What is the Fatty Esters Market Size?

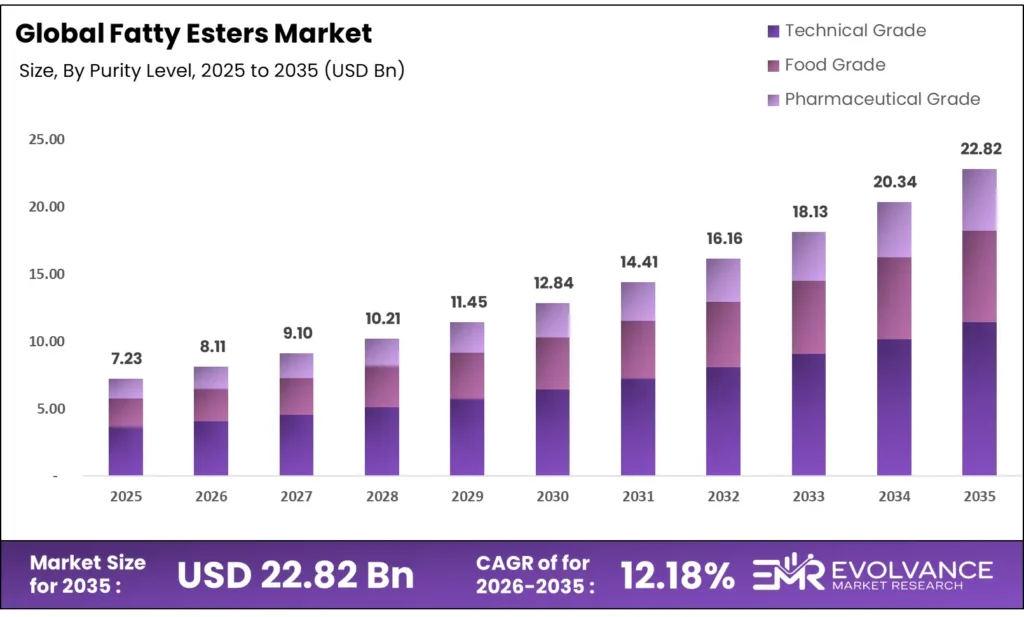

The Global Fatty Esters Market size will be worth around USD 22.82 Billion by 2035 from USD 7.23 Billion in 2025, growing at a CAGR of 12.18% during the forecast period 2026 to 2035. Methyl ester demand in biodiesel production and the shift to natural esters in personal care are the two forces pulling capital into this market. Buyers are actively replacing synthetic lubricants with bio-based ester alternatives, signaling a procurement shift with multi-year contract implications. Raw material price swings in vegetable oils remain the main cost variable manufacturers must manage.

Market Highlights

- The Global Fatty Esters Market valued at USD 7.23 Billion in 2025, expected to reach USD 22.82 Billion by 2035 at a CAGR of 12.18%.

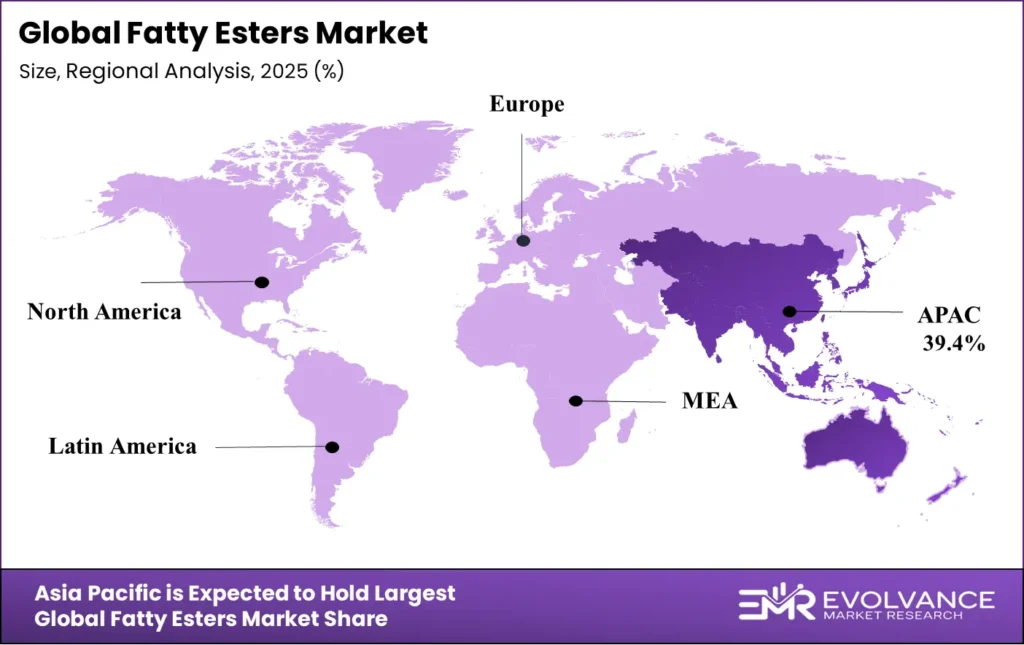

- Asia Pacific leads with a 39.4% market share, valued at USD 2.8 Billion.

- Methyl Esters dominate the By Product Type segment with a 38.1% share.

- Technical Grade leads the By Purity Level segment with a 58.7% share.

- Vegetable Oils hold the top spot in By Raw Material with a 54.3% share.

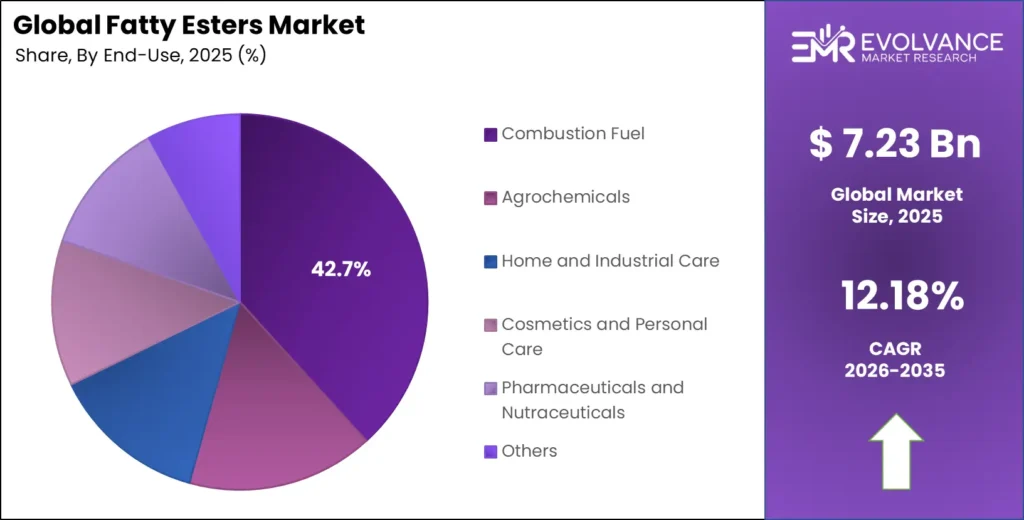

- Combustion Fuel leads the By End Use segment with a 42.7% share.

Market Overview

Fatty esters are compounds formed when fatty acids react with alcohols. They serve as core building blocks across biodiesel, lubricants, personal care, food processing, and pharma. Their versatility stems from adjustable carbon chain lengths and functional groups, which allow producers to tailor performance for each end-use sector without major process changes.

Global fatty acid ester exports reached 164 importing countries between July 2024 and June 2025, with 513 export shipments from 112 exporters serving 109 buyers across biodiesel and surfactant sectors. This breadth of trade coverage shows the market is not concentrated in a single application cluster — it is a horizontally distributed commodity with deep cross-industry penetration.

The shift away from fossil-based raw materials has placed fatty esters at the center of the green chemistry agenda. Brands in personal care, food, and industrial segments are replacing petroleum-derived additives with bio-based alternatives. This change is not cosmetic — it reflects binding sustainability commitments and retailer procurement requirements that are reshaping upstream demand.

Volza recorded 574 fatty ester export shipments worldwide between June 2024 and May 2025, with May 2025 alone accounting for 48 shipments — a 7% year-over-year rise compared with May 2024. A month-on-month uptick of this size signals that buyer restocking activity is accelerating, a forward indicator that end-market consumption remains firm heading into the second half of the forecast cycle.

Government mandates on renewable fuel blending and biodegradable lubricant standards are creating structural demand floors that give producers planning visibility. The EU’s revised Renewable Energy Directive and similar policies in Asian markets directly link fatty ester volumes to policy compliance cycles rather than pure market sentiment. This regulatory pull reduces demand volatility for large-scale methyl ester producers.

Product Type Insights

Methyl Esters dominate with 38.1% due to their direct use in biodiesel blending mandates.

In 2025, Methyl Esters held a dominant market position in the By Product Type segment of the Fatty Esters Market, with a 38.1% share. Their lead is structural, not cyclical — government-mandated biodiesel blending ratios in the EU, India, Indonesia, and the US directly specify fatty acid methyl esters (FAME) as the qualifying compound. Producers serving these mandates operate under long-term off-take agreements, which insulates their volume from spot-market demand shifts.

Ethyl Esters serve as a complementary biodiesel feedstock and a carrier solvent in pharmaceutical formulations. Their cost slightly exceeds methyl esters due to ethanol pricing, but they offer lower cold-flow pour points — a property that gives them an edge in colder-climate fuel blends and in regulated drug delivery applications where solvent purity is a compliance requirement.

Polyol Esters are the performance lubricant segment, prized for thermal stability and biodegradability in aerospace, compressor, and wind turbine applications. As industrial buyers face tighter environmental reporting obligations, polyol esters become a direct compliance tool — their use reduces lubricant-related carbon reporting liabilities at the asset level.

Sorbitan Esters are widely used as non-ionic emulsifiers in food and cosmetics. Their safety profile under global food additive regulations (E-numbers in the EU and GRAS status in the US) makes them a low-risk formulation choice for manufacturers targeting multiple regulatory jurisdictions simultaneously.

Isopropyl Esters function as lightweight emollients in skin care, offering fast skin absorption without occlusive residue. Consumer preference for non-greasy textures in daily moisturizers and sunscreens is directly supporting demand in this sub-segment, particularly in Asia Pacific markets where lightweight textures dominate prestige formulations.

Medium-Chain Triglycerides (MCTs) are the fastest-evolving sub-segment, driven by pharmaceutical drug delivery innovation and the mainstreaming of MCT oil in nutritional supplements. As reported by trade sources, strategic partnerships among major players including BASF, Croda International, and Lonza are underway to expand MCT product portfolios and geographic reach — a consolidation move that signals rising commercial value in this segment.

Purity Level Insights

Technical Grade dominates with 58.7% due to high-volume industrial and biodiesel applications.

In 2025, Technical Grade held a dominant market position in the By Purity Level segment of the Fatty Esters Market, with a 58.7% share. Its dominance reflects where volume sits — biodiesel production, industrial lubricants, and agricultural chemicals all run on technical-grade inputs. Buyers in these sectors compete on cost, not purity, which means technical grade producers benefit from scale economies and tight supply contracts that food and pharma grades cannot match on volume.

Food Grade esters command a price premium above technical grade, justified by stricter purity requirements and compliance with FDA, EFSA, and Codex Alimentarius standards. Demand is growing as clean-label reformulation projects expand across global food manufacturers, but the absolute volume ceiling is lower than industrial grade due to the specificity of food-use approvals.

Pharmaceutical Grade esters carry the highest unit value in the purity hierarchy. Their use in drug delivery, excipient systems, and nutraceutical encapsulation demands GMP-certified production lines, rigorous traceability documentation, and pharmacopeial compliance. These barriers limit supplier entry and protect margin for established producers with validated facilities.

Raw Material Insights

Vegetable Oils dominate with 54.3% due to abundant supply and established processing infrastructure.

In 2025, Vegetable Oils held a dominant market position in the By Raw Material segment of the Fatty Esters Market, with a 54.3% share. Palm, soy, sunflower, and rapeseed oils provide a large, globally traded feedstock base with competitive pricing relative to animal fats. Malaysia’s palm-oil oleochemical infrastructure alone exported 91 shipments of fatty esters during the June 2024 to May 2025 period, per Volza data — evidence that vegetable-oil-based production chains are already deeply integrated into global supply networks.

Animal Fats provide tallow and lard-derived esters used primarily in industrial lubricants and soap manufacturing. Their supply is a byproduct of the meat processing chain, which makes them cost-competitive but also exposes producers to supply variability tied to livestock cycles rather than dedicated oleochemical farming.

Tall Oil is a pine-derived byproduct of the paper pulp industry, offering a non-food-competing feedstock for ester production. Its role is rising as producers seek raw materials that do not compete with food supply chains — a sourcing argument that is gaining traction with sustainability-focused buyers.

End Use Insights

Combustion Fuel dominates with 42.7% due to binding renewable fuel mandates in major economies.

In 2025, Combustion Fuel held a dominant market position in the By End Use segment of the Fatty Esters Market, with a 42.7% share. Biodiesel blending mandates — B7 in the EU, B20 targets in Indonesia, and escalating blending requirements in India — create a guaranteed demand floor for fatty acid methyl esters that does not depend on consumer preference cycles. The United States exported 774 shipments of fatty acid esters between July 2024 and June 2025, representing approximately 38% of global export share, according to Volza — a volume largely tied to biodiesel feedstock trade flows.

Agrochemicals use fatty esters as adjuvants and emulsifiers in pesticide and herbicide formulations. Their role is to improve active ingredient spread and uptake on plant surfaces — a functional performance benefit that sustains demand independent of commodity crop price cycles.

Home and Industrial Care applications include surfactants, fabric softeners, and cleaning concentrates. Esters in this segment benefit from the wider reformulation push toward biodegradable cleaning agents, a shift driven by wastewater treatment regulations in Europe and tightening green procurement standards in corporate supply chains.

Cosmetics and Personal Care represent a high-margin end-use where ester selection directly affects product texture, skin feel, and stability. Consumer demand for natural and clean-label ingredients is directing formulators toward plant-derived esters over synthetic alternatives, supporting volume growth in this segment across prestige and mass-market tiers alike.

Pharmaceuticals and Nutraceuticals is the highest-value end-use in the portfolio. MCT oils, excipient esters, and lipid-based drug delivery systems are all drawing investment as pharmaceutical companies look for solubility-enhancing carriers with established safety records. India exported 267 shipments of fatty acid esters between July 2024 and June 2025 — roughly 13% of global export shipments per Volza — with a significant share directed to pharmaceutical and nutraceutical buyers in Europe and North America.

Market Segments Covered in the Report

By Product Type

- Methyl Esters

- Ethyl Esters

- Polyol Esters

- Sorbitan Esters

- Isopropyl Esters

- Glycerol Esters

- Medium-Chain Triglycerides (MCTs)

By Purity Level

- Technical Grade

- Food Grade

- Pharmaceutical Grade

By Raw Material

- Vegetable Oils

- Animal Fats

- Tall Oil

- Others

By End Use

- Combustion Fuel

- Agrochemicals

- Home and Industrial Care

- Cosmetics and Personal Care

- Pharmaceuticals and Nutraceuticals

- Others

Regional Insights

Asia Pacific Dominates the Fatty Esters Market with a Market Share of 39.4%, Valued at USD 2.8 Billion

Asia Pacific holds a 39.4% share worth USD 2.8 Billion, built on deep palm-oil processing infrastructure in Malaysia and Indonesia, large biodiesel blending mandates, and the region’s role as the world’s primary oleochemical production hub. China alone exported 247 shipments of fatty esters between June 2024 and May 2025, per Volza data — volumes that reflect both domestic industrial demand and re-export activity feeding global supply chains.

North America Fatty Esters Market Trends

North America is the world’s largest fatty ester exporter by shipment volume. The United States exported 686 fatty ester shipments between June 2024 and May 2025 — the highest country-level total globally, per Volza. This export dominance reflects a mature biodiesel supply chain, strong soy-oil processing capacity, and deep integration with pharmaceutical and cosmetic end-use markets that import and re-export specialty ester fractions.

Europe Fatty Esters Market Trends

Europe is a net importer of fatty esters, with Germany absorbing approximately 27% of global fatty ester import shipments — 470 shipments recorded in Volza trade data. Germany’s position reflects its role as the EU’s largest chemical processing economy, where imported esters feed specialty lubricant, surfactant, and personal care manufacturing. Spain and Italy also export regionally, supporting EU and Latin American markets with food-grade and cosmetic-grade ester volumes.

Latin America Fatty Esters Market Trends

Latin America is a growing consumption market for fatty esters, driven by expanding biodiesel mandates in Brazil and Mexico and a rising consumer goods sector that is adopting natural ingredient formulations. Brazil’s national biodiesel blending program creates a structural demand anchor for methyl esters, while Mexico’s personal care manufacturing base — serving both domestic and US export markets — is generating new demand for cosmetic-grade ester inputs.

Middle East & Africa Fatty Esters Market Trends

The Middle East and Africa region represents an early-stage but commercially relevant market for fatty esters. GCC countries are investing in downstream chemical processing to reduce raw material export dependency, creating conditions for local ester production to develop. South Africa’s established chemical and personal care manufacturing base offers a route for regional distribution into Sub-Saharan African consumer markets that are adopting packaged goods faster than local supply chains can respond.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The EU’s revised Renewable Energy Directive (RED III), effective from 2023 with binding national implementation targets through 2030, mandates a 42.5% renewable share in final energy use. This directive explicitly qualifies fatty acid methyl esters as compliant biodiesel components, creating a legislated volume floor that producers can plan around with multi-year confidence.

In 2024, the US Environmental Protection Agency finalized Renewable Fuel Standard (RFS) volume requirements through 2025, setting biomass-based diesel at over 3.35 billion gallons. This mandate directly sustains methyl ester demand from US soybean processors and keeps North American production capacity at high utilization rates regardless of spot fuel price movements.

The European Chemicals Agency (ECHA) continues its REACH compliance reviews for ester-based surfactants and lubricant additives, with updated substance evaluations published through 2024 and 2025. Manufacturers supplying the EU market must maintain Safety Data Sheets aligned with the latest Classification, Labelling and Packaging (CLP) Regulation updates — a compliance cost that disadvantages smaller producers lacking dedicated regulatory affairs teams.

India’s Bureau of Indian Standards (BIS) published updated specifications for biodiesel (B100) under IS 15607 in 2024, tightening methyl ester purity and cold-flow parameters. These updated specs affect producers supplying the Indian market directly, as non-compliant batches face rejection at blending terminals — putting a premium on consistent production quality from export origins including Singapore and Malaysia.

Fatty Esters Market Dynamics

Drivers

Biodiesel Mandates Create Structural Volume Floors for Methyl Ester Producers Amid Shrinking Fossil Fuel Reserves

Governments across the EU, India, Indonesia, and the US have written fatty acid methyl esters into binding fuel blend mandates. This is not discretionary demand — it is compliance-driven purchasing. Producers with long-term supply agreements tied to these mandates operate at predictable utilization rates, a structural advantage over companies serving purely market-driven sectors.

The United States exported 686 shipments of fatty esters between June 2024 and May 2025 — the highest country-level total globally per Volza. This volume reflects how deep the US biodiesel supply chain runs, from soy farm to export terminal. As fossil fuel reserves face stricter extraction limits in regulated markets, the renewable fuel mandate baseline will only extend further, extending the demand runway for methyl ester capacity investments made today.

Consumer Shift to Natural Esters in Personal Care Accelerates Specialty Grade Demand

Cosmetics and personal care brands are reformulating away from synthetic emollients toward plant-derived fatty esters to meet clean-label consumer expectations. This shift is brand-driven and retailer-enforced — major beauty retailers now publish restricted substance lists that functionally exclude several petroleum-derived alternatives. The consequence is a structural demand transfer, not a temporary trend.

Isopropyl and sorbitan esters are the primary beneficiaries. Their safety profiles under FDA and EFSA frameworks make them easy approval paths for formulators operating across multiple geographies. Japan exported 76 shipments of fatty esters between June 2024 and May 2025, per Volza, with a significant share attributed to high-value cosmetic and specialty chemical sectors — confirming that premium formulation markets are actively sourcing specialty esters at scale.

Restraints

High Production Costs of Bio-Based Ester Lubricants Slow Adoption Among Price-Sensitive Industrial Buyers

Bio-based polyol and ester lubricants carry a significant cost premium over mineral oil alternatives. For industrial buyers managing maintenance budgets under cost control pressure, this gap is a genuine adoption barrier. The performance case for bio-based esters is strong in regulated environments — but in sectors without mandatory biodegradability requirements, buyers default to lower-cost mineral options and absorb the environmental liability.

This cost gap is not closing fast enough to be dismissed. Enzymatic esterification reduces energy costs but does not yet match the per-tonne economics of large-scale petrochemical processing. Until bio-based lubricant producers either achieve greater scale or regulatory pressure forces a true total-cost-of-ownership comparison that internalizes environmental disposal costs, the price objection will persist in maintenance procurement decisions.

Raw Material Price Volatility Compresses Producer Margins and Disrupts Forward Planning

Vegetable oil prices — particularly palm, soy, and rapeseed — are subject to weather events, trade policy shifts, and energy market spillovers that create multi-quarter pricing uncertainty. Fatty ester producers relying on spot-market vegetable oil procurement face margin compression whenever feedstock costs spike without a corresponding ability to pass costs forward to customers under fixed-price contracts.

Animal fat prices introduce a different volatility dimension, tied to livestock cycle fluctuations rather than crop cycles. Producers using blended feedstock strategies can partially offset this, but the hedging infrastructure for oleochemical feedstocks is less developed than for energy commodities — leaving many mid-size producers exposed to price swings that erode quarterly profitability without warning.

Growth Factors

MCT Oil Expansion in Pharma Drug Delivery and Supplements Opens High-Margin Revenue Streams

Medium-chain triglycerides are moving from niche nutritional product to mainstream pharmaceutical excipient. Their ability to improve the oral bioavailability of poorly soluble drug compounds makes them a valued tool for formulation scientists — one that is gaining traction as the pharmaceutical pipeline fills with lipophilic compounds that need solubility-enhancing carriers to reach viable dosage forms.

The nutraceutical channel is equally active. MCT oil has crossed into mainstream consumer awareness through sports nutrition, ketogenic diet products, and cognitive supplement categories. This consumer pull is creating volume demand that pharmaceutical-grade MCT producers can partly serve, though the purity and documentation requirements differ significantly between channels. Producers who can serve both channels from shared infrastructure gain a unit economics advantage.

Fatty Esters as Fat Replacers in Food Processing Address Global Obesity Policy Pressure

Food manufacturers are under growing regulatory and consumer pressure to reduce saturated fat content in packaged foods. Fatty esters offer a technically sound fat-replacement pathway — they can mimic mouthfeel and texture while delivering fewer calories and a more favorable lipid profile. With over 30% of adults in major economies affected by obesity, governments are considering fat content labeling and reformulation incentives that could accelerate adoption.

This opportunity is not yet fully priced into market projections. Most current fatty ester demand in food processing is tied to emulsification rather than fat replacement. However, as food safety regulators in the EU and US signal intent to tighten saturated fat guidelines, reformulation activity will increase — and fatty ester producers with food-grade production lines and clean regulatory profiles are best positioned to capture that incremental volume.

Emerging Trends

Non-GMO and Upcycled Feedstock Sourcing Becomes a Commercial Differentiator, Not Just an ESG Label

The market is shifting toward traceability as a product feature. Buyers in personal care, food, and nutraceuticals are requesting batch-level documentation on fatty ester origin, crop certification, and processing route. This shift is being enforced through supplier questionnaires and ESG procurement policies at major consumer goods companies — making clean-supply-chain claims commercially binding rather than voluntary.

Molecular distillation is advancing alongside this sourcing shift. Improvements in this purification technique are enabling producers to achieve pharmaceutical and cosmetic purity levels from a wider range of feedstocks — including recycled cooking oils and upcycled oleochemical bystreams. This expands the addressable feedstock base while meeting the sustainability sourcing requirements that buyers now enforce.

Furthermore, the clean-label trend in food is reinforcing fatty ester adoption as a formulation component consumers can recognize and accept. Unlike synthetic emulsifiers with numerical E-code identifiers, ester-based alternatives can often be labeled with their natural source — “sunflower-derived emulsifier,” for example. This naming advantage reduces consumer rejection risk for food brands, making fatty esters a lower-risk clean-label swap that product development teams are actively pursuing.

Key Companies Insights

Arkema operates across high-performance specialty chemicals with a strong presence in bio-based ingredients for coatings, adhesives, and personal care. Its focus on renewable feedstock integration positions it to capture demand from formulators who need both performance and sustainability credentials in a single supplier. Arkema’s investment in bio-based acrylics and specialty esters reflects a deliberate strategy to move away from commodity chemical volumes toward higher-margin, application-specific solutions.

BASF SE reported total sales of €65.3 billion in fiscal year 2024 and invested €6.0 billion in capital expenditure, reflecting ongoing expansion across specialty chemical segments including oleochemicals and ester-based intermediates used in detergents, lubricants, and personal care. Despite revenue softening from €68.9 billion in 2023 due to broader chemical price compression, BASF’s EBITDA before special items held at €7.9 billion — evidence that its diversified portfolio including fatty ester intermediates sustains profitability even through sector-wide pricing cycles.

Elevance Renewable Sciences Inc. is a technology-forward producer using metathesis chemistry to convert natural oils into specialty chemicals with precise molecular structures. This approach allows Elevance to produce fatty ester derivatives with tailored performance properties that batch-process competitors cannot easily replicate. Its model targets high-value specialty niches in lubricants, surfactants, and personal care where custom chain-length esters command premium pricing and long-term application-specific contracts.

Krishi Oils Limited operates within India’s oleochemical supply chain, supplying fatty ester inputs to personal care, food, and industrial sectors. India’s role as a top-four global fatty ester exporter — with 247 shipments of fatty esters between June 2024 and May 2025 per Volza — provides Krishi with a favorable export environment backed by strong domestic feedstock availability from the country’s sunflower and soy processing industries. Its proximity to growing Southeast Asian import markets adds a logistics advantage over Western competitors.

Key Companies

- Arkema

- BASF SE

- Elevance Renewable Sciences Inc.

- Krishi Oils Limited

- Larodan AB (ABITEC)

- Wilmar International Ltd

- Cargill Incorporated

- Cayman Chemical

- Merck KGaA

- TCI Chemicals (India) Pvt. Ltd

Recent Development

- May 2025 – Global fatty ester export volumes recorded 48 shipments in a single month, a 7% year-over-year rise versus May 2024 per Volza. This uptick confirms that end-market restocking activity remained firm heading into mid-2025.

- July 2024 – June 2025 – Vietnam accounted for approximately 21% of global fatty acid ester imports with 89 shipments recorded per Volza, confirming its role as a leading consumption hub for biodiesel and industrial surfactant inputs in Southeast Asia.

- July 2024 – June 2025 – Germany absorbed approximately 21% of global fatty acid ester imports with 91 shipments logged per Volza, reflecting its position as the EU’s primary processing hub for specialty chemical inputs including ester-based lubricant and surfactant feedstocks.

- In 2024 – BASF SE reported total sales of €65.3 billion and capital expenditure of €6.0 billion, with investments covering specialty chemical capacity including fatty ester intermediates used in detergents, lubricants, and emulsifiers. The company generated EBITDA before special items of €7.9 billion, demonstrating sustained profitability across diversified chemical lines including oleochemicals and specialty esters for personal care and industrial use.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 7.23 Billion |

| Forecast Revenue (2035) | USD 22.82 Billion |

| CAGR (2026-2035) | 12.18% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Methyl Esters, Ethyl Esters, Polyol Esters, Sorbitan Esters, Isopropyl Esters, Glycerol Esters, Medium-Chain Triglycerides), By Purity Level (Technical Grade, Food Grade, Pharmaceutical Grade), By Raw Material (Vegetable Oils, Animal Fats, Tall Oil, Others), By End Use (Combustion Fuel, Agrochemicals, Home and Industrial Care, Cosmetics and Personal Care, Pharmaceuticals and Nutraceuticals, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Arkema, BASF SE, Elevance Renewable Sciences Inc., Krishi Oils Limited, Larodan AB (ABITEC), Wilmar International Ltd, Cargill Incorporated, Cayman Chemical, Merck KGaA, TCI Chemicals (India) Pvt. Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |