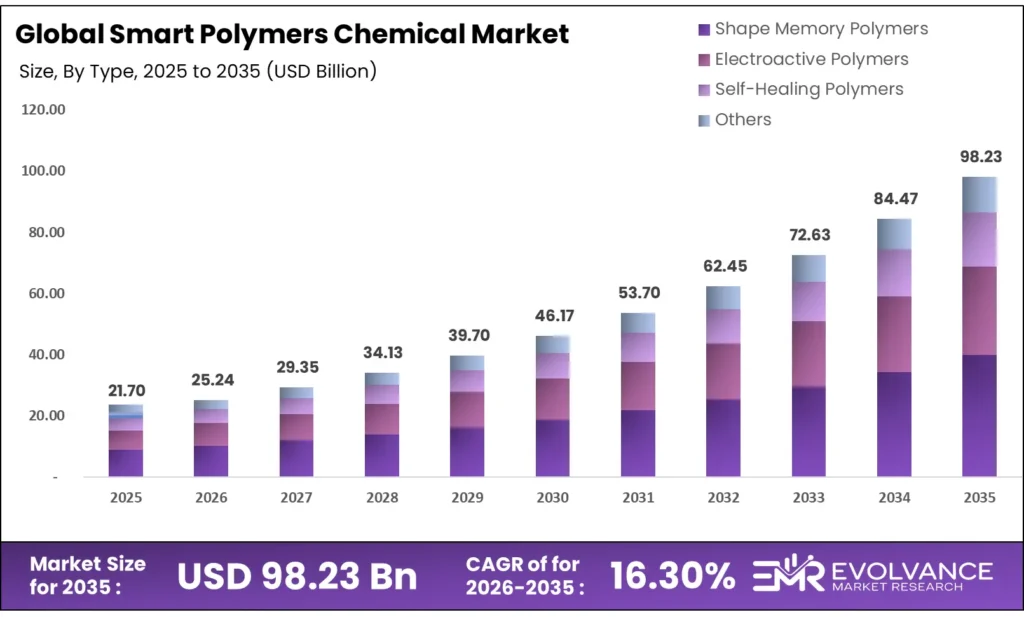

The Global Smart Polymers Chemical Market size will be worth around USD 98.23 Billion by 2035 from USD 21.70 Billion in 2025, growing at a CAGR of 16.30% during the forecast period 2026 to 2035. Biomedical device makers and automotive engineers are both pulling demand for stimuli-responsive materials in parallel. Buyers are shifting spend toward polymers that combine shape-memory and self-healing properties in a single platform. Raw material sourcing from petrochemical supply chains remains a constraint as bio-based chemicals alternatives scale up slowly.

Market Highlights

- The Global Smart Polymers Chemical Market valued at USD 21.70 Billion in 2025, reaching USD 98.23 Billion by 2035 at a CAGR of 16.30%.

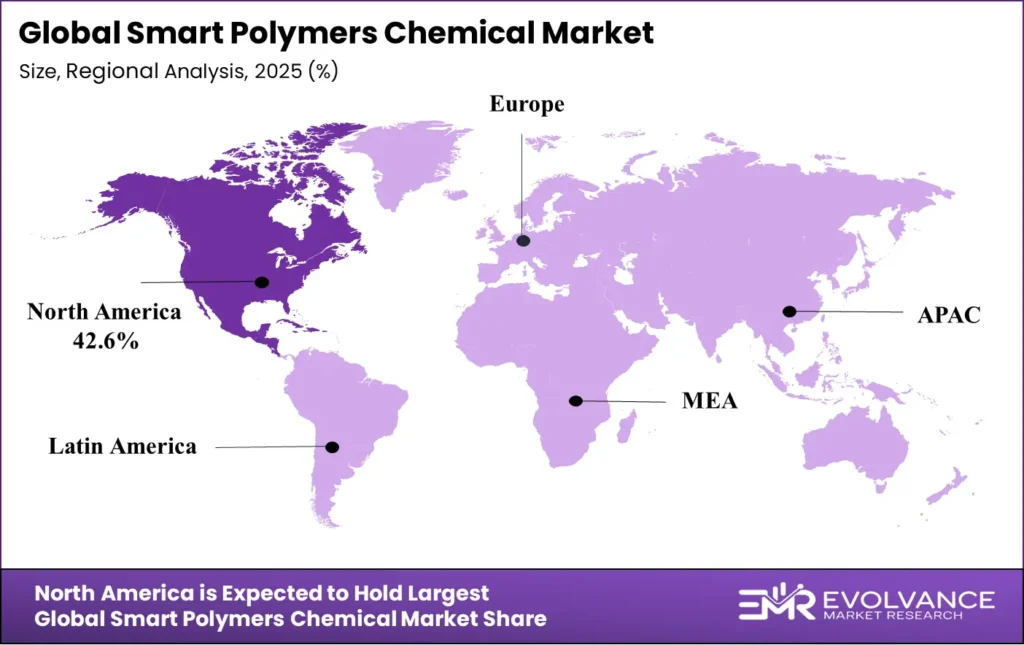

- North America leads with a 42.6% market share, valued at USD 9.2 Billion.

- By Type, Shape Memory Polymers dominate with 53.6% share.

- By Stimulus, Physical Stimuli Responsive leads with 67.4% share.

- By Processing Technique, Injection Molding holds 46.2% share.

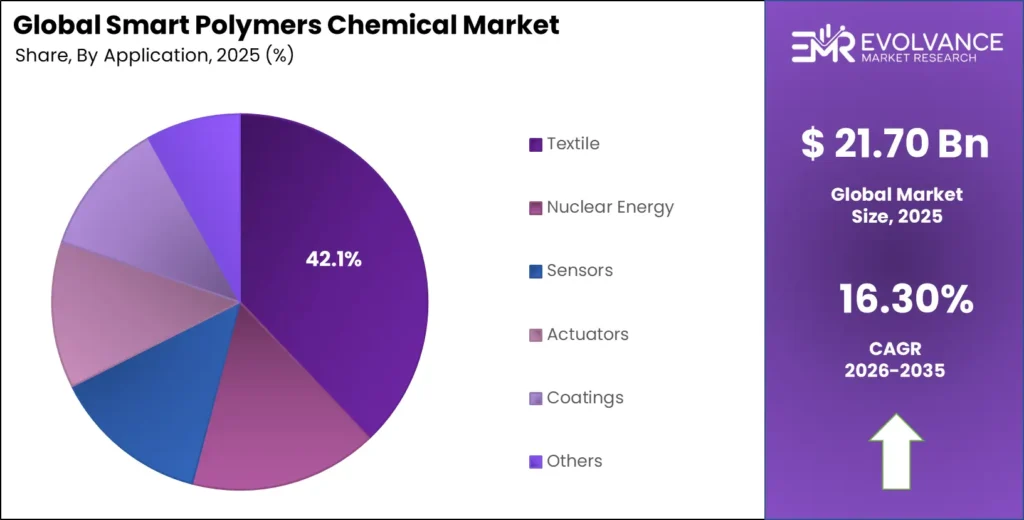

- By Application, Textile leads with 42.1% share.

- By End Use, Electrical and Electronics dominates with 47.3% share.

Market Overview

Smart polymers are materials that respond to external triggers such as heat, pH, light, electric fields, or magnetic forces by changing their shape, stiffness, or other physical traits. This responsiveness makes them useful across drug delivery, electronics, automotive, and aerospace applications. Unlike conventional plastics, their built-in adaptability removes the need for additional mechanical or electronic control systems.

The chemical market for these materials covers production, formulation, and sale of stimuli-responsive polymer compounds to industrial and research buyers. This includes shape-memory, electroactive, and self-healing polymer families. Buyers range from medical device makers to automotive OEMs to consumer electronics firms. Each segment values different trigger mechanisms and response speeds, which drives product-level differentiation across vendors.

Global plastics production reached 435 million tonnes in 2020, up from 234 million tonnes in 2000. This two-decade expansion of polymer manufacturing capacity has built the feedstock and process infrastructure that smart polymer producers now leverage. Specialty compounds like stimuli-responsive formulations sit at the high-value end of this supply base, allowing chemical firms to command premium pricing within an already-scaled industrial system.

As reported by OECD, plastics lifecycle greenhouse gas emissions will reach 2.8 gigatonnes CO2-equivalent annually by 2040, up from 1.8 gigatonnes in 2020. This trajectory is pushing industrial buyers to seek materials that extend product life or enable recyclability. Smart polymers with self-healing or bio-degradable properties directly address this pressure, making them strategically attractive to manufacturers facing ESG targets and regulatory scrutiny.

Government spending in North America and Europe is flowing into bio-based polymer research and advanced manufacturing. Regulatory frameworks increasingly incentivize circular material design, which benefits smart polymer producers offering biodegradable polymer variants. BASF’s launch of pH-sensitive biodegradable stimuli-responsive polymers for oncology drug delivery signals how regulatory pressure and market need are converging in the life sciences segment.

Type Insights

Shape Memory Polymers dominate with 53.6% due to broad use in automotive and biomedical sectors.

In 2025, Shape Memory Polymers held a dominant market position in the By Type segment of the Smart Polymers Chemical Market, with a 53.6% share. Their lead comes from two structural advantages: they work with standard polymer processing lines, and they respond to thermal triggers that most industrial systems already generate. Automotive lightweighting programs and minimally invasive medical device designs both rely on shape-memory behavior, giving this sub-segment a wide and stable buyer base.

Electroactive Polymers serve the flexible electronics and sensor markets, where mechanical actuation must occur without traditional motors or rigid components. Their role is expanding in soft robotics and wearable health monitors, two areas that are attracting large R&D budgets. Arkema’s advances in 5G and wearable applications highlight how electroactive polymer demand is being pulled by next-generation connectivity hardware that needs thin, flexible functional materials.

Self-Healing Polymers address a structural cost problem: material degradation over time. By enabling coatings and surfaces to repair minor damage without human intervention, these polymers reduce maintenance cycles in aerospace, automotive, and infrastructure markets. Covestro’s planned post-2025 expansions in self-healing coatings point to growing commercial confidence that this sub-segment can scale beyond laboratory-grade specialty materials into volume production.

Others in the type segment cover hydrogels, pH-responsive gels, and magnetically active formulations. These serve niche but growing applications in targeted drug delivery and environmental sensing. Their combined share remains modest today, but pharmaceutical investment in controlled-release systems is directing new development capital into this category, which could shift its position within the type mix over the forecast period.

Stimulus Insights

Physical Stimuli Responsive dominates with 67.4% due to established thermal and light-based trigger infrastructure.

In 2025, Physical Stimuli Responsive polymers held a dominant market position in the By Stimulus segment of the Smart Polymers Chemical Market, with a 67.4% share. Temperature and light are the most controllable and measurable triggers in industrial settings. Buyers across automotive, packaging, and medical sectors already have the equipment to manage these physical inputs, which makes physical stimuli polymers the lowest-friction choice when designing responsive material systems.

Chemical Stimuli Responsive polymers react to pH, ionic strength, or chemical concentration changes. BASF’s development of pH-sensitive biodegradable formulations for oncology drug delivery is the clearest commercial signal that this sub-segment is moving from research pipelines into scalable product lines. The ability to trigger release or shape change only in specific chemical environments makes these materials essential for precision medicine and environmental monitoring applications.

Biological Stimuli Responsive polymers respond to enzymes, glucose, or other biomolecular signals. Their primary use case is in implantable drug delivery and regenerative medicine, where a material must adapt to the body’s own chemistry rather than an external device. FDA and EMA approval timelines for novel biological-trigger systems remain a barrier, but the long-term value proposition in personalized therapy keeps investment flowing into this sub-segment.

Processing Techniques Insights

Injection Molding dominates with 46.2% due to high-volume compatibility and low per-unit cost.

In 2025, Injection Molding held a dominant market position in the By Processing Techniques segment of the Smart Polymers Chemical Market, with a 46.2% share. Most industrial smart polymer components — from automotive clips to medical casings — require consistent geometry at high throughput. Injection molding delivers both, and existing factory infrastructure already supports the process. This makes it the default choice for any smart polymer application moving from prototype to production scale.

3D Printing is the fastest-moving processing technique in this market. Evonik and Desktop Metal extended their collaboration to qualify INFINAM ST 6100L photopolymer for high-volume 3D printing of smart material components. Additionally, advances in vat photopolymerization (VPP) are enabling precision 4D printing of multi-stimuli responsive structures for biomedical use. These developments show that 3D printing is no longer a prototyping tool — it is becoming a volume production pathway for complex responsive geometries that injection molding cannot achieve.

Extrusion supports continuous production of smart polymer films, fibers, and coatings. The textile segment, which holds the largest application share, relies heavily on extruded smart fibers that change color, shape, or moisture response. Extrusion’s ability to process high volumes of thermoplastic smart polymers at consistent quality makes it a backbone technique for industrial-scale material manufacturing.

Application Insights

Textile dominates with 42.1% due to mass-market demand for responsive fabrics and performance wear.

In 2025, Textile held a dominant market position in the By Application segment of the Smart Polymers Chemical Market, with a 42.1% share. Sportswear, medical compression garments, and military fabrics all benefit from fibers that respond to body heat, moisture, or mechanical stress. The scale of the global textile industry means that even a modest smart polymer penetration rate translates into high absolute volume, which sustains this segment’s leading position.

Nuclear Energy applications use smart polymers for radiation-responsive sealing and containment materials. This is a small but highly regulated segment where performance requirements are extreme and material qualification timelines are long. Price sensitivity is low, making nuclear an attractive niche for specialty polymer producers willing to invest in compliance.

Sensors represent a high-growth application area driven by the spread of wearable electronics and IoT devices. Smart polymers that change conductivity or shape in response to pressure, chemical exposure, or temperature are enabling a new class of low-cost, flexible sensors. The integration of conductive and multi-stimuli polymers in AI and wearable devices is directing materials development toward faster-response, higher-sensitivity formulations.

Actuators use electroactive and shape-memory polymers to generate controlled mechanical movement without traditional motors. Soft robotics and prosthetics are the leading buyers, and both sectors are scaling. The shift toward bio-inspired machines that need compliant, lightweight actuation is pulling actuator-grade smart polymer demand upward.

End Use Insights

Electrical and Electronics dominates with 47.3% due to rapid wearable and flexible device adoption.

In 2025, Electrical and Electronics held a dominant market position in the By End Use segment of the Smart Polymers Chemical Market, with a 47.3% share. Consumer electronics manufacturers are embedding responsive polymer components into flexible displays, smart patches, and skin-integrated sensors at a pace that other end-use segments cannot match. The combination of miniaturization pressure and functionality demand in consumer tech makes electronics the most active procurement channel for smart polymer producers.

Healthcare is the second most important end-use segment and the one with the strongest long-term structural pull. pH and enzyme-responsive systems for targeted drug delivery, plus 4D-printed implants for regenerative medicine, represent the next wave of clinical adoption. However, FDA and EMA biocompatibility requirements slow time-to-market for novel formulations, which means the healthcare segment’s share growth will be steady rather than sudden.

Aerospace uses smart polymers primarily in morphing structures, self-healing surfaces, and lightweight adaptive components. The combination of weight reduction mandates and extreme environmental exposure in aerospace creates a compelling value case for smart materials. Defense procurement cycles are long, but contracts are large and performance standards keep out low-cost substitutes.

Automotive is integrating shape-memory and self-healing polymers into both structural and aesthetic components. Lightweighting for fuel efficiency and electric vehicle range extension are the primary drivers. Rising integration of these materials in adaptive performance components signals that automotive OEMs are moving beyond early pilots into series production, which will expand purchase volumes through the forecast period.

Market Segments Covered in the Report

By Type

- Shape Memory Polymers

- Electroactive Polymers

- Self-Healing Polymers

- Others

By Stimulus

- Physical Stimuli Responsive

- Chemical Stimuli Responsive

- Biological Stimuli Responsive

By Processing Techniques

- Injection Molding

- 3D Printing

- Extrusion

- Blow Molding

By Application

- Textile

- Nuclear Energy

- Sensors

- Actuators

- Coatings

- Others

By End Use

- Electrical and Electronics

- Healthcare

- Aerospace

- Automotive

- Others

Regional Insights

North America Dominates the Smart Polymers Chemical Market with a Market Share of 42.6%, Valued at USD 9.2 Billion

North America holds 42.6% of the global market, worth USD 9.2 Billion in 2025. This lead comes from deep university-industry research ties, mature procurement infrastructure in pharma and defense, and early federal investment in advanced materials. The US FDA’s approval framework, while slow, has already cleared several smart polymer drug delivery systems — creating a precedent that other regions are now trying to replicate.

Europe Smart Polymers Chemical Market Trends

Europe is the second-largest market, backed by the EU’s strong push toward bio-based and circular materials under its Green Deal and chemicals strategy. German and French chemical producers are investing heavily in sustainable smart polymer formulations. Regulatory alignment across EU member states gives producers a single compliance pathway, which lowers the cost of entering the European market compared to fragmented regulatory regimes elsewhere.

Asia Pacific Smart Polymers Chemical Market Trends

Asia Pacific is the fastest-growing regional market, led by China, Japan, and South Korea. China’s state-backed polymer industry is scaling production of electroactive and shape-memory materials for electronics and EV components. Japan leads in precision biomedical smart polymer research. South Korea’s electronics conglomerates are driving demand for flexible responsive materials in next-generation consumer devices and displays.

Latin America Smart Polymers Chemical Market Trends

Latin America represents an early-stage market where demand is concentrated in Brazil and Mexico. Industrial buyers here are primarily focused on smart polymer coatings for agricultural and infrastructure applications. Import dependency on North American and European producers keeps costs high, but local chemical manufacturers are beginning to explore licensing agreements to build regional formulation capacity.

Middle East & Africa Smart Polymers Chemical Market Trends

The Middle East and Africa market is at its earliest development stage. Gulf Cooperation Council nations are funding materials science research as part of economic diversification efforts. Demand for smart polymers in water treatment membranes and oil and gas pipeline coatings is emerging in the GCC. South Africa leads the African sub-region through its academic research institutions and mining sector material needs.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The US FDA’s 21 CFR framework governs smart polymer materials used in medical devices and drug delivery. Since 2024, the FDA has increased scrutiny on novel polymer implants and controlled-release systems. Any smart polymer with direct patient contact must pass biocompatibility testing under ISO 10993 standards before receiving market clearance. This requirement filters out unproven formulations and rewards producers with strong clinical data packages.

The European Chemicals Agency (ECHA) updated its REACH compliance requirements in 2024 to include stricter substance registration for stimuli-responsive polymer additives. Producers selling in the EU must document chemical triggers, degradation byproducts, and environmental persistence for all smart polymer formulations. This raises the compliance cost for new entrants but strengthens the competitive position of established producers with existing REACH portfolios.

The EU’s Chemical Strategy for Sustainability, reinforced in 2025, explicitly supports bio-based and biodegradable polymer development. Producers offering certified bio-derived smart polymers can access green procurement preferences in public contracts across EU member states. This policy creates a direct revenue advantage for companies that align R&D with sustainability criteria, which is reshaping product roadmaps at BASF, Evonik, and Solvay.

In North America, the 2024 National Advanced Manufacturing Plan allocated funding toward smart materials research in defense and aerospace. This creates a government-backed demand signal for high-performance shape-memory and electroactive polymers. Producers that qualify under defense procurement standards gain access to stable, high-margin contracts that insulate them from commercial market volatility.

Smart Polymers Chemical Market Dynamics

Drivers

Shape-Memory and Self-Healing Polymers Drive Adoption in Automotive Lightweighting and Adaptive Electronics

Automotive OEMs are under firm pressure to cut vehicle weight for electric range and fuel efficiency targets. Shape-memory polymers replace heavier metal components in interior and structural applications, delivering the same functional response at lower mass. This is not an experimental substitution — it is entering series production roadmaps at major manufacturers across Europe and Asia.

Self-healing polymers address a direct cost problem in consumer electronics: screen and casing damage. Devices that repair minor scratches without human intervention reduce warranty claims and extend product life cycles. Electronics producers view smart polymer integration as a quality differentiation tool. The rising integration of these materials in adaptive performance components is creating new OEM supply chain slots for specialty chemical producers.

Moreover, BASF’s launch of pH-sensitive biodegradable stimuli-responsive polymers for controlled-release oncology drug delivery shows how driver momentum crosses sectors. A single polymer platform developed for pharma can be adapted for agriculture, food packaging, and industrial sensing. This cross-sector applicability means the automotive and electronics demand wave also funds R&D that expands total addressable market for all buyers.

Restraints

High Production Costs and Biocompatibility Hurdles Limit Industrial and Clinical Scale-Up

Advanced stimuli-responsive polymer formulations require multi-step synthesis and tight process controls. These requirements push production costs well above conventional polymer benchmarks. For buyers outside pharma and defense — where price sensitivity is higher — the cost gap prevents broad adoption. According to OECD data, global plastics production doubled from 234 million tonnes in 2000 to 435 million tonnes in 2020, yet smart polymers remain a fraction of total volume because cost barriers have not yet collapsed.

Regulatory and biocompatibility hurdles are the second major brake on growth. FDA and EMA approval processes for novel smart polymer drug delivery and implant systems are long and expensive. Even polymer families with prior approvals for related applications must run new biocompatibility studies when formulation changes are made. This slows the speed at which clinical innovations reach commercial scale.

Furthermore, scalability challenges mean that laboratory-validated smart polymer formulations often perform differently at industrial volumes. Batch consistency, long-term stability under real-world conditions, and supply chain reliability for specialty monomers all create friction between proof-of-concept and full commercialization. Until these manufacturing challenges are solved at the process level, industrial buyers will remain cautious about switching from proven conventional materials.

Growth Factors

Bio-Based Smart Polymers and Wearable Electronics Open Two Parallel Revenue Streams

Sustainability regulations in Europe and North America are creating concrete commercial demand for bio-derived smart polymers. The EU’s circular economy mandate and US green procurement preferences are moving bio-based materials from a niche positioning into a procurement requirement. Producers who develop certified bio-based stimuli-responsive polymers will access public contracts and ESG-driven private buyers that conventional petrochemical-derived alternatives cannot serve.

Wearable electronics are generating a parallel demand stream. Smart wearable patches and skin-integrated devices need soft, responsive polymers that can flex, sense, and actuate against human skin. Arkema’s advances in 5G and wearables illustrate how major chemical producers are positioning smart polymer platforms for this market. OECD data shows plastics production will rise by 70% by 2040 from the 2020 base — and responsive specialty materials will capture an outsized share of that incremental volume.

Additionally, adoption in targeted drug delivery and regenerative medicine through pH and enzyme-responsive systems is building a third high-margin revenue layer. 4D-printed implants that change shape after insertion — guided by body temperature or biological triggers — represent a clinical category that did not exist five years ago. The producers who supply materials for these applications earn both premium pricing and long-term supply agreements tied to clinical program timelines.

Emerging Trends

4D Printing and Multi-Stimuli Polymer Platforms Redefine What Smart Materials Can Do

Vat photopolymerization is enabling 4D printing of structures that respond to pH, temperature, magnetic fields, and electric signals simultaneously. Multi-material VPP for 4D-printed stimuli-responsive devices — including encryption structures and shape-morphing components — represents a step change from single-response systems. Early movers who master this process hold a structural advantage: complex multi-stimuli geometry cannot be reverse-engineered quickly by competitors.

Sustainable and bio-derived smart polymer development is shifting from optional to mandatory in company R&D roadmaps. Major chemical producers are dedicating formulation budgets to bio-based responsive materials because sustainability-linked supply contracts are now standard in automotive and healthcare procurement. OECD data confirms that only 9% of total plastic waste was actually recycled globally in 2019 — a figure that is pushing regulators and buyers to demand inherently recyclable or biodegradable smart polymer alternatives.

Furthermore, conductive and multi-stimuli polymers are entering flexible electronics and AI-integrated sensor platforms. Smart wearable patches and skin-integrated devices are crossing from medical into consumer use cases. This trend is creating a new category of buyers — consumer electronics brands — who have the scale to absorb premium material costs and the marketing incentive to feature smart material functionality as a product differentiator in retail markets.

Key Companies Insights

BASF SE holds a strong position in this market through its materials science depth and recent move into pH-sensitive biodegradable stimuli-responsive polymers for oncology drug delivery. This development is not just a product launch — it signals BASF’s intent to link its polymer chemistry expertise directly to pharma procurement pipelines. By targeting controlled-release oncology systems, BASF positions itself in a segment where switching costs are high and margin protection is strong once clinical approvals are secured.

DuPont de Nemours, Inc. brings a broad portfolio of high-performance polymers that underpin several smart material applications in electronics, automotive, and industrial coatings. DuPont’s strength in material science paired with its global distribution network gives it reach into end-use segments that smaller specialty producers cannot efficiently serve. Its position in the electronics supply chain is particularly relevant as demand for flexible and responsive materials in wearables and sensors continues to scale.

Dow Inc. serves the smart polymer market through its specialty chemicals and advanced materials divisions. Dow’s scale in polymer manufacturing means it can bring responsive material formulations to market faster and at lower cost than pure-play specialty firms. However, its broad portfolio also means smart polymers compete internally for R&D and capital allocation priority. Focused specialty producers may outpace Dow in niche segments where technical differentiation is the primary purchase criterion.

SABIC is leveraging its position in the global petrochemical value chain to develop advanced smart polymer compounds for automotive and industrial markets. Its access to low-cost feedstocks in the Gulf region provides a cost structure advantage over Western European producers. SABIC’s investment in sustainable and circular polymer development aligns with growing buyer pressure for materials that meet ESG criteria without sacrificing mechanical performance.

Key Companies

- BASF SE

- DuPont de Nemours, Inc.

- Dow Inc.

- SABIC

- Evonik Industries AG

- 3M Company

- Huntsman Corporation

- Solvay SA

- Mitsui Chemicals, Inc.

- Others

Recent Development

- In October 2025, Covestro unveiled new mechanically recycled and bio-attributed polycarbonate (PC) and polyurethane (PU) grades under its “CQ” (Circular Intelligence) brand, containing at least 25% alternative raw materials.

- In October 2025, DOMO Chemicals launched DOMAMID polyamides with up to 69% bio-attributed content, achieving a nearly 100% CO₂ reduction compared to fossil-based grades.

- In October 2025, Evonik introduced its eCO product range, a portfolio of polymers and specialty chemicals designed to deliver up to 70% lower carbon emissions than conventional products.

- In October 2025, BASF expanded its circular polymer portfolio, highlighting reduced product carbon footprint (rPCF) grades and integrating renewable feedstocks.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 21.70 Billion |

| Forecast Revenue (2035) | USD 98.23 Billion |

| CAGR (2026-2035) | 16.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Shape Memory Polymers, Electroactive Polymers, Self-Healing Polymers, Others), By Stimulus (Physical Stimuli Responsive, Chemical Stimuli Responsive, Biological Stimuli Responsive), By Processing Techniques (Injection Molding, 3D Printing, Extrusion, Blow Molding), By Application (Textile, Nuclear Energy, Sensors, Actuators, Coatings, Others), By End Use (Electrical and Electronics, Healthcare, Aerospace, Automotive, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | BASF SE, DuPont de Nemours Inc., Dow Inc., SABIC, Evonik Industries AG, 3M Company, Huntsman Corporation, Solvay SA, Mitsui Chemicals Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Sources

- OECD – Saving Costs in Chemicals Management

- OECD – Chemical Safety

- OECD iLibrary – Testing of Chemicals

- European Environment Agency – Production of Chemicals

- Reuters – Chemicals Industry Struggles to Kick Its Fossil Fuel Habit (2025)

- OECD – A Chemicals Perspective on Designing with Sustainable Plastics

- World Bank – Chemicals Value Added in Manufacturing, OECD

- Statspanda – Production of Man-Made Chemicals (Live Counter)

- BASF – Combined Management Report FY2024

- BASF – Annual Report FY2025

- OECD – Plastics and the Environment

- OECD – Global Plastics Outlook: Full Report