What is the Flywheel Energy Storage Systems Market Size?

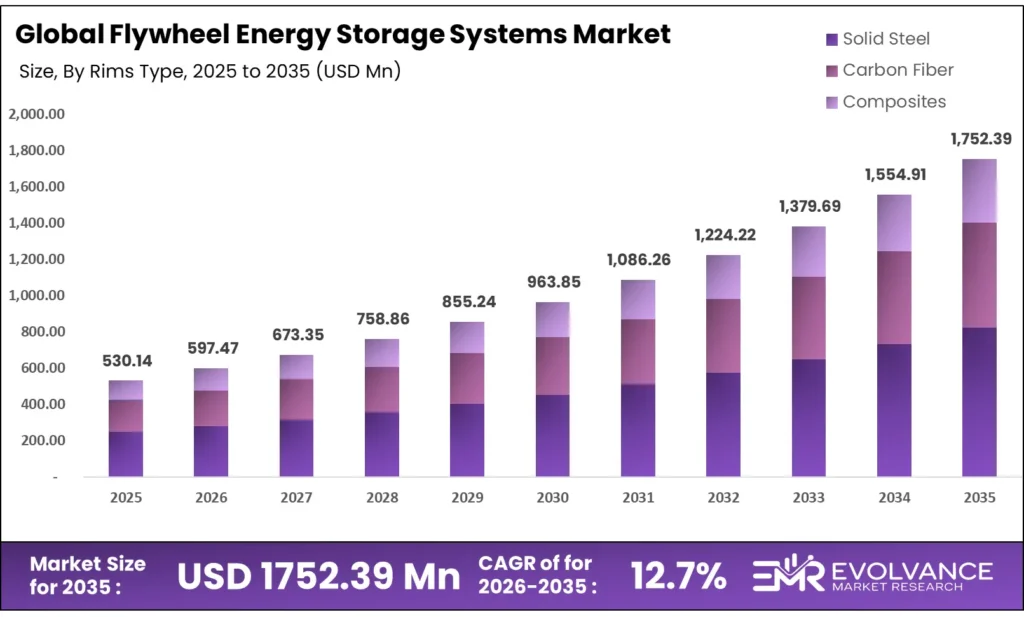

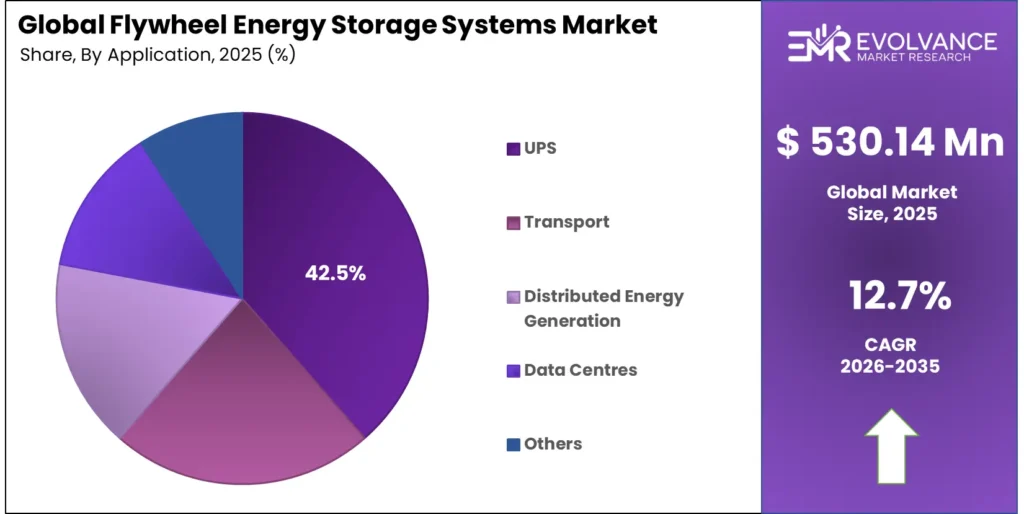

The Global Flywheel Energy Storage Systems Market size will be worth around USD 1,752.39 Million by 2035 from USD 530.14 Million in 2025, growing at a CAGR of 12.7% during the forecast period 2026 to 2035. Grid operators deploying solar and wind at scale need fast-response storage that lithium-ion cannot supply alone — a gap flywheel systems are built to fill. Buyers in data centers and utilities are shifting spend toward high-cycle, low-maintenance storage as uptime demands tighten. Supply constraints remain, with flywheel costs ranging from $1,500 to $6,000 per kWh, limiting adoption outside high-value frequency regulation use cases.

Market Highlights

- Global Flywheel Energy Storage Systems Market valued at USD 530.14 million in 2025, reaching USD 1,752.39 million by 2035 at a CAGR of 12.7%.

- North America dominates with 48.3% market share, valued at USD 256.0 million.

- By Rims Type, Solid Steel leads with 47.2% share in 2025.

- By Component, Flywheel Rotor holds the largest share at 51.2%.

- By Application, UPS holds the top position with 42.5% share.

Market Overview

Flywheel energy storage systems store electricity as kinetic energy using a spinning rotor. When power is needed, the rotor slows and converts motion back to electricity. This design delivers fast response times — measured in milliseconds — making it the preferred choice for frequency regulation in power grids and uninterruptible power supply systems in critical facilities.

The market spans solid steel and carbon fiber rim types, serving a range of end users from data centers to transport operators. Unlike chemical batteries, flywheels do not degrade with charge cycles, which gives them a strong total cost advantage over long operating lifetimes. This structural benefit is driving systematic evaluation by grid operators and industrial facility managers replacing legacy power protection equipment.

- According to the International Energy Agency, global installed electricity storage capacity reached approximately 160 GW of pumped-storage hydropower in 2021, representing more than 90% of total global electricity storage. This figure shows how concentrated legacy storage is in one technology — and highlights the structural opening for fast-response alternatives like flywheels as grids add variable renewables.

- Data from the International Energy Agency shows that global grid-scale battery storage capacity reached approximately 28 GW by end of 2022, after more than 11 GW of new capacity was added that year alone — a yearly growth rate exceeding 75%. This pace of storage deployment signals rising procurement budgets across the power sector, benefiting all storage technologies including flywheels that occupy a differentiated performance niche.

Government support is accelerating the market. The United States Department of Energy has issued Categorical Exclusions that allow flywheel energy storage projects to bypass lengthy environmental reviews, cutting development timelines. The 30 MW Dinglun flywheel project in China, connected to the grid in 2024, showed utilities globally that flywheel technology can be deployed at utility scale — removing a key adoption barrier.

Flywheel Energy Storage Systems Market Segmentation Insights

Rims Type Insights

Solid Steel dominates with 47.2% due to lower cost and broad industrial availability.

In 2025, Solid Steel held a dominant market position in the By Rims Type segment of the Flywheel Energy Storage Systems Market, with a 47.2% share. Solid steel rotors offer proven mechanical reliability at a lower material cost compared to advanced composites. Utilities and industrial buyers choosing flywheel UPS systems favor steel because it meets performance specs for short-duration grid services without requiring premium composite sourcing chains.

Carbon Fiber rotors serve performance-driven applications where weight reduction and higher rotational speed are critical. Carbon fiber delivers greater energy density per unit mass, enabling compact flywheel designs suited for aerospace, transport, and space-constrained data center installations. As production volumes rise and composite material costs fall, carbon fiber systems are positioned to take a larger share in high-specification segments over the forecast period.

Composites represent a hybrid approach, blending materials to balance cost and performance. Composite rim systems target mid-range applications where the peak speed of pure carbon fiber is not required but steel’s heavier mass creates design constraints. As flywheel makers push to lower system weight and extend cycle life, composite rim technology is drawing R&D investment from several European and Asian manufacturers.

Component Insights

Flywheel Rotor dominates with 51.2% due to its role as the core energy storage element.

In 2025, Flywheel Rotor held a dominant market position in the By Component segment of the Flywheel Energy Storage Systems Market, with a 51.2% share. The rotor is the primary energy-bearing part of any flywheel system — its mass, material, and spin rate determine the system’s total storage capacity and power output. Buyers upgrading or replacing flywheel systems drive consistent rotor demand, creating a recurring revenue stream for manufacturers beyond initial system sales.

Magnetic Bearings are a critical enabling component that eliminates friction losses in modern high-speed flywheel systems. By suspending the rotor magnetically, these bearings allow flywheels to spin at speeds exceeding 50,000 RPM with near-zero mechanical wear — a core reason flywheel systems outlast chemical alternatives in high-cycle environments. According to United States data, flywheel storage facilities achieve round-trip efficiency between 85% and 87%, a level largely enabled by low-loss magnetic bearing designs.

Motor-Generator units convert electrical energy into rotational kinetic energy during charging and reverse the process during discharge. The motor-generator is the interface between the flywheel and the power grid or facility load, and its efficiency directly sets the system’s round-trip performance. Advanced power electronics in motor-generator units are enabling faster grid response — a key competitive feature as grid operators tighten frequency regulation specs.

Application Insights

UPS dominates with 42.5% due to mission-critical power protection demand in data centers and hospitals.

In 2025, UPS held a dominant market position in the By Application segment of the Flywheel Energy Storage Systems Market, with a 42.5% share. Data centers, hospitals, and financial trading floors cannot tolerate even milliseconds of power interruption. Flywheel UPS systems provide seamless bridging power without the chemical degradation risk of battery UPS alternatives — a compelling argument for facility operators managing strict uptime SLAs. Langley Holdings plc, through its Piller Group subsidiary, generated €217.9 million in revenue in 2019 from flywheel-integrated UPS systems serving data centers and airports globally.

Transport applications use flywheels for regenerative braking energy recovery in rail, bus, and automotive systems. High-cycle endurance is the decisive advantage here — transit systems operating hundreds of brake-accelerate cycles per day destroy battery packs within years, while flywheels sustain performance indefinitely. Adoption in public transit is gaining pace as operators weigh total lifecycle costs over procurement price alone.

Distributed Energy Generation applications deploy flywheels to buffer power output from small-scale solar and wind installations connected to local microgrids. These behind-the-meter storage systems help industrial sites and remote communities manage generation variability without depending on grid infrastructure. As microgrid installations multiply globally, this segment offers a long-term volume opportunity for flywheel suppliers with compact, low-maintenance product lines.

Data Centres as a dedicated segment reflect the scale at which hyperscale and colocation operators now procure power infrastructure. Global data center electricity consumption is projected to reach 1,000 TWh by 2026, and every terawatt-hour of consumption raises the cost of downtime — increasing the economic case for premium flywheel UPS over standard battery alternatives. This trajectory makes data center operators one of the highest-value buyer cohorts in the flywheel market over the next decade.

Market Segments Covered in the Report

By Rims Type

- Solid Steel

- Carbon Fiber

- Composites

By Component

- Flywheel Rotor

- Magnetic Bearings

- Motor-Generator

- Others

By Application

- UPS

- Transport

- Distributed Energy Generation

- Data Centres

- Others

Regional Insights

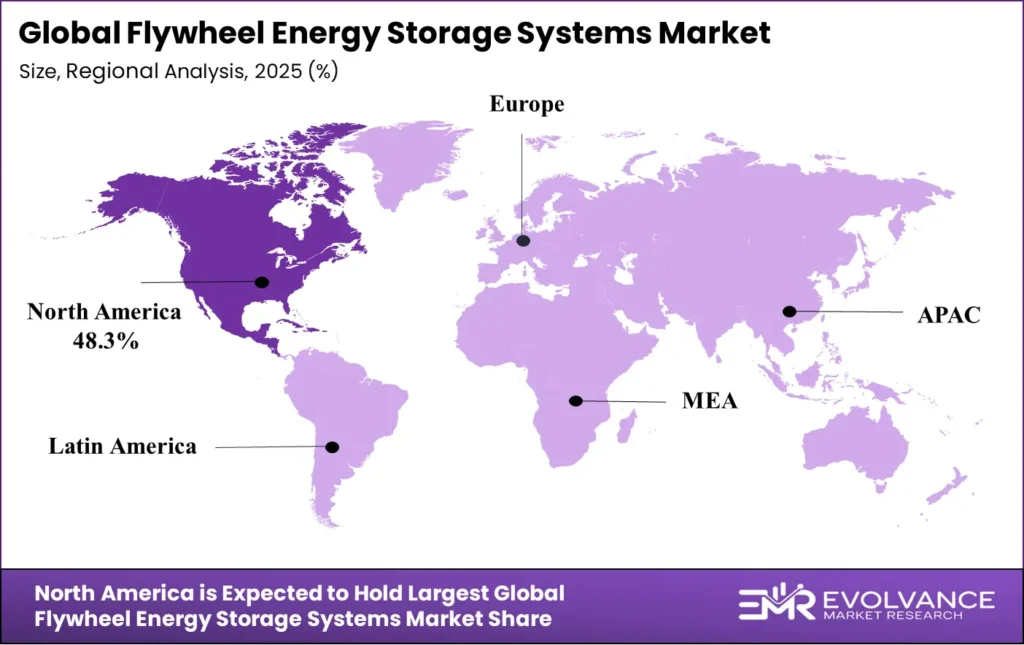

North America Dominates the Flywheel Energy Storage Systems Market with a Market Share of 48.3%, Valued at USD 256.0 Million

North America holds 48.3% of the global market, valued at USD 256.0 Million in 2025. This lead reflects decades of investment in frequency regulation infrastructure, with the United States operating at least five utility-scale flywheel projects totaling approximately 47 MW of capacity as of 2023. DOE policy support and mature grid ancillary service markets provide a commercial framework that accelerates private investment in flywheel deployment ahead of other regions.

Europe Flywheel Energy Storage Systems Market Trends

Europe is building momentum in flywheel adoption, driven by grid decarbonization targets and aggressive renewable energy integration across Germany, France, and the UK. European manufacturers including Stornetic GmbH and Adaptive Balancing Power GmbH are advancing commercial flywheel products for grid frequency markets. EU energy storage policy frameworks are pushing grid operators to diversify storage technology portfolios beyond batteries, opening procurement channels for flywheel suppliers.

Asia Pacific Flywheel Energy Storage Systems Market Trends

Asia Pacific is establishing itself as a high-growth deployment region. China’s 30 MW Dinglun flywheel project — the world’s largest flywheel facility — began operating in 2024 in Shanxi Province. This project proves utility-scale viability and gives Asia Pacific governments and utilities a domestic reference point for procurement decisions. China’s grid modernization spend and India’s renewable capacity build-out are creating volume opportunities for regional flywheel manufacturers.

Latin America Flywheel Energy Storage Systems Market Trends

Latin America is an early-stage market where energy storage adoption is tied to renewable energy project pipelines in Brazil and Mexico. Grid reliability challenges in parts of the region are creating demand for UPS-grade flywheel systems in industrial and commercial facilities. As Brazil expands its wind and solar capacity, the need for fast-response grid-support storage will create entry points for flywheel vendors targeting frequency regulation contracts.

Middle East & Africa Flywheel Energy Storage Systems Market Trends

The Middle East and Africa region presents a niche but growing market centered on data center power protection and off-grid industrial applications. GCC nations are investing in smart grid modernization as part of national energy diversification programs, creating demand for high-reliability storage. South Africa’s grid instability has accelerated interest in industrial UPS solutions, positioning flywheel systems as a premium alternative for mining and telecom operators facing frequent power outages.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The United States Department of Energy issued Categorical Exclusions for flywheel energy storage projects, removing the requirement for lengthy environmental impact assessments. This policy directly reduces project development timelines and lowers pre-construction costs for flywheel developers. For project sponsors, this means faster time-to-revenue and lower regulatory risk, making the US the most commercially accessible major market for utility-scale flywheel deployment.

- China’s National Energy Administration set grid-level energy storage deployment targets under its 2021-2025 five-year energy plan, mandating that renewable energy projects above a set capacity threshold include paired storage. This policy is directly driving utility-scale flywheel deployment in China, as demonstrated by the 30 MW Dinglun project commissioned in 2024. Similar storage mandates are being considered in South Korea and India, indicating a global regulatory shift that will expand the addressable flywheel market across Asia Pacific.

The Federal Energy Regulatory Commission (FERC) Order 841, finalized in 2018 and enforced through subsequent compliance filings, requires regional transmission organizations to open frequency regulation markets to all storage technologies. This rule removed a key market access barrier for flywheel operators. By treating flywheels equally with battery systems in ancillary service markets, FERC Order 841 created a commercial framework that supports long-term contract revenue for flywheel grid projects.

The European Union’s Battery Regulation, effective from 2024, sets lifecycle and supply chain standards specifically for electrochemical storage — but does not apply to mechanical storage. This regulatory distinction gives flywheel systems a compliance cost advantage over lithium-ion battery storage in EU markets. Grid operators seeking storage technologies with lower regulatory overhead are evaluating flywheels as a structurally simpler option alongside battery systems.

Flywheel Energy Storage Systems Market Dynamics

Drivers

Grid Operators Adding Renewable Capacity Need Millisecond-Response Storage That Chemical Batteries Cannot Reliably Provide

Solar and wind generation creates rapid power swings that threaten grid frequency stability. Flywheel systems respond in under 4 milliseconds — faster than any battery technology — making them the preferred solution for frequency regulation in grids with high renewable penetration. As renewable share rises globally, this performance gap becomes a procurement driver, not just a technical preference.

- The International Energy Agency data shows global grid-scale battery capacity hit 28 GW by end of 2022, with over 11 GW added in that year alone. This pace signals that utility buyers are actively expanding storage budgets across all technology types. Flywheel vendors positioned in frequency regulation markets benefit from this capital deployment cycle without directly competing with battery systems on energy duration.

The DOE’s Categorical Exclusion program for flywheel projects, combined with FERC Order 841’s equal market access mandate, gives US flywheel developers a clear regulatory path. This policy alignment means grid-scale flywheel projects can reach commercial operation faster in the US than in most other markets — a structural advantage that is pulling investment into North American deployments and establishing them as global reference cases.

Restraints

Capital Costs Between $1,500 and $6,000 per kWh Price Flywheel Systems Out of General Energy Storage Procurement

Flywheel energy storage carries a capital cost of $1,500 to $6,000 per kWh — significantly above the current installed cost of lithium-ion battery systems, which have fallen below $200 per kWh at utility scale in recent years. This cost gap limits flywheel adoption to applications where their performance advantages — cycle life, response speed, and maintenance profile — justify the premium. Buyers evaluating general-purpose storage will almost always choose batteries on a per-kWh cost basis.

The energy density gap further constrains the market. Flywheel systems are optimized for high-power, short-duration discharge — typically under 30 seconds. This makes them unsuitable for applications requiring sustained energy delivery over hours, such as overnight solar backup or multi-hour peak shaving. Buyers with mixed storage needs must combine flywheels with longer-duration technologies, adding system complexity and total project cost.

However, this restraint is partially self-limiting. In high-cycle environments — where a storage system charges and discharges hundreds of times per day — flywheel’s near-zero degradation gives it a lower total cost of ownership over a 20-year operating life than any battery chemistry currently available. The challenge for flywheel vendors is getting procurement teams to evaluate lifecycle cost rather than upfront capital cost.

Growth Factors

Data Center Power Consumption Reaching 1,000 TWh by 2026 Turns Flywheel UPS Into a High-Volume Procurement Category

Global data center electricity consumption is projected to reach 1,000 TWh by 2026. Every facility in that base requires power protection, and the cost of a single unplanned outage — measured in lost transactions, SLA penalties, and reputational damage — dwarfs the premium cost of flywheel UPS over battery alternatives. This economics shift is making flywheel UPS a standard specification in hyperscale and colocation facility design, not a premium option.

Hybrid energy storage systems combining flywheels with batteries are creating a new market category. Flywheels handle the high-frequency regulation and short-burst power needs while batteries manage longer duration storage. This architecture delivers better total system performance than either technology alone. Vendors offering integrated hybrid systems — including Amber Kinetics and VYCON — are positioned to capture a broader slice of utility and industrial storage budgets than flywheel-only product lines.

Additionally, the NREL West Gate Program supported KineticCore Solutions in 2025 to develop low-cost long-duration flywheel designs. Federal R&D backing of this kind accelerates commercialization timelines and validates the technology for institutional buyers who require government endorsement before committing to new storage platforms. Successful NREL-backed projects typically attract follow-on private capital, strengthening the commercialization pipeline for next-generation flywheel systems.

Emerging Trends

AI Integration and the World’s Largest Flywheel Project Signal a Commercial Maturity Shift in the Market

The 30 MW flywheel facility in Shanxi, China — the largest in the world — became operational in 2024, demonstrating that flywheel technology can be scaled to utility-grade capacity. This project removes the “unproven at scale” objection that has slowed utility procurement globally. Grid operators in Europe, South Korea, and Australia are now watching this facility as a reference case for their own storage tender processes.

AI-driven energy management systems are being integrated into commercial flywheel deployments as of 2024. These platforms optimize charge-discharge cycles in real time, predict maintenance needs before failures occur, and interface with grid management systems for automated frequency regulation bidding. The addition of AI management significantly improves the commercial return on flywheel assets by maximizing the hours they participate in ancillary service markets.

Furthermore, Torus Nova Spin was named to TIME’s Best Inventions list, marking a moment when advanced flywheel technology entered mainstream commercial recognition. This type of public validation accelerates enterprise buyer awareness and shortens sales cycles. Flywheel systems achieve round-trip efficiency between 85% and 87% — a figure that AI-optimized dispatch can push further toward the top of that range in high-cycle grid applications.

Key Companies Insights

Langley Holdings plc is the market’s largest integrated flywheel power systems group, operating through its Piller Group subsidiary to serve data centers, airports, and industrial facilities globally. The company reported record profit before tax of €152.3 million in FY2025, up from €125.4 million in FY2024 — a performance that reflects both strong demand for flywheel UPS systems and Langley’s ability to deliver at scale from its 18 production facilities across Europe, the UK, and the US. With net assets exceeding €1 billion and an order backlog of €930 million at end of FY2024, Langley holds a balance sheet advantage that smaller flywheel rivals cannot match when competing for large facility contracts.

Amber Kinetics, Inc. is advancing steel flywheel technology for long-duration grid storage, a segment most flywheel vendors have not addressed. Its M32 system targets four-hour discharge durations — extending the flywheel use case well beyond traditional frequency regulation into peak shaving and renewable firming markets. This product positioning creates a direct competitive overlap with battery storage in a market segment where flywheel’s cycle life and environmental profile are strong advantages. Amber Kinetics’ technology has been deployed in utility-scale pilot projects, establishing commercial reference points for buyers evaluating grid storage diversification.

Adaptive Balancing Power GmbH targets the European industrial and grid frequency regulation market with compact flywheel systems designed for behind-the-meter and grid-edge installations. The company’s focus on modular system architecture allows customers to scale capacity incrementally — a procurement model that reduces upfront capital commitment and lowers adoption risk for first-time flywheel buyers. As European grid operators face increasing renewable variability, Adaptive Balancing Power’s regionally-focused product line and engineering support model position it well to capture frequency regulation contracts in Germany and neighboring markets.

VYCON, Inc. specializes in flywheel UPS and power conditioning systems for data centers, healthcare facilities, and defense installations. Its VDC series products are deployed in mission-critical environments where battery replacement cycles create unacceptable downtime and hazardous material disposal costs. VYCON’s go-to-market strategy targets facility managers who have experienced battery failures and are willing to pay a premium for a maintenance-free alternative. This focus on proven, high-reliability reference installations has built VYCON a differentiated reputation in the North American data center power protection market.

Key Companies

- Langley Holdings plc

- Amber Kinetics, Inc.

- Adaptive Balancing Power GmbH

- VYCON, Inc.

- Teraloop

- Stornetic GmbH

- Revterra

- PUNCH Flybrid

- Levistor Ltd

- Energiestro

- Candela (Shenzhen) New Energy Technology Co., Ltd.

- Bc New Energy (Tianjin) Co., Ltd. (BNE)

- Beacon Power, LLC

- Kinetic Traction Systems, Inc.

- Dumarey Group

Recent Development

- In February 2026 – Langley Holdings plc reported record profit before tax of €152.3 million for FY2025, up from €125.4 million in FY2024. The result reflects strong order flow for flywheel UPS and industrial power systems across global markets.

- In 2025 – KineticCore Solutions received support from the NREL West Gate Program to develop low-cost long-duration flywheel designs. Federal backing signals institutional validation of next-generation flywheel technology beyond short-duration frequency regulation.

- In 2024 – The world’s largest flywheel energy storage facility, rated at 30 MW, became operational in Shanxi Province, China. The Dinglun project connects to the national grid and serves as a global reference for utility-scale flywheel deployment.

- In 2024 – AI-driven management and cybersecurity solutions began integration into commercial flywheel systems. Vendors deploying these platforms are enabling automated participation in grid ancillary service markets, improving asset revenue generation.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 530.14 Million |

| Forecast Revenue (2035) | USD 1,752.39 Million |

| CAGR (2026-2035) | 12.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Rims Type (Solid Steel, Carbon Fiber, Composites), By Component (Flywheel Rotor, Magnetic Bearings, Motor-Generator, Others), By Application (UPS, Transport, Distributed Energy Generation, Data Centres, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Langley Holdings plc, Amber Kinetics, Inc., Adaptive Balancing Power GmbH, VYCON Inc., Teraloop, Stornetic GmbH, Revterra, PUNCH Flybrid, Levistor Ltd, Energiestro, Candela (Shenzhen) New Energy Technology Co. Ltd., Bc New Energy (Tianjin) Co. Ltd. (BNE), Beacon Power LLC, Kinetic Traction Systems Inc., Dumarey Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |