What is the Advanced Power Electronics Market Size?

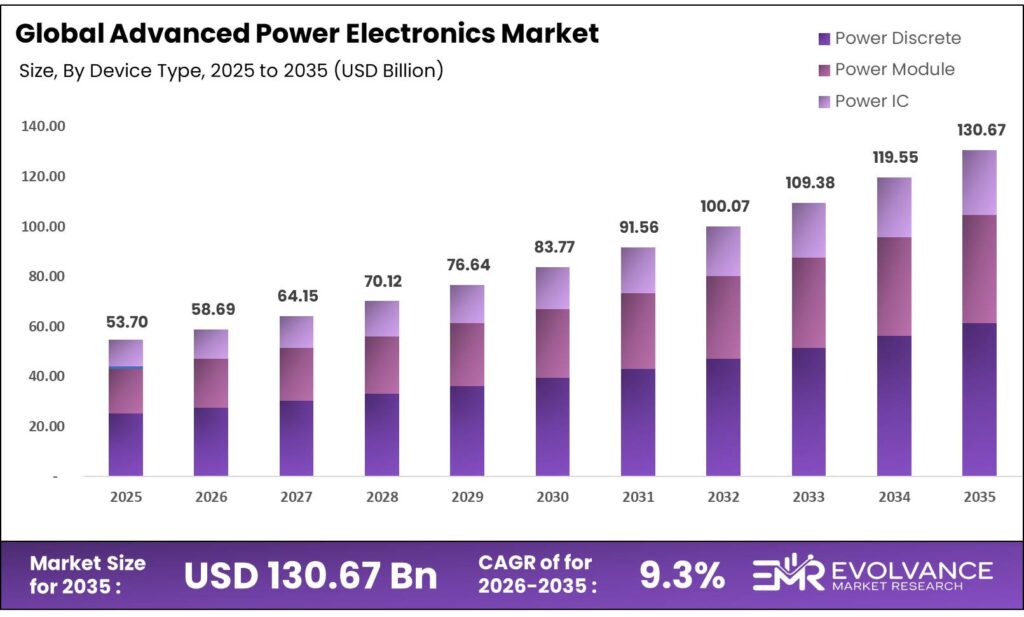

The Global Advanced Power Electronics Market size will be worth around USD 130.67 Billion by 2035 from USD 53.7 Billion in 2025, growing at a CAGR of 9.3% during the forecast period 2026 to 2035. Electric vehicle adoption and AI data center build-outs are pulling capital into wide bandgap devices at a pace legacy silicon cannot match. Enterprise buyers are shifting procurement toward SiC and GaN components, prioritizing efficiency and thermal performance over unit cost. However, limited substrate availability for wide bandgap materials remains a real supply constraint that could slow volume ramp-up through the mid-decade.

Market Highlights

- The Global Advanced Power Electronics Market valued at USD 53.7 Billion in 2025, reaching USD 130.67 Billion by 2035 at a CAGR of 9.3%.

- Asia Pacific leads with 43.7% market share, valued at USD 23.5 Billion.

- Power Discrete dominates the By Device Type segment with 61.2% share.

- Silicon Carbide leads the By Material segment with 54.7% share.

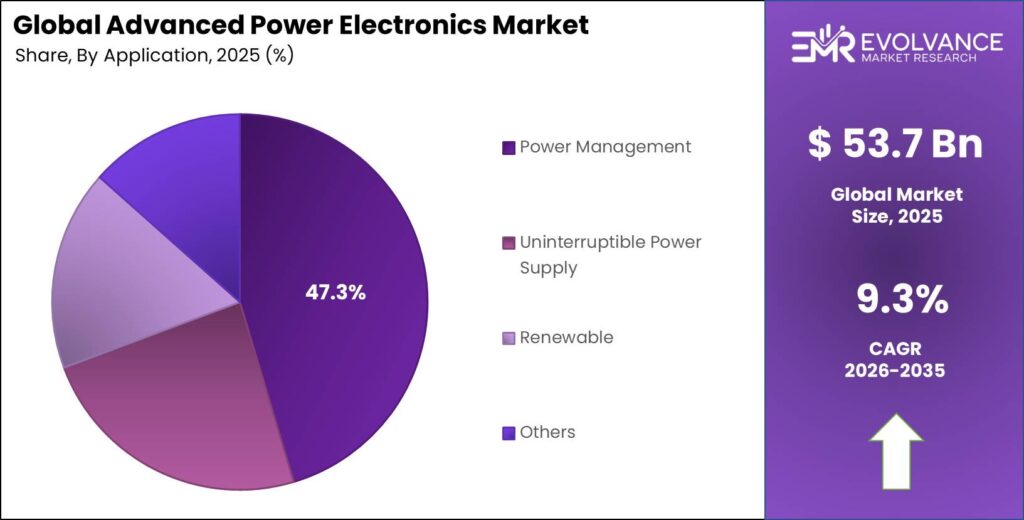

- Power Management leads the By Application segment with 47.3% share.

- Telecommunication leads the By End Use segment with 39.4% share.

Market Overview

The advanced power electronics market covers semiconductors, modules, and integrated circuits that control and convert electrical power across voltage levels and frequencies. These devices sit at the core of every modern energy system — from EV drivetrains to grid inverters to server power supplies. Without them, neither clean energy nor digital infrastructure can function at scale.

The market spans four primary technology layers: power discrete devices, power modules, power ICs, and wide bandgap materials such as Silicon Carbide and Gallium Nitride. Each layer serves distinct performance needs. Wide bandgap materials handle the most demanding applications — higher voltages, higher temperatures, and faster switching — where traditional silicon reaches its physical limits.

According to the International Energy Agency, global investment in data centres reached $500 billion in 2024, nearly doubling since 2022. This capital concentration directly funds power conversion hardware — the transformers, inverters, and voltage regulators embedded in every server rack. For power electronics vendors, data center build cycles now represent a demand baseline, not a cyclical uplift.

As reported by the International Energy Agency, global data centre electricity use reached 415 TWh in 2024, equal to 1.5% of total global electricity demand. Every terawatt-hour flowing through a hyperscale facility passes through power electronics at least twice. That conversion chain creates recurring demand for high-efficiency semiconductors — and vendors who improve conversion ratios by even a fraction of a percent gain an immediate procurement edge.

Government programs are reinforcing demand from the supply side. Grid modernization budgets across North America, Europe, and Asia are directing capital into power conversion infrastructure. Automotive electrification mandates are locking in multi-year procurement cycles for SiC-based traction inverters. These structural commitments reduce demand volatility and provide vendors with long-range visibility rarely seen in semiconductor markets.

Device Type Insights

Power Discrete dominates with 61.2% due to broad voltage compatibility and low switching losses.

In 2025, Power Discrete held a dominant market position in the By Device Type segment of the Advanced Power Electronics Market, with a 61.2% share. This dominance reflects structural demand across automotive, industrial, and telecom applications where discrete transistors, diodes, and thyristors deliver proven performance at competitive cost. Buyers prefer discrete devices for high-current applications where modular replacement reduces maintenance costs and extends system life cycles.

Power Modules address applications that require high power density in compact formats. These pre-packaged assemblies reduce design complexity for OEMs building EV inverters and industrial drives. Infineon Technologies raised its AI power supply segment revenue target to €1.5 billion for 2026 from €1.0 billion previously, signaling strong institutional demand for advanced module-based solutions in data center and EV platforms.

Power ICs serve control-layer functions — gate drivers, DC-DC converters, and power management units embedded in consumer and telecom electronics. Their value lies in integration: a single IC replaces multiple discrete components, cutting board space and BOM cost. This form factor advantage makes Power ICs the natural choice for compact, high-frequency applications such as AI server power supplies and 5G base station amplifiers.

Material Insights

Silicon Carbide dominates with 54.7% due to its thermal and voltage tolerance in EV and grid applications.

In 2025, Silicon Carbide (SiC) held a dominant market position in the By Material segment of the Advanced Power Electronics Market, with a 54.7% share. SiC outperforms silicon in high-voltage, high-temperature environments — the exact conditions found in EV traction inverters and utility-scale inverters. Toyota’s adoption of SiC MOSFETs in the bZ4X onboard charger and DC/DC converter confirms that Tier 1 automakers are standardizing on SiC for next-generation platforms, locking in multi-year volume demand.

Gallium Nitride (GaN) is gaining ground in high-frequency, compact power supply designs. GaN switches faster than SiC and enables smaller magnetic components, making it ideal for AI data center power architectures where space and thermal density are binding constraints. The power GaN market is projected at a 42% CAGR, driven by consumer and telecom applications — a rate that signals GaN is moving from niche qualification to mainstream deployment at accelerating speed.

Sapphire serves specialized optoelectronic and high-brightness LED applications where its optical transparency is a functional requirement. Its role in advanced power electronics is narrower than SiC or GaN but remains relevant in defense and precision industrial segments where thermal stability and hardness outweigh cost considerations.

Application Insights

Power Management dominates with 47.3% due to its presence across every electronic system class.

In 2025, Power Management held a dominant market position in the By Application segment of the Advanced Power Electronics Market, with a 47.3% share. Every electronic device — from smartphones to server racks — needs power management hardware to regulate voltage, control switching, and protect circuits. This universal dependency creates a demand floor that is resistant to cyclical correction. As per the International Energy Agency, the United States alone accounted for 45% of global data centre electricity use in 2024, representing approximately 187 TWh — a load that requires dense, high-efficiency power management at every conversion stage.

Uninterruptible Power Supply (UPS) applications are expanding alongside data center growth and grid reliability mandates. Hyperscale operators require N+1 or N+2 redundancy for every power rail, creating sustained demand for UPS power electronics even in periods of stable grid supply. This segment benefits directly from the $500 billion invested globally in data centers in 2024, as each new facility adds UPS capacity proportional to its IT load.

Renewable Energy applications include solar inverters, wind power converters, and battery energy storage systems. Global solar manufacturing investment reached $80 billion in 2023, according to the International Energy Agency — capital that flowed directly into inverter and converter hardware. As solar and wind capacity scales, each gigawatt of new generation requires a matching gigawatt of power conversion capacity, creating a linear demand relationship that compounds annual volume growth.

Others in the application segment cover medical equipment, aerospace systems, and lighting controls. These markets are smaller in volume but higher in margin. Medical and aerospace buyers apply stringent qualification standards that create long-term supplier lock-in — a dynamic that rewards vendors with deep application experience over commodity competitors.

End Use Insights

Telecommunication dominates with 39.4% due to continuous infrastructure upgrade cycles and power density demands.

In 2025, Telecommunication held a dominant market position in the By End Use segment of the Advanced Power Electronics Market, with a 39.4% share. 5G base station rollouts require GaN-based power amplifiers and high-efficiency rectifiers at every site. China accounted for 25% of global data centre electricity use in 2024, equivalent to approximately 104 TWh — a scale of digital infrastructure that demands matching telecom power electronics at the access, backhaul, and core network layers.

Industrial end users deploy power electronics in motor drives, welding systems, and process automation. This segment provides stable baseline demand but is sensitive to capex cycles in manufacturing. Vendors serving industrial buyers benefit from long replacement intervals and standardized form factors that reduce design-in costs — but must accept that pricing pressure is higher here than in automotive or defense.

Automotive is the fastest-scaling end-use segment by technology intensity. The shift from 400V to 800V EV architectures creates demand for SiC-based onboard chargers and DC-DC converters that did not exist in high volumes three years ago. STMicroelectronics power semiconductor sales reached $7,915 million in 2023, growing 13.0% year-over-year, driven by EV and industrial demand — showing that automotive electrification is already registering at revenue level for leading vendors.

Consumer Electronics absorbs large volumes of power ICs and GaN chargers. While unit margins are lower than automotive or defense, consumer electronics drives qualification activity that pulls new materials into cost-effective production. GaN chargers entering the consumer market today are building the volume base that will fund cost reductions for industrial and automotive GaN adoption in future years.

Energy and Power covers utility-scale grid-tied inverters, HVDC transmission converters, and substation automation. This segment is growing as grid operators modernize transmission networks. Government investment in grid infrastructure — particularly in North America and Europe — is converting public budget allocations into direct procurement demand for advanced power conversion hardware.

Market Segments Covered in the Report

By Device Type

- Power Discrete

- Power Module

- Power IC

By Material

- Silicon Carbide

- Gallium Nitride

- Sapphire

- Others

By Application

- Power Management

- Uninterruptible Power Supply

- Renewable

- Others

By End Use

- Telecommunication

- Industrial

- Automotive

- Consumer Electronics

- Military and Defense

- Energy and Power

- Others

Regional Insights

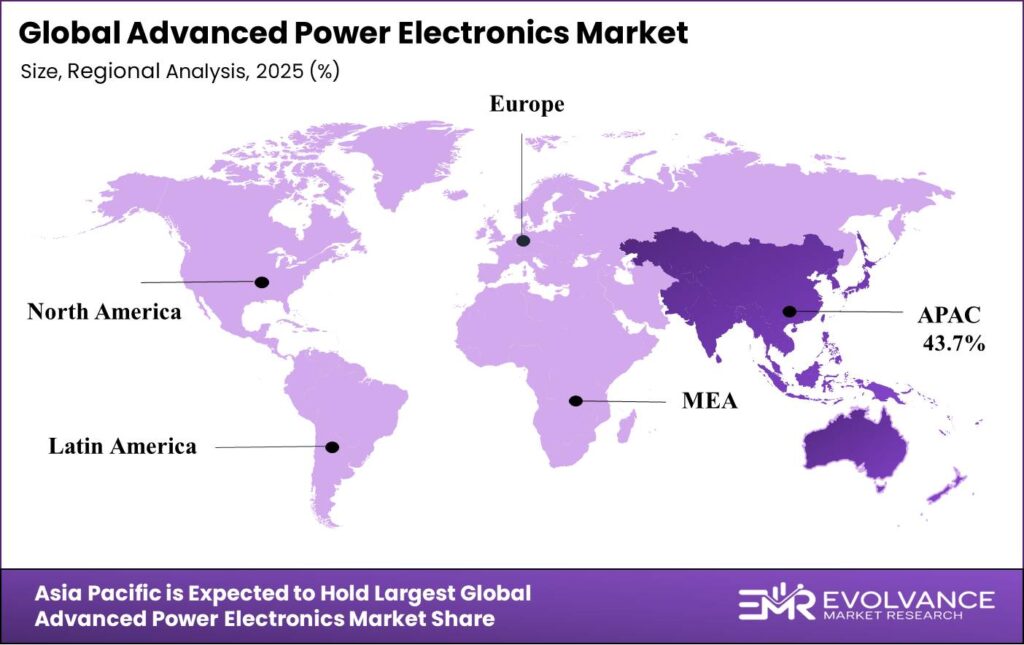

Asia Pacific Dominates the Advanced Power Electronics Market with a Market Share of 43.7%, Valued at USD 23.5 Billion

Asia Pacific holds 43.7% of the global advanced power electronics market, valued at USD 23.5 Billion. This lead reflects China’s position as the world’s largest producer and buyer of solar PV, EVs, and consumer electronics — all of which require dense power semiconductor content. China alone accounts for approximately 80% of global solar PV manufacturing capacity, according to the International Energy Agency, making the region the structural epicenter of power electronics demand and production.

North America Advanced Power Electronics Market Trends

North America holds the second-largest position, underpinned by large data center investments and an active EV supply chain build-out. The United States accounted for 45% of global data centre electricity use in 2024 — a load that requires high-efficiency power conversion at scale. Domestic semiconductor policy is also pushing supply chain localization, which is driving new fab investments that will gradually reduce import dependency for SiC and GaN devices.

Europe Advanced Power Electronics Market Trends

Europe’s position is shaped by aggressive emissions targets and industrial electrification policy. The EU’s carbon border adjustment and vehicle emission standards are forcing OEMs to accelerate EV transitions, which creates durable demand for SiC traction inverters. Europe accounted for 15% of global data centre electricity use in 2024, equivalent to approximately 62 TWh, supporting power conversion hardware demand across hyperscale and edge facilities.

Latin America Advanced Power Electronics Market Trends

Latin America is an emerging market for advanced power electronics, led by Brazil and Mexico. Grid expansion projects and renewable energy targets are creating early-stage demand for power conversion hardware. However, limited local manufacturing capability means the region depends heavily on imports — a structural constraint that keeps volume growth below the global average but creates distribution and integration opportunities for international vendors.

Middle East and Africa Advanced Power Electronics Market Trends

The Middle East and Africa region is investing in solar and grid infrastructure at a scale that will require substantial power electronics deployment over the forecast period. Gulf Cooperation Council nations are funding utility-scale renewable projects as part of energy diversification strategies. South Africa’s grid modernization program adds further demand. These government-led investments reduce demand uncertainty and support multi-year procurement contracts for inverter and converter hardware.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The U.S. CHIPS and Science Act, signed in 2022 and with funds actively disbursed through 2024-2026, allocates over $52 billion for domestic semiconductor production. For advanced power electronics, this directly funds SiC and GaN wafer fab capacity within U.S. borders. Vendors qualifying for CHIPS grants gain a cost floor advantage that reduces dependence on Asian substrate supply — a structural shift that reshapes competitive positioning.

The European Chips Act, effective from 2023 through its funding cycle into 2026, targets doubling Europe’s share of global semiconductor output to 20% by 2030. The regulation specifically supports wide bandgap semiconductor manufacturing, covering SiC and GaN technologies critical to EV and renewable energy applications. European OEMs procuring power electronics for vehicles sold in the EU will increasingly preference locally qualified sources to meet supply chain resilience requirements.

China’s semiconductor self-reliance policies, reinforced through 2024 government guidance, continue channeling state capital into domestic power semiconductor production. These policies affect global market dynamics by accelerating Chinese vendors’ qualification timelines for automotive and industrial-grade SiC devices, increasing competitive pressure on established Japanese and European suppliers in Asia Pacific markets.

Energy efficiency regulations such as the EU’s Ecodesign Regulation and the U.S. Department of Energy efficiency standards for power supplies mandate minimum conversion efficiency thresholds. These rules effectively set a performance floor that older silicon-based devices cannot meet, accelerating replacement cycles and pulling forward demand for SiC and GaN-based power electronics across industrial and data center applications.

Advanced Power Electronics Market Dynamics

Drivers

800V EV Platform Adoption Accelerates SiC Procurement Across Tier 1 Automotive Supply Chains

The shift from 400V to 800V EV architectures is not a gradual trend — it is a platform-level decision that locks in SiC component requirements for the vehicle’s entire life cycle. Automakers committing to 800V cannot revert to silicon-based inverters without redesigning the entire drivetrain. This creates multi-year, non-cancelable demand curves for SiC MOSFET vendors with qualified automotive-grade devices.

Toyota’s adoption of SiC MOSFETs in the bZ4X onboard charger and DC/DC converter illustrates how Tier 1 manufacturers are standardizing on wide bandgap materials for platform-level efficiency gains. This is not a single-vehicle program — Toyota’s platform decisions cascade across hundreds of thousands of annual units. Vendors achieving qualification on flagship EV models secure volume that compounds with every production ramp.

Additionally, ON Semiconductor’s power semiconductor sales reached $5,311 million in 2023, growing 3.4% year-over-year with EV adoption as a core driver. For investors, this confirms that automotive electrification is already generating measurable top-line growth for SiC specialists — and that the current correction in broader semiconductor revenues has not reversed the EV-specific demand trajectory.

Restraints

SiC and GaN Manufacturing Complexity Limits Yield and Raises Unit Costs Above Silicon Alternatives

SiC and GaN devices require production environments with tighter defect tolerances than standard silicon. SiC wafer defect density directly impacts device yield — and yield determines unit cost. Current wafer sizes are smaller than silicon’s mature 300mm standard, limiting the economies of scale that drive silicon’s cost competitiveness. Until GaN wafer manufacturing scales to 300mm, cost parity with silicon remains out of reach for most volume applications.

STMicroelectronics quarterly revenue declined to $3.46 billion in Q1 2024, an 18% year-over-year decrease, with margin compression reflecting both slower automotive demand and the fixed cost burden of wide bandgap production ramps. This margin pressure is not unique to STMicro — it signals that the industry is absorbing higher production costs ahead of volume revenues, a mismatch that smaller vendors cannot sustain without external capital.

Supply chain constraints compound the cost problem. SiC substrates depend on a narrow supplier base, and multi-year wafer supply agreements have become the primary mechanism for securing material access. Vendors without locked wafer supply face spot market pricing volatility that makes long-term customer pricing commitments risky. This dynamic favors vertically integrated players and disadvantages fabless or asset-light power electronics firms.

Growth Factors

AI Data Center Power Demands Create a Durable Revenue Base for High-Efficiency GaN Conversion Hardware

AI inference workloads require sustained, dense power delivery at the server rack level — a regime where GaN’s high-frequency switching and compact footprint outperform silicon. Figures from the International Energy Agency show global data centre electricity use grew at approximately 12% annually since 2017, a rate that compounds facility power budgets faster than efficiency gains offset them. Each new AI facility adds incremental power electronics demand that does not reverse when the facility reaches full utilization.

Infineon Technologies responded to this shift by raising its AI power supply segment revenue target to €1.5 billion for 2026, up from €1.0 billion. This 50% upward revision reflects confirmed design wins, not speculative forecasts. For the broader market, Infineon’s target revision signals that hyperscale buyers are committing capital to next-generation power conversion hardware on a timeline that vendors can plan manufacturing capacity around.

Moreover, advancements in 300mm GaN wafer manufacturing are beginning to enable cost-effective scaling. As GaN wafer sizes increase, per-device manufacturing costs fall along the same learning curve that silicon followed. This cost reduction trajectory will expand GaN’s addressable market from high-end data centers into mid-tier industrial and telecom applications — broadening the revenue base beyond the hyperscale segment that currently drives most GaN growth.

Emerging Trends

Vertical Integration in SiC Supply Chains Shifts Competitive Advantage From Device Performance to Material Access

Leading SiC vendors are moving upstream into substrate production to secure material supply and capture margin across the value chain. This vertical integration trend changes the competitive calculus: a company controlling its own wafer supply can offer long-term pricing stability that a fabless competitor cannot match. Multi-year wafer supply agreements are becoming the new competitive moat, replacing device performance as the primary differentiator in SiC markets.

Automotive-grade GaN transistors for 100V applications are now reaching qualification milestones with multiple Tier 1 suppliers. This qualification activity signals that GaN is moving from data center and consumer applications into the automotive supply chain — a transition that would open the highest-margin, longest-cycle procurement segment to GaN vendors. Early qualification wins in automotive GaN will translate into decade-long revenue relationships as platform production scales.

Furthermore, the power GaN market’s projected 42% CAGR driven by consumer and telecom demand is funding the R&D and manufacturing scale that will eventually make GaN cost-competitive in industrial and automotive segments. Consumer volume today is building the production infrastructure for automotive deployment tomorrow. Vendors investing in GaN capacity now are positioning for a market that will be larger and more diversified in three to five years than current revenue figures suggest.

Key Companies Insights

Rockwell Automation, Inc. positions itself at the intersection of power electronics and industrial software, embedding power conversion intelligence into its broader automation platforms. This integration strategy raises switching costs for industrial buyers who standardize on Rockwell’s ecosystem. However, Rockwell’s dependence on industrial capex cycles creates revenue exposure when manufacturing investment contracts — a structural vulnerability that its software revenue mix only partially offsets during downturns.

ABB Ltd. competes across the full power electronics value chain, from semiconductor-level components to grid-scale power conversion systems. ABB’s depth in grid infrastructure gives it access to utility procurement budgets that most semiconductor vendors cannot reach directly. As governments fund grid modernization at scale, ABB’s ability to bundle power electronics hardware with engineering and integration services creates a revenue model that pure-play component suppliers cannot replicate.

Toshiba Corporation maintains a strong position in power discrete devices and industrial power modules, with particular depth in IGBT and SiC product lines. Toshiba’s long history in power semiconductor manufacturing gives it mature process know-how for high-reliability applications in rail, industrial drives, and renewable energy. The company’s challenge is accelerating its SiC and GaN roadmap fast enough to stay competitive with dedicated wide bandgap specialists who are scaling capacity more aggressively.

STMicroelectronics N.V. is one of the most exposed major vendors to the EV demand cycle, with power semiconductor sales of $7,915 million in 2023 growing 13.0% year-over-year before the 2024 automotive slowdown compressed margins by 54% in Q1 2024. STMicro’s SiC product line is well-established, but the margin compression episode demonstrates that even well-positioned vendors face significant earnings volatility when a single end market — in this case automotive — corrects faster than production costs can flex downward.

Key Companies

- Rockwell Automation, Inc.

- Instruments Incorporated

- ABB Ltd.

- Toshiba Corporation

- Texas FUJI ELECTRIC CO, LTD.

- STMicroelectronics N.V.

- Microsemi Corporation

- Mitsubishi Electric Corporation

- Renesas Electronics Corporation

- Infineon Technologies AG

Recent Development

- In December 2024, the U.S. Department of Energy (DOE) announced $118 million in funding for ten Energy Frontier Research Centers, including $13.9 million over four years for the new “APEX” center (A Center for Power Electronics Materials and Manufacturing Exploration) led by NREL to advance next-generation power electronics.

- In October 2024, the Northeast Microelectronics Coalition (NEMC) Hub awarded over $1 million in grants to 13 companies through its PROPEL Manufacturing Program, funded by the CHIPS and Science Act, to support the development and production of advanced microelectronics, including power electronics.

- In November 2024, Infineon Technologies received the “Future Power Electronics Technology Innovation Award” from TrendForce for its advancements in wide-bandgap semiconductors, including the development of the world’s first 300mm gallium nitride (GaN) power semiconductor technology and the world’s thinnest 20µm silicon power wafer.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 53.7 Billion |

| Forecast Revenue (2035) | USD 130.67 Billion |

| CAGR (2026-2035) | 9.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Device Type (Power Discrete, Power Module, Power IC), By Material (Silicon Carbide, Gallium Nitride, Sapphire, Others), By Application (Power Management, Uninterruptible Power Supply, Renewable, Others), By End Use (Telecommunication, Industrial, Automotive, Consumer Electronics, Military and Defense, Energy and Power, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Rockwell Automation, Inc., Instruments Incorporated, ABB Ltd., Toshiba Corporation, Texas FUJI ELECTRIC CO, LTD., STMicroelectronics N.V., Microsemi Corporation, Mitsubishi Electric Corporation, Renesas Electronics Corporation, Infineon Technologies AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |