What Is the Adaptive Learning Software Market Size?

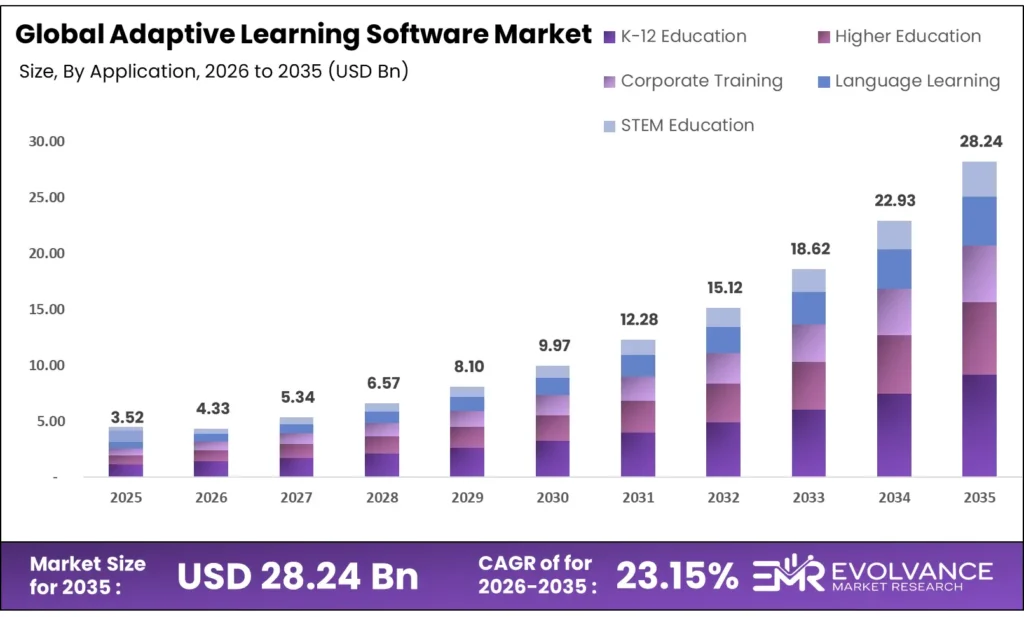

The Global Adaptive Learning Software Market was valued at approximately USD 3.52 billion in 2025 and is projected to grow from USD 4.33 billion in 2026 to nearly USD 28.24 billion by 2035, registering a CAGR of around 23.15% during 2026–2035. Growth is accelerating as educational institutions, corporations, and governments invest in AI-powered personalized learning platforms to close skills gaps and improve outcomes.

Adaptive learning software uses artificial intelligence, machine learning, and data analytics to adjust content, pacing, and difficulty in real time based on learner performance. Expansion is driven by rising edtech investments, cloud-based LMS adoption, generative AI integration, and competency-based education models globally.

The Adaptive Learning Software Market is experiencing steady growth as educational institutions adopt AI-driven personalized learning solutions to improve outcomes and engagement. These platforms enable real-time analytics and customized content delivery. The market is closely connected with advancements in the Agentic AI for Customer Support Automation, where intelligent systems enhance user interaction. Moreover, integration with the Content Creator Economy supports the creation of educational content, while synergies with the AI Podcast Creation Platforms enable audio-based learning experiences.

Market Highlights

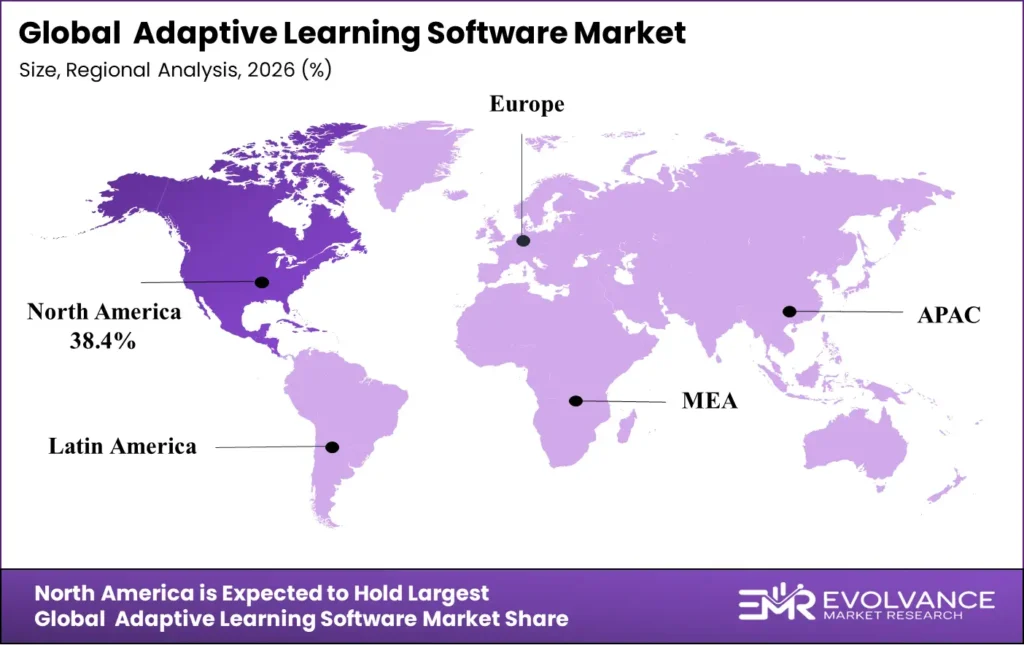

- North America dominated the market, holding the largest share of 38.4% in 2025.

- Asia Pacific is expected to expand at the fastest CAGR of 27.8% during 2026–2035.

- By component, the platform software segment dominated with the largest share of 36.7% in 2025.

- By component, the analytics & reporting segment is expected to expand at the fastest CAGR of 25.9% during 2026–2035.

- By deployment, the cloud-based segment accounted for the biggest market share of 68.5% in 2025.

- By deployment, the hybrid segment is expected to grow at a CAGR of 28.1% during 2026–2035.

- By application, K-12 education contributed the highest market share of 32.4% in 2025.

- By application, the corporate training segment is expected to expand at the fastest CAGR of 26.3% during 2026–2035.

- By technology, the AI & ML segment is expected to expand at the fastest CAGR of 29.4% during 2026–2035.

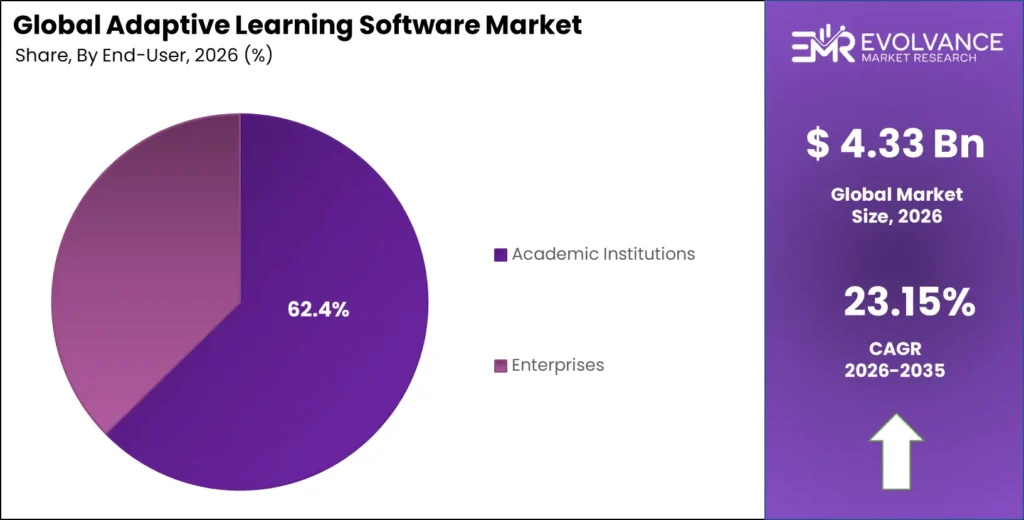

- By end-user, the academic institutions segment captured the highest market share of 62.4% in 2025.

- By end-user, the enterprise segment is expected to expand at the fastest CAGR of 25.7% during 2026–2035.

U.S. Adaptive Learning Software Market Size and Growth 2026 to 2035

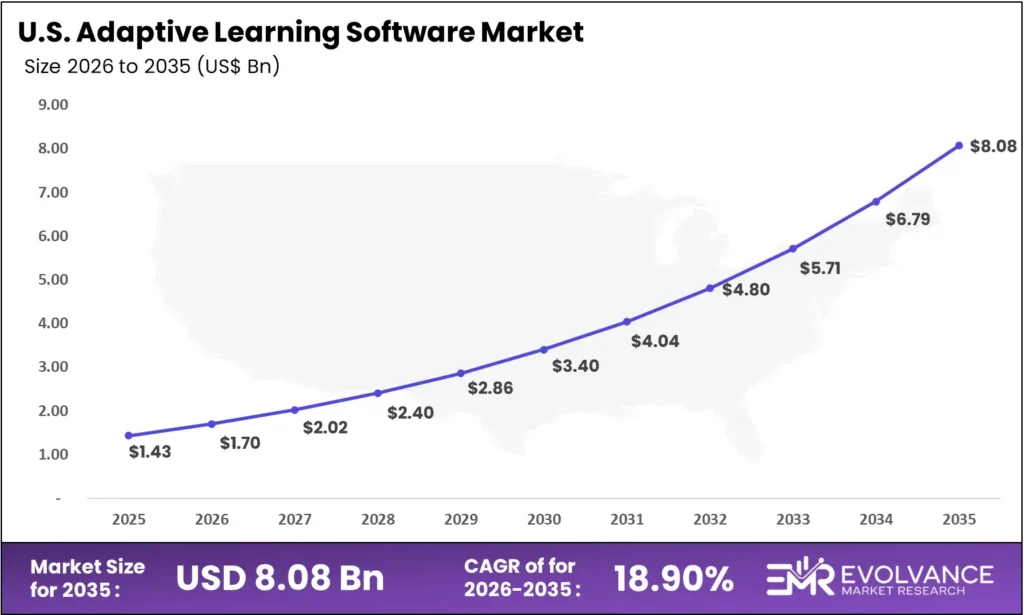

The U.S. Adaptive Learning Software Market size is estimated at USD 1.43 billion in 2025 and is projected to reach approximately USD 1.70 billion in 2026, reflecting strong enterprise and institutional adoption of AI-powered personalized learning platforms. The market is expected to grow at a strong CAGR of 18.90% from 2026 to 2035, driven by rising demand for outcome-focused digital instruction within K-12 schools, universities, and enterprise training programs. Increasing integration of AI-driven content curation, cloud-native LMS platforms, and competency-based learning modules across industries such as healthcare, BFSI, technology, and manufacturing is accelerating market expansion.

Organizations across the United States are embedding adaptive learning engines directly into LMS, HRIS, and workforce development systems to enhance productivity, reduce skills gaps, and improve learner retention. Growing government investments in digital education infrastructure and corporate mandates for continuous learning further support long-term market growth.

What Is Adaptive Learning Software?

Adaptive Learning Software is intelligent educational technology that uses artificial intelligence, machine learning, data analytics, and cognitive science to personalize learning in real time. It continuously evaluates learner progress, identifies skill gaps, predicts performance, and adjusts content, difficulty, and assessments accordingly. By leveraging learner modeling, knowledge tracing, and spaced repetition, these platforms enhance engagement, improve outcomes, and enable scalable, personalized education across academic, corporate, and lifelong learning environments.

Adaptive Learning Software Market Outlook

Rising Demand for Personalized Learning at Scale

Global learner populations continue to expand with over 1.8 billion students enrolled in formal education and over 3.5 billion workers requiring continuous upskilling. This unprecedented demand is compelling institutions and enterprises to invest in adaptive learning platforms capable of delivering individualized instruction at scale. Over USD 680 billion is projected for global education technology spending through 2035, creating substantial demand for AI-driven adaptive systems spanning intelligent tutoring, automated assessment, personalized content recommendation, and real-time learning analytics dashboards.

Generative AI Integration in Learning Platforms

The rapid integration of generative AI is fundamentally transforming adaptive learning by enabling dynamic content creation, conversational AI tutors, automated question generation, and real-time feedback synthesis. Large language models and multimodal AI systems are enabling platforms to generate personalized explanations, create practice exercises tailored to individual knowledge gaps, and simulate one-on-one tutoring interactions at scale. Over 72% of major edtech platforms are expected to integrate generative AI capabilities by 2028, driving demand for sophisticated adaptive learning engines.

Corporate Upskilling and Workforce Transformation

The global skills gap crisis is accelerating enterprise adoption of adaptive learning platforms, with corporate learning and development budgets exceeding USD 380 billion annually. Companies are deploying AI-powered adaptive training systems to reduce onboarding time by up to 50%, increase knowledge retention by 35%, and deliver compliance training across distributed global workforces. However, challenges remain including integration complexity with existing HR systems, content migration costs, and measuring definitive ROI on learning technology investments.

Government Digital Education Mandates

Governments worldwide are implementing national digital education strategies driving adoption of adaptive learning technologies. India’s National Education Policy, the EU’s Digital Education Action Plan, China’s Education Modernization 2035 initiative, and the U.S. National Educational Technology Plan are allocating billions toward personalized learning infrastructure, creating regulatory tailwinds for adaptive platform adoption across public education systems.

Key Market Trends

- Conversational AI Tutoring: Growing deployment of LLM-powered conversational tutors providing real-time explanations, Socratic questioning, and personalized feedback across subjects from mathematics to professional certification preparation.

- Learning Analytics & Predictive Modeling: Rising adoption of advanced analytics platforms that predict learner outcomes, identify at-risk students, and recommend early interventions through behavioral pattern analysis and knowledge tracing algorithms.

- Microlearning & Adaptive Content Delivery: Increasing demand for bite-sized, adaptive microlearning modules optimized for mobile devices, enabling just-in-time learning in corporate environments and reducing cognitive load for improved retention.

- Competency-Based Adaptive Pathways: Emergence of competency-based education models powered by adaptive platforms that map learning to specific skills, enabling learners to progress at their own pace with mastery-based advancement criteria.

- Multimodal Adaptive Experiences: Growing investment in adaptive systems supporting video, AR/VR simulations, interactive labs, and gamified scenarios that dynamically adjust across modalities based on learner preferences and performance data.

- Interoperability & Learning Ecosystem Integration: Expanding demand for adaptive platforms that seamlessly integrate with LMS, SIS, HR systems, and credential platforms via xAPI, LTI, and open standards to create unified learning ecosystems.

Market Scope

| Report Coverage | Details |

|---|---|

| Market Size in 2025 | USD 3.52 Billion |

| Market Size in 2026 | USD 4.33 Billion |

| Forecasted Market Size by 2035 | USD 28.24 Billion |

| Market Growth Rate (2026–2035) | CAGR of 23.15% |

| Base Year | 2025 |

| Historic Period | 2020–2025 |

| Forecast Period | 2026–2035 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | Component, Deployment, Application, Technology, End-User, Region |

Component Insights

The platform software segment dominated the Adaptive Learning Software Market with the largest share of 36.7% in 2025, driven by growing institutional demand for comprehensive adaptive engines capable of real-time learner modeling, content sequencing, and performance analytics. Institutions are prioritizing platform investments that offer scalable personalization across diverse subject areas and learner populations.

The analytics and reporting segment is expected to expand at the fastest CAGR of 25.9% during 2026–2035, fueled by increasing emphasis on learning outcome measurement, accreditation compliance reporting, and data-driven instructional decision-making across academic and corporate environments.

Deployment Insights

The cloud-based deployment segment accounted for the biggest market share of 68.5% in 2025, driven by scalability advantages, lower upfront costs, automatic updates, and accessibility across devices and locations. Cloud deployment enables institutions to serve geographically dispersed learners while maintaining centralized data analytics and content management.

The hybrid deployment segment is expected to grow at a CAGR of 28.1% during 2026–2035, supported by enterprise requirements for data sovereignty, offline learning capabilities in low-connectivity regions, and integration with existing on-premise learning management infrastructure.

Application Insights

The K-12 education segment held the major market share of 32.4% in 2025, driven by government-mandated digital learning programs, growing adoption of personalized math and reading platforms, and post-pandemic acceleration of blended learning models across 700 million primary and secondary students globally.

The corporate training segment is expected to expand at the fastest CAGR of 26.3% during 2026–2035, propelled by accelerating workforce reskilling needs, compliance training automation, and enterprise demand for measurable learning outcomes tied to business performance metrics.

End-User Insights

The academic institutions segment captured the highest market share of 62.4% in 2025, as schools, colleges, and universities invest in adaptive platforms to improve student outcomes, reduce dropout rates, and deliver equitable access to personalized education. The enterprise segment is expected to expand at the fastest CAGR of 25.7% during 2026–2035, driven by growing corporate learning budgets, talent retention strategies linked to continuous development, and demand for AI-powered skills gap analysis and career pathing solutions.

Segments Covered in the Report

By Component

- Platform Software

- Content Tools

- Analytics & Reporting

- Services

By Deployment Mode

- Cloud-Based

- On-Premise

- Hybrid

By Application

- K-12 Education

- Higher Education

- Corporate Training

- Language Learning

- STEM Education

By Technology

- AI & Machine Learning

- Natural Language Processing

- Data Analytics

- Gamification

By End-User

- Academic Institutions

- Enterprises

- Government

- Individual Learners

Regional Insights

North America — Leading the Market

North America dominated the adaptive learning software market with the largest share of 38.4% in 2025. The region’s leadership is driven by the world’s most mature edtech ecosystem, substantial venture capital investment exceeding USD 8 billion annually in education technology, strong institutional adoption across over 6,000 higher education institutions, and pioneering corporate learning programs at Fortune 500 companies. The U.S. Department of Education’s National Educational Technology Plan and the Every Student Succeeds Act provisions for evidence-based learning technologies provide regulatory support for adaptive platform adoption across 130,000 K-12 schools nationwide.

Asia Pacific — Fastest Growing Region

Asia Pacific is expected to expand at the fastest CAGR of 27.8% during 2026–2035, driven by massive student populations exceeding 800 million, aggressive government digitization of education systems, and rapidly growing edtech markets in China, India, South Korea, and Southeast Asia. China’s AI+Education national strategy, India’s National Education Policy 2020 emphasizing technology-enabled learning, and South Korea’s AI Digital Textbook initiative launching in 2025 are creating unprecedented demand for adaptive learning platforms across the region.

Europe — Significant Market Position

Europe holds a significant position in the adaptive learning market, driven by the EU’s Digital Education Action Plan investing €2 billion in digital learning infrastructure, GDPR-compliant adaptive platform development, and strong adoption across Nordic countries leading in educational innovation. Major deployments across Germany, the United Kingdom, France, and the Netherlands are driving demand for multilingual adaptive content engines and cross-border competency frameworks.

Latin America — Emerging Opportunities

Latin America’s adaptive learning market is growing steadily, driven by government digital education initiatives, expanding mobile internet penetration reaching 72%, and growing demand for scalable educational solutions across underserved communities. Brazil’s Connected Education Innovation Program and Mexico’s national digital literacy initiatives are accelerating adaptive platform adoption across public education systems.

Middle East & Africa — Growing Demand

The Middle East and Africa region presents expanding opportunities driven by Vision 2030 education reform initiatives in Saudi Arabia and UAE, growing EdTech investment in Sub-Saharan Africa, and increasing demand for scalable learning solutions to address teacher shortages. The UAE’s Mohammed bin Rashid Smart Learning Program and Saudi Arabia’s Education and Training Evaluation Commission are driving substantial investment in adaptive learning technologies.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- ASEAN Countries

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC Countries

- South Africa

- Rest of MEA

Market Value Chain Analysis

- AI & Data Infrastructure Providers: Cloud computing platforms, AI/ML framework developers, NLP engine providers, and data analytics vendors delivering foundational computing infrastructure, machine learning models, and data processing capabilities that power adaptive learning algorithms and real-time learner modeling systems.

- Adaptive Learning Platform Developers: Specialized edtech companies designing and developing adaptive learning engines, intelligent tutoring systems, content recommendation algorithms, knowledge tracing models, and learner analytics dashboards that transform educational content into personalized learning experiences at scale.

- Content Creators & System Integrators: Educational publishers, curriculum designers, instructional designers, and implementation partners creating adaptive-ready content, integrating platforms with LMS/SIS infrastructure, and ensuring alignment with accreditation standards, accessibility requirements, and institutional pedagogical frameworks.

- End-Use Learning Stakeholders: K-12 schools, universities, corporate L&D departments, government training agencies, and individual learners utilizing adaptive platforms to improve learning outcomes, accelerate skill acquisition, ensure compliance, and drive measurable educational and business performance improvements.

Top Adaptive Learning Software Market Companies

DreamBox Learning (Discovery Education)

DreamBox Learning leads the K-12 adaptive mathematics market with its Intelligent Adaptive Learning engine serving over 6 million students across 130,000 classrooms. The platform’s proprietary algorithm analyzes over 48,000 data points per student per hour to continuously personalize math instruction pathways.

Knewton (Wiley)

Knewton’s adaptive learning platform, now part of Wiley’s portfolio, provides AI-powered course material personalization across higher education and professional learning. The technology analyzes learner proficiency across granular knowledge components to recommend optimal content sequencing and practice activities.

McGraw Hill (ALEKS)

McGraw Hill’s ALEKS (Assessment and Learning in Knowledge Spaces) platform utilizes knowledge space theory and adaptive questioning to precisely map student knowledge states across STEM subjects, serving millions of learners in higher education with AI-driven personalized learning pathways.

Pearson (AI-Powered Learning)

Pearson is transforming from traditional publishing to an AI-first learning company, deploying adaptive learning capabilities across its global portfolio serving 750+ institutions. Its AI Study Tools and Pearson+ platform leverage generative AI for personalized study plans and conversational tutoring.

Other key players include Duolingo, Coursera, Area9 Lyceum, Carnegie Learning, Smart Sparrow (Pearson), Realizeit, Fishtree, CogBooks, Cerego, and Docebo, each focusing on specialized adaptive capabilities including language learning, enterprise training, competency-based education, and intelligent content recommendation.

| Company | Core Strength | Strategic Focus 2025–2026 |

|---|---|---|

| DreamBox Learning | K-12 Adaptive Math | Gen AI Tutoring & Multi-Subject Expansion |

| Knewton (Wiley) | Adaptive Courseware | Professional Learning & Certification Prep |

| McGraw Hill (ALEKS) | Knowledge Space Modeling | Predictive Analytics & Retention Tools |

| Pearson | Global Scale & Content | AI-First Platform Transformation |

| Duolingo | Gamified Language Adaptive | Multimodal AI & Video Lessons |

Recent Developments

- March 2025 — Pearson launched its next-generation AI Study Companion integrating GPT-powered conversational tutoring with real-time adaptive assessment, achieving 40% improvement in student concept mastery across pilot institutions.

- June 2025 — Duolingo introduced adaptive video lessons powered by multimodal AI, dynamically adjusting content difficulty and pacing based on learner comprehension signals and engagement patterns across 45 languages.

- September 2025 — McGraw Hill expanded ALEKS with predictive student success analytics, enabling institutions to identify at-risk learners 6 weeks earlier and deploy targeted adaptive interventions reducing course failure rates by 28%.

- January 2026 — DreamBox Learning launched its generative AI tutoring module enabling real-time personalized math explanations with natural language interaction, deployed across 15,000 elementary schools in the United States.

- February 2026 — Multiple enterprise learning platforms integrated adaptive skills assessment engines with HR talent management systems, enabling automated career pathing and personalized upskilling recommendations aligned to organizational competency frameworks.

Future Outlook 2030–2035

Between 2030 and 2035, the adaptive learning software market is expected to evolve into fully autonomous AI-driven learning ecosystems capable of orchestrating entire educational journeys with minimal human instructional intervention. The convergence of artificial general intelligence research, neuromorphic computing, brain-computer interface technologies, immersive extended reality learning environments, and decentralized credentialing systems will redefine educational paradigms globally.

As global learner populations expand toward 2.2 billion formal students and 4 billion professional learners by 2035, adaptive learning will become the foundational infrastructure of smart education systems supporting the projected market expansion to USD 28.24 billion by 2035. The integration of emotional AI for affective computing in learning, quantum computing for complex learner modeling, and blockchain-verified adaptive credentials will drive transformational growth across all educational sectors worldwide.