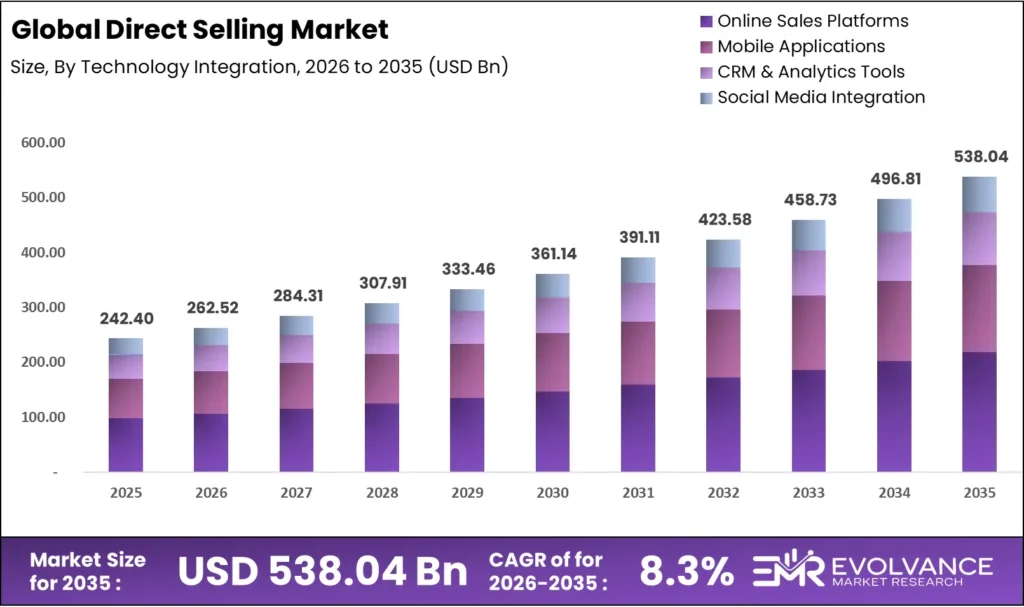

Direct Selling Market: $242B in 2025 to $538B by 2035

The global direct selling market size will reach USD 538.04 billion by 2035 from USD 242.40 billion in 2025, growing at a CAGR of 8.3% during the forecast period 2026 to 2035. Health and wellness product demand, rising micro-entrepreneurship in emerging markets, and digital platform adoption among independent sales representatives drive this expansion.

Subscription-based ordering models are reshaping buyer behavior across the sector. USANA Health Sciences reported that its auto-order program accounted for 63% of product sales volume in 2024, showing how recurring purchase mechanics lock in retention and smooth revenue cycles. Supply-side risks include intensifying regulatory oversight — the U.S. Federal Trade Commission proposed its “Earnings Claim Rule” in January 2025 — and financial stress among legacy brands, as Tupperware filed for Chapter 11 bankruptcy in September 2024.

Direct Selling Market Highlights: Key Data at a Glance

- Market size 2025: USD 242.40 billion, forecast to reach USD 538.04 billion by 2035 at an 8.3% CAGR

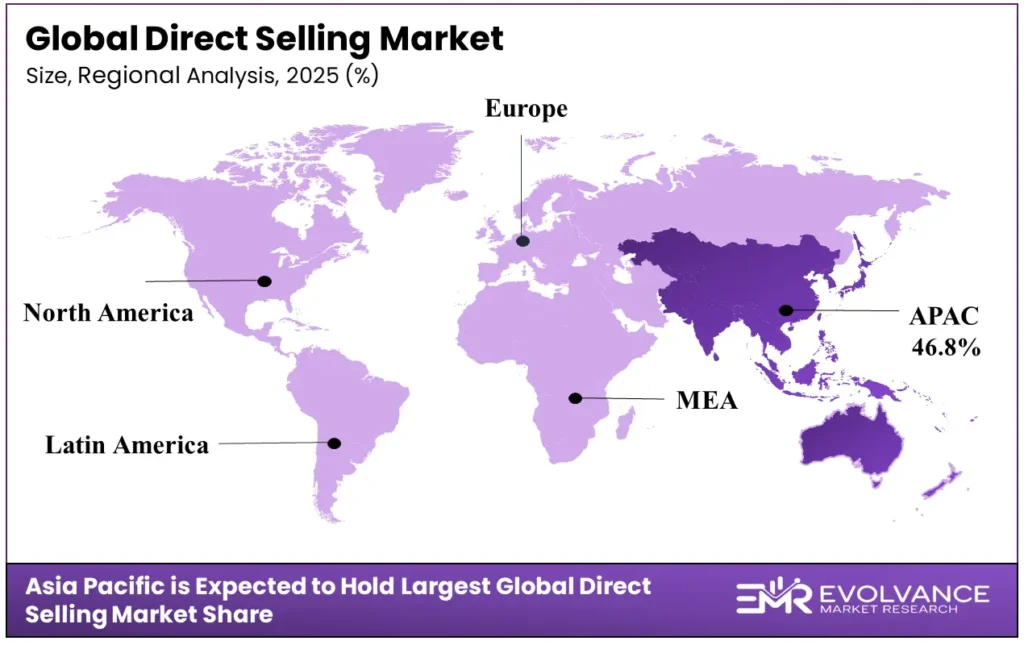

- Dominant region — Asia Pacific: 46.8% share valued at USD 111.26 billion, home to 62.3 million independent representatives in 2024

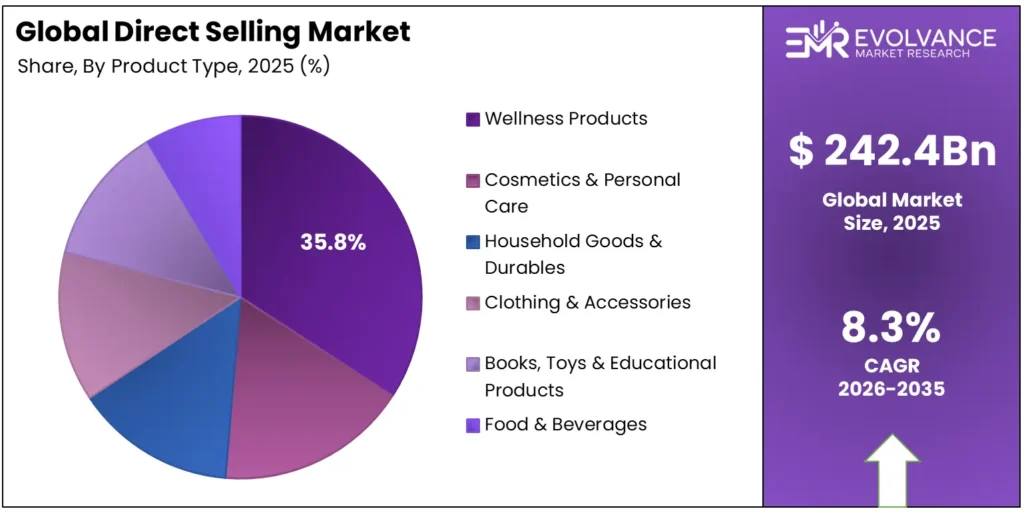

- Dominant segment — Health & Wellness: 35.3% of global revenue, led by Herbalife, reporting net sales growth of 6.3% in Q4 2025

- Leading method — Multi-Level Marketing (MLM): 59.6% of the market by type, anchored by Amway, Herbalife, and PM-International

- Top company by revenue: Amway at USD 7.4 billion in 2024, ranking first on the Global 100 list with 59 companies generating nearly USD 64 billion combined

- Digital shift: 79% of organizations adopted direct online selling channels in 2025; Oriflame processed 99% of orders via online platforms in 2024

- Workforce growth: Sales representatives aged 55 and older rose from 21% to 28% of the total workforce in 2024, marking a structural demographic shift

What Is the Direct Selling Market and How Does It Work

The direct selling market encompasses all commerce where products or services are sold face-to-face, through personal networks, or via digital platforms outside of fixed retail locations. Sales occur through independent representatives who earn commissions rather than through traditional store channels, making the model accessible to entrepreneurs at low startup cost.

This analysis consolidates data from company SEC filings, World Federation of Direct Selling Associations (WFDSA) statistical reports, Direct Selling News Global 100 rankings, and individual brand annual reports covering fiscal year 2024 and 2025. evolvance market research analysts covered 5 regions and 6 segment groups to produce a forecast grounded in both published financial disclosures and trade association data. For buyers evaluating this market — whether for investment, entry, or procurement — the breadth of source coverage matters because no single public database captures all revenue streams across informal and digital channels simultaneously.

The sector traces its modern roots to door-to-door sales models of the early 20th century, but the arrival of MLM structures in the 1950s and 1960s fundamentally changed recruitment economics. Personal care, nutrition, and household goods dominated early growth. By 2025, the model spans financial services, real estate, digital subscriptions, and AI-powered wellness tools, with companies like eXp Realty applying it to property brokerage at USD 4.6 billion in 2024 revenue.

Buyer behavior in this market is relationship-driven at its core. Independent representatives serve dual roles as customers and distributors, meaning retention of productive sellers directly equals customer retention. According to the WFDSA, Asia/Pacific alone had 62.3 million independent representatives in 2024, up 3.4% from 2023, reflecting how digital connectivity and women’s workforce participation sustain seller supply even where retail sales flatten.

Direct Selling Market Dynamics: Drivers, Risks, and Trends

India and Mexico Offset North America Declines in 2024

Global market stabilization became visible in 2024 as a 4.6% improvement in average market growth rates masked diverging regional trajectories. According to the World Federation of Direct Selling Associations (WFDSA), India posted a 4.0% retail sales increase to USD 3.528 billion, while Mexico grew 2.6% to USD 6.842 billion. These gains partially offset the 5.2% contraction in the United States, which still represents the single largest national market at USD 34.74 billion.

Health & Wellness Demand Pushes Segment to 35.3% Revenue Share

Consumer demand for specialized wellness products has made health and wellness the dominant segment at 35.3% of global revenue. As reported by Herbalife Nutrition Ltd. in its annual SEC filing, net sales grew 6.3% in Q4 2025 and its preferred member base reached 3.0 million as of December 31, 2024. Amway’s nutrition category grew 2% to represent 64% of its USD 7.4 billion total 2024 revenue, showing how wellness concentration is deepening at the top of the market.

Older Demographics Drive Micro-Entrepreneurship Workforce Growth

Micro-entrepreneurship attraction among older demographics is redefining the sales force. Based on data from the Direct Selling Association (DSA), global sales representatives aged 55 and older increased from 21% to 28% of the total workforce in 2024. This cohort brings established personal networks and lower turnover rates. The shift matters for operators because older representatives tend to generate higher average order values and qualify at higher plan tiers faster than younger cohorts.

Domestic Manufacturing Policies Strengthen Supply Chain Resilience

Domestic production investments are reducing supply chain exposure for leading brands. As confirmed by Amway in its 2025 newsroom release, the company marked 10 years of “Make in India” manufacturing, a strategic hedge against global logistics disruptions and tariff volatility. Combined with a $12 million commitment to new store infrastructure and R&D in India through 2026, the company is treating the subcontinent as both a manufacturing base and a primary revenue growth engine simultaneously.

FTC Earnings Claim Rule Raises Compliance Cost for All U.S. Operators

Federal regulatory oversight intensified in January 2025 when the FTC proposed its “Earnings Claim Rule,” requiring written substantiation and three-year record-keeping for all income claims. This directly raises compliance costs for the roughly 6.2 million Herbalife members and tens of millions of representatives across U.S.-based MLM operators. Herbalife had already accumulated USD 161.6 million in cumulative restructuring and compliance pre-tax expenses through 2024.

Tupperware Bankruptcy Signals Legacy Brand Fragility

Tupperware Brands Corporation filed for Chapter 11 bankruptcy in September 2024, closing plants and exiting markets after prolonged financial underperformance. As documented in U.S. bankruptcy court records, the sale of its IP and core assets to a lender consortium was approved for USD 23.5 million cash plus USD 63 million in debt forgiveness in October 2024. The collapse illustrates that a globally recognized brand cannot survive on legacy distribution models alone when sales force engagement and product relevance deteriorate together.

India Entry and D2C Channels Open High-Value Growth Opportunities

South Asian market expansion has become a primary revenue engine. As per Nu Skin Enterprises investor communications, the company prepared for a significant market pre-opening in India scheduled for Q4 2025, while Amway committed USD 12 million to India infrastructure through 2026. Separately, findings from the DSA Growth & Outlook Survey show 79% of organizations adopted direct online selling channels in 2025, integrating D2C models to enhance margins and reach customer segments outside the traditional representative network entirely.

Consumer Trust in Direct Selling Rose 21% Since 2019

Consumer trust in the direct selling industry rose 21% compared to 2019 levels, according to 2025 DSA Growth & Outlook results. This recovery matters because trust is the single largest barrier to first-time buyer conversion in relationship-driven commerce. In our view, the trust rebound reflects both sustained product quality investment at the top of the market and the departure of lower-credibility operators during the post-pandemic correction cycle — leaving a cleaner competitive field for established brands.

AI Tools and Social Commerce Accelerate Digital Maturation

Digital ecosystem maturation accelerated as Nu Skin deployed its AI-driven “Vera” and “Stella” apps to enable data-driven personalization and social commerce in 2025. Oriflame processed approximately 99% of total orders via online platforms in 2024, up from 95% in 2023, while mobile devices drove 69% of those orders. The gap between digitally native operators and traditional door-to-door models is now widening at a pace that structural laggards cannot close through events alone.

Subscription Models and FTC Negative Option Rule Reshape Repeat Purchases

Subscription-based delivery models gained dominance in 2024 as major players integrated recurring revenue systems. Vorwerk’s Cookidoo platform reached 5.5 million subscribers by end of 2024, up 17% from 4.7 million in 2023. The FTC’s new “Negative Option Rule,” effective May 2025, mandates “click-to-cancel” mechanisms for all recurring purchase programs — adding compliance friction but simultaneously validating subscription models as mainstream enough to warrant federal consumer protection frameworks.

Direct Selling Market Segmentation Analysis by Product and Method

By Product Type: Health and Wellness Leads at 35.3%

| Sub-segment | Share % | Primary driver |

|---|---|---|

| Health & Wellness | 35.3% | Post-COVID nutrition and supplement demand |

| Cosmetics & Personal Care | — | Social commerce and beauty influencer adoption |

| Household Goods & Durables | — | Emerging market demand and the Vorwerk appliance model |

| Clothing & Accessories | — | Social selling via personal stylist networks |

| Books, Toys & Educational Products | — | Parent-network referral in developing markets |

| Food & Beverages | — | Subscription meal kit and consumables integration |

| Financial Services | — | Insurance and wealth management via a representative model |

Health & Wellness dominates with 35.3% share due to rising chronic disease rates, nutritional deficiency trends, and sustained post-COVID consumer spending on preventive care. As stated in Herbalife Nutrition Ltd. SEC filings, Asia Pacific net sales reached USD 1,723.8 million in 2024, while data from the Amway newsroom confirms its nutrition category alone accounted for 64% of total revenue.

Cosmetics & Personal Care is the second product pillar, with brands like Oriflame and Nu Skin driving social commerce conversion. Nu Skin reported wellness and beauty together represented 84.7% of its USD 1.49 billion 2025 revenue, confirming that personal care and wellness are effectively fused in the highest-revenue product portfolios. IoT integration in personal care — such as Nu Skin’s ageLOC LumiSpa iO device — is linking hardware sales to recurring consumable subscriptions.

Household Goods & Durables operates through the premium direct-sales appliance model exemplified by Vorwerk. According to the Vorwerk Group Annual Report 2024, Thermomix revenue held at EUR 1,717.4 million in 2024 despite European consumer restraint, supported by an advisor base exceeding 100,000 globally. The segment’s high ticket values and attached subscription services — Cookidoo at 5.5 million subscribers — make it structurally different from consumables-led categories.

Financial Services represents a fast-growing non-physical category. Figures from the Direct Selling News Global 100 show Primerica generated USD 3.07 billion in 2024 direct sales revenue, ranking seventh globally, while World Financial Group reached USD 1.5 billion. The representative model maps well to insurance and investment products because trust-based relationships are the primary conversion mechanism in financial services as well.

By Type / Method: MLM Commands 59.6% of the Market

| Sub-segment | Share % | Primary driver |

|---|---|---|

| Multi-Level Marketing (MLM) | 59.6% | Network recruitment, economics, and passive income appeal |

| Single-Level Marketing (SLM) | — | Simplicity, compliance, safety, and direct consumer access |

| Party Plan System | — | Social proof and group purchase behavior |

| Door-To-Door Selling | — | High-touch premium product demonstrations |

| Vending and Direct Sales | — | Convenience channel integration |

Multi-Level Marketing dominates with 59.6% share because the downline recruitment model creates compounding distribution networks that scale faster than single-representative models. The top MLM operators — Amway, Herbalife, and PM-International — collectively generate over USD 15 billion annually. However, MLMs’ dominance also attracts the heaviest regulatory attention, particularly the FTC’s January 2025 Earnings Claim Rule proposal targeting income representations.

Single-Level Marketing offers a structurally simpler compliance profile. Representatives earn commissions only on personal sales rather than on downline activity, making earnings claims easier to substantiate. The rise of D2C digital selling has blurred the line between SLM and direct e-commerce — 79% of organizations adopting online selling channels in 2025 are effectively operating SLM structures in their digital channels, regardless of their overall compensation plan architecture.

By End-User, Distribution Channel, Selling Plan, and Technology Integration

| Sub-segment | Share % | Primary driver |

|---|---|---|

| Individual Customers | — | Personal network trust and convenience |

| Commercial Customers | — | B2B wellness and services procurement |

Individual Customers represent the overwhelming end-user base, driven by personal relationships with independent representatives. As per Herbalife Nutrition Ltd. SEC filings, its preferred member count reached 3.0 million as of December 31, 2024, within a total of 6.2 million members — showing how the consumables loyalty structure converts buyers into recurring subscribers rather than one-time purchasers.

Independent Sales Representatives remain the primary distribution channel, but Online/Digital Platforms and Social Commerce are closing the gap rapidly. As noted in the Oriflame Annual Report 2024, referral-link registrations via social media reached nearly 20% in 2024. Data from Nu Skin Enterprises press releases confirms 129,311 paid affiliates via personal social networks in Q4 2025 — showing social commerce is now a structural distribution channel, not an experimental one.

AI-Driven Sales Optimization leads the technology integration segment. As documented in Herbalife Nutrition Ltd. SEC filings, the company invested a cumulative USD 330 million in its Herbalife One digital platform by December 31, 2024, integrating CRM, analytics, and distributor management. Nu Skin’s Vera and Stella AI apps and Oriflame’s Business app — with 207,000 monthly active users — represent the front line of AI deployment at the representative level.

Key Market Segments

By Product Type

- Health & Wellness

- Cosmetics & Personal Care

- Household Goods & Durables

- Clothing & Accessories

- Books, Toys & Educational Products

- Food & Beverages

- Financial Services

By Type / Method

- Multi-Level Marketing (MLM)

- Single-Level Marketing (SLM)

- Party Plan System

- Door-To-Door Selling

- Vending and Direct Sales

By End-User

- Individual Customers

- Commercial Customers

By Distribution Channel

- Independent Sales Representatives

- Online/Digital Platforms

- Social Commerce

By Selling Plan

- Binary Plan

- Unilevel Plan

- Matrix Plan

- Hybrid Plan

- Monoline Plan

- Board Plan

By Technology Integration

- AI-Driven Sales Optimization

- Cloud-Based Downline Management

- Automated Commission Systems

Direct Selling Regional Analysis: Asia Pacific Leads at 46.8%

Asia Pacific Direct Selling Market: 46.8% Share, USD 111.26 Billion

Asia Pacific commands the largest share at 46.8%, valued at USD 111.26 billion. According to the World Federation of Direct Selling Associations (WFDSA), the region reached USD 66.058 billion in 2024 with 62.3 million independent representatives, representing 59.8% of the global total. Eight billion-dollar national markets anchor the region’s structural lead — no other region approaches this depth of multi-country scale.

As per data published by the WFDSA, China generated USD 15.546 billion in 2024, up 5.0%, as regulatory easing ahead of the 2025 anniversary of direct sales resumption restored operator confidence. Korea posted USD 15.065 billion despite a 3.5% decline, while Malaysia reached USD 10.197 billion at the highest GDP penetration rate globally at 2.417%. India grew 4.0% to USD 3.528 billion, with Amway and Nu Skin both committing new market infrastructure investments through 2026.

North America Direct Selling Market: Largest Single Country, Structural Decline

Research by the WFDSA confirms the United States remains the single largest national market at USD 34.74 billion in 2024, though that represents a 5.2% decline from 2023. Combined with Canada’s USD 2.189 billion (down 5.6%), North America totaled USD 36.929 billion, reflecting post-pandemic consumer and sales force adjustments. The Americas region posted a -2.8% CAGR from 2021 to 2024, the steepest decline of any region.

Figures from the WFDSA show Brazil grew 6.3% to USD 7.844 billion and Mexico expanded 2.6% to USD 6.842 billion, showing Latin America increasingly offsetting North American weakness. Argentina posted a nominal surge of 310.1% to USD 2.362 billion, driven by 220% inflation rather than real volume growth — a data point investors must discount when reading headline Americas growth figures.

Europe Direct Selling Market: USD 35.352 Billion with Six Billion-Dollar Markets

As noted by the WFDSA, Europe reached USD 35.352 billion in 2024, accounting for 21.6% of the global total, though the region declined 1.5% year-over-year. Germany — the region’s largest market at USD 19.05 billion — fell 5.2%, reflecting broad macroeconomic pressure on discretionary spending. The region posted a 0.2% CAGR from 2021 to 2024, the only positive multi-year trend outside Asia Pacific.

Data published by the WFDSA shows France held near flat at USD 4.714 billion (+0.1%), supported by new market entrants, while Italy posted USD 2.930 billion with a marginal 1.1% decline. As per the Oriflame Annual Report 2024, Europe and CIS sales reached EUR 324.1 million in 2024, with member counts down 5% year-over-year, illustrating the dual pressure of economic headwinds and platform-driven consolidation across the region.

Africa/Middle East Direct Selling Market: USD 1.265 Billion, Largest Regional Decline

According to the WFDSA, Africa/Middle East reached USD 1.265 billion in 2024, representing only 0.8% of the global total and declining 5.9% from 2023. The region posted a -7.8% CAGR from 2021 to 2024 — the steepest multi-year contraction globally. Modest gains in Israel and the UAE contrasted with broader declines across sub-Saharan Africa. No billion-dollar national market exists in this region, limiting its near-term weight in global competitive strategy.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Top Direct Selling Companies: Revenue and Strategy 2024–2025

The direct selling industry is highly concentrated at the top. According to Direct Selling News, 59 companies on the Global 100 generated nearly USD 64 billion combined in 2024, with the top five — Amway, Herbalife, eXp Realty, Natura &Co, and Vorwerk — accounting for roughly USD 25.3 billion of that total. The battle lines are drawn between legacy nutrition brands defending volume share and new-model operators like eXp using the direct sales structure in non-traditional categories.

We believe the most underappreciated competitive dynamic in this landscape is the divergence between brands investing heavily in digital platforms — Herbalife’s cumulative USD 330 million in its Herbalife One system — and those relying on event-based and community recruitment models. That capital allocation gap will compound over the next five years as AI personalization tools widen the conversion rate differential between digitally equipped and manually operated sales forces.

Amway leads the global market with USD 7.4 billion in 2024 revenue, though that figure declined 3% from 2023 due to currency effects. The nutrition category — its strategic core — grew 2% to 64% of total sales. The company’s dual focus on domestic manufacturing through “Make in India” and a USD 12 million India infrastructure commitment positions it for growth in the market most analysts expect to become the next USD 10 billion direct selling country.

Herbalife ranked second at USD 5 billion in 2024 revenue. As reported in its SEC annual filing, new distributors worldwide increased 22% year-over-year in Q4 2024, marking three consecutive quarters of growth, and its sales leader re-qualification rate improved to 70.3% for the twelve-month period ending January 2025. These metrics suggest the distribution base is stabilizing, though USD 218.3 million in interest expense in 2024 — up from USD 165.9 million in 2023 — reflects the financing cost of that rebuild.

Note: The 6.3% net sales growth referenced in the Market Highlights section refers to Herbalife’s Q4 2025 performance, distinct from the 2024 annual figures discussed here.

Natura &Co ranked fourth at USD 4.2 billion in 2024 direct sales revenue. As announced in March 2025, the company executed a recapitalization through its Oriflame subsidiary, reducing EUR 520 million of debt and securing a EUR 50 million equity injection from founding family investors. Oriflame’s operational metrics show full digital transition — 99% of orders processed online — but declining member counts in Europe and CIS present a near-term volume challenge.

Vorwerk ranked fifth at USD 4.1 billion. Data from the Vorwerk Group Annual Report 2024 shows total group revenue held at EUR 3,171.8 million in 2024, with the Thermomix advisor base exceeding 100,000 globally, up 6.6% on average from 2023. The Kobold vacuum division saw revenue decline 9.7% to EUR 776.7 million, revealing that premium appliance direct sales face distinct headwinds from consumer restraint that the subscription-anchored Thermomix model has so far avoided.

eXp World Holdings ranked third at USD 4.6 billion, applying the direct sales agent model to real estate brokerage. PM-International ranked sixth at USD 3.22 billion, opening a new Tallinn, Estonia office in February 2026 as part of planned new subsidiaries in Kazakhstan, Czech Republic, India, Vietnam, and Ireland. Primerica at USD 3.07 billion and Coway at USD 3.0 billion round out the top tier, each operating in non-traditional direct sales categories — financial services and water purification, respectively.

Nu Skin Enterprises generated USD 1.73 billion in full-year 2024 revenue; its full-year 2025 revenue fell to USD 1.49 billion. As per Nu Skin’s Q4 2025 press release, sales leaders declined 19% year-over-year to 30,045 and Mainland China customers fell 21% to 118,523. The company’s Rhyz diversification segment fell 22.0% to USD 223.6 million in 2025, while operating margin recovered to 6.3% in Q4 2025 through cost discipline rather than top-line growth.

As documented in USANA Health Sciences SEC filings, the company generated USD 854.5 million in 2024 revenue. Its December 2024 acquisition of direct-to-consumer brand Hiya for USD 206.161 million added subscription automation capability, with Asia Pacific representing 79.5% of its 454,000 active customers. Atomy reached USD 1.83 billion and operates a value-focused MLM model distinct from the premium positioning of Herbalife and Nu Skin.

Top Key Players

- Amway

- Natura &Co

- Herbalife

- eXp World Holdings Inc.

- Vorwerk

- PM-International

- Primerica

- Coway

- Nu Skin Enterprises Inc.

- Atomy

Direct Selling Market: Key Developments from 2024 to 2026

In February 2026, soccer star Cristiano Ronaldo invested USD 7.5 million in Herbalife’s digital nutrition platform Pro2col, acquiring a 10% equity stake in the subsidiary. The investment signals that celebrity-backed digital wellness ventures are now a viable direct selling growth vector — and marks a direct challenge to social-commerce-native brands competing for younger demographics through influencer channels.

In January 2026, Betterware de México (BeFra) agreed to acquire Tupperware’s Latin American business — focused on Mexico and Brazil — for USD 250 million, including a perpetual royalty-free license to the Tupperware brand in the LATAM region. The deal reflects how Tupperware’s October 2024 bankruptcy created acquisition opportunities for regional operators to absorb established brand equity without the legacy debt structure that caused the original collapse.

In March 2025, Herbalife announced plans to acquire digital wellness platform Pro2col Health and ketone supplement company Pruvit Ventures outright, plus a 51% stake in biotech firm Link BioSciences, for a combined USD 25–30 million. This cluster of acquisitions marks a deliberate move toward science-backed product lines and subscription-compatible digital tools — directly addressing the category credibility gap that the FTC’s compliance environment now demands of large MLM operators.

In June 2025, MONAT Global completed a record-breaking launch in Germany — its strongest-ever market debut — as part of an aggressive European expansion. That same month, Oriflame expanded its “Personalised Wellness Pack” subscription into the Czech Republic and Romania after a Spanish pilot. Both moves confirm that Western Europe, despite headline market contraction, still attracts new entrant capital from brands with differentiated models.

Related Direct Selling Markets Worth Tracking

The direct selling market does not operate in isolation. Country-level regulatory environments, demographic growth rates, and category-specific product demand create distinct sub-markets that require independent analysis for operators, investors, and procurement teams making entry or expansion decisions.

Key Related Markets

- US Direct Selling Market

- China Direct Selling Market

- India Direct Selling Market

- Germany Direct Selling Market

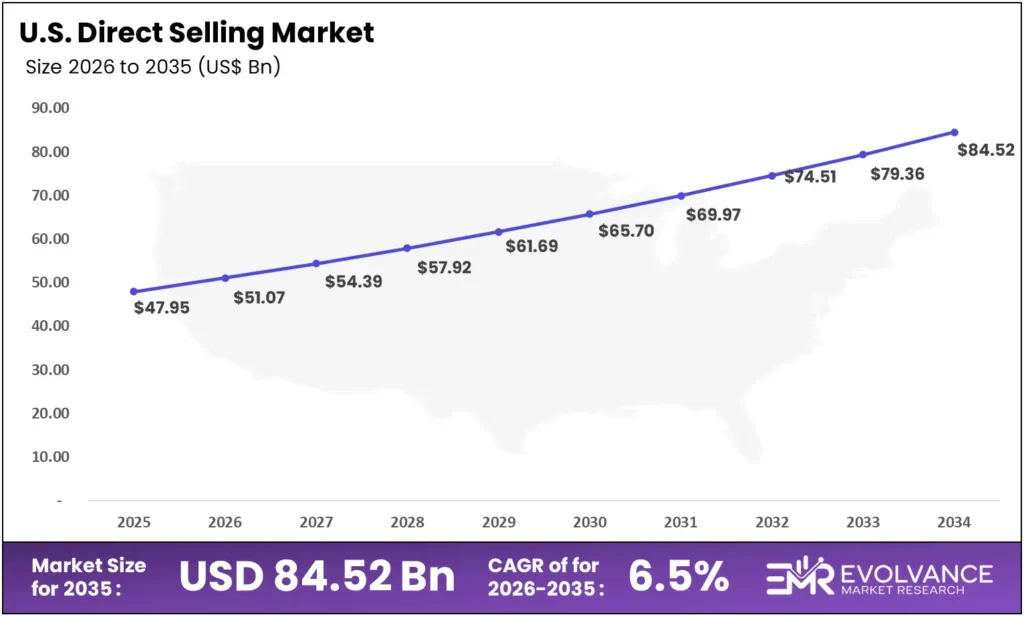

US Direct Selling Market: USD 47.95B to USD 84.52B at 6.5% CAGR

The US direct selling market is the single largest national market by value, even as it faces structural contraction. According to the WFDSA, United States direct sales retail sales totaled USD 34.74 billion in 2024, a 5.2% decline from 2023, representing 56.8% of the Americas region. Post-pandemic consumer behavior normalization and declining sales force participation have driven multi-year contraction despite the country hosting the world’s largest MLM operators by revenue.

While 2024 actual retail sales stood at USD 34.74 billion, the forecast base of USD 47.95 billion for 2025 and target of USD 84.52 billion by 2035 at a 6.5% CAGR reflects recovery potential tied to digital channel adoption, regulatory stabilization post-FTC rule implementation, and the demographic shift toward older micro-entrepreneurs. The FTC’s January 2025 Earnings Claim Rule will increase compliance costs for operators but simultaneously clean out lower-credibility participants — raising average earnings per active representative and improving the sector’s consumer trust profile in the medium term.

Domestic manufacturing policy and India-linked supply chain shifts matter for U.S. operators because cost structures for nutrition and personal care products are increasingly tied to non-domestic production. As stated in the Amway U.S. Income Disclosure Statement, IBOs with product sales averaged USD 1,199 in annual earnings before expenses in 2024 — a figure that constrains recruitment arguments unless supported by strong community events and digital training tools.

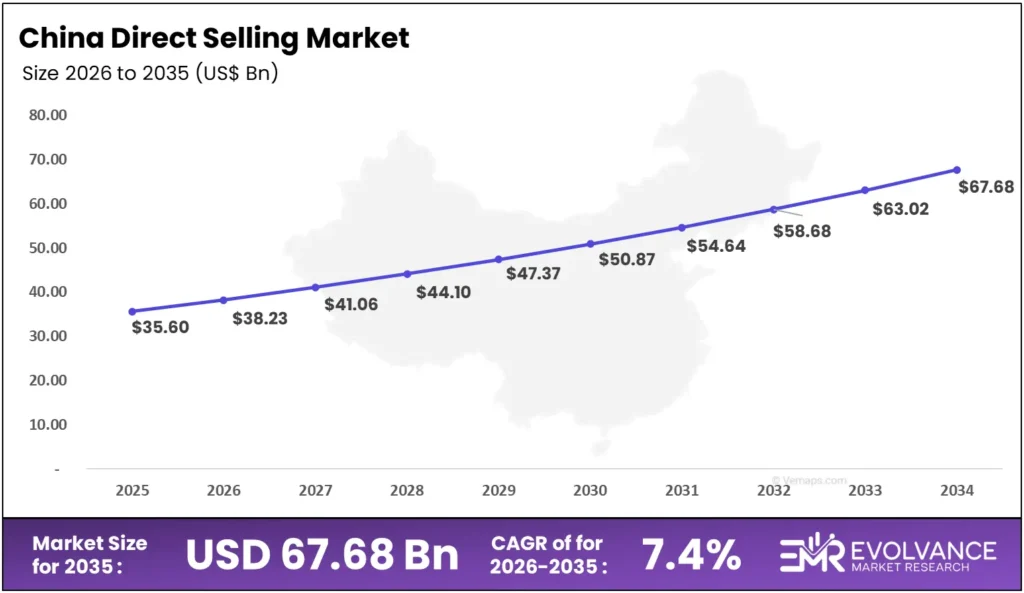

China Direct Selling Market: USD 35.60B to USD 67.68B at 7.4% CAGR

China is the second-largest national direct selling market globally and a critical growth lever for all major operators. As documented by the WFDSA, China direct sales retail sales totaled USD 15.546 billion in 2024, a 5.0% increase from 2023, representing 23.5% of the Asia/Pacific region. Regulatory easing ahead of the 2025 anniversary of direct sales resumption drove the improvement after years of tighter enforcement following the 2019 “Hundred-Day Action” crackdown.

While 2024 actual retail sales stood at USD 15.546 billion, the forecast base of USD 35.60 billion for 2025 and target of USD 67.68 billion by 2035 at a 7.4% CAGR reflects optimism about regulatory normalization and middle-class wellness demand. However, risks remain concentrated. As per Nu Skin Enterprises’ Q4 2025 press release, Mainland China customer count fell 21% to 118,523, showing how regulatory environment shifts can rapidly deflate even established operator metrics. Brands with diversified Asia Pacific footprints — Korea, Taiwan, and Malaysia providing buffer — are better positioned than those with concentrated China exposure.

India Direct Selling Market: USD 14.2B to USD 31.81B at 8.4% CAGR

The India direct selling market is the fastest-growing major national market and the most strategically important entry target for global operators through 2030. Figures from the WFDSA show India direct sales retail sales totaled USD 3.528 billion in 2024, growing 4.0% from 2023 and representing 5.3% of the Asia/Pacific region. While 2024 actual retail sales stood at USD 3.528 billion, the forecast base of USD 14.2 billion for 2025 and target of USD 31.81 billion by 2035 at an 8.4% CAGR implies India will become one of the world’s top three direct selling markets within the forecast period.

Direct selling is legal in India under the Consumer Protection (Direct Selling) Rules, 2021, which established the first formal regulatory framework distinguishing legitimate direct sales from pyramid schemes. The rules mandate registration, return policies, and maximum entry fees, providing the compliance clarity that global operators need before committing capital. Over 6 million registered direct sellers operate in India as of 2025, with Vestige, Mi Lifestyle, Modicare, and Amway among the most active domestic and international brands.

Amway committed USD 12 million to new store infrastructure and R&D in India through 2026, marking 10 years of local manufacturing. Nu Skin prepared a significant India market pre-opening for Q4 2025. Both investments reflect a structural bet that India’s combination of entrepreneurial culture, young demographics, and growing middle-class wellness spending will produce a demand curve that mirrors China’s 2010–2020 direct selling expansion — but with a more stable regulatory foundation from the outset.

Germany Direct Selling Market: USD 18.2B to USD 32.29B at 5.9% CAGR

Germany anchors the European direct selling market as its single largest national contributor, though 2024 data showed continued pressure. WFDSA figures confirm Germany direct sales retail sales totaled USD 19.05 billion in 2024, a 5.2% decline from 2023, representing 53.9% of the Europe region’s total. The concentration of European revenue in Germany means any sustained German contraction drags continental figures regardless of performance in France, Italy, or Eastern Europe.

While 2024 actual retail sales stood at USD 19.05 billion, the forecast base of USD 18.2 billion for 2025 and target of USD 32.29 billion by 2035 at a 5.9% CAGR reflects Germany’s structural strengths — high household income, strong consumer protection trust in regulated direct sellers, and deep market penetration of premium appliance brands like Vorwerk. MONAT Global’s record-breaking June 2025 Germany launch confirms the market still attracts new capital despite headline decline. Recovery will depend on whether digital onboarding tools can reactivate the lapsed representative base faster than macroeconomic headwinds suppress new recruiter interest.

Direct Selling Market Scope and Report Coverage

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 242.40 Billion |

| Forecast Revenue (2035) | USD 538.04 Billion |

| CAGR (2026–2035) | 8.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Dominant Region | Asia Pacific with 46.8% share valued at USD 111.26 Billion |

| Dominant Segment | Health & Wellness with 35.3% share |

| Leading Method | Multi-Level Marketing (MLM) with 59.6% share |

| Segments Covered | By Product Type, By Type/Method, By End-User, By Distribution Channel, By Selling Plan, By Technology Integration |

| Regional Analysis | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Competitive Landscape | Amway, Natura &Co, Herbalife, eXp World Holdings Inc., Vorwerk, PM-International, Primerica, Coway, Nu Skin Enterprises Inc., Atomy |

| Regulatory Framework | FTC Earnings Claim Rule (proposed January 2025), FTC Negative Option Rule (effective May 2025), India Consumer Protection (Direct Selling) Rules 2021 |

| Data Sources | WFDSA Statistical Reports, Direct Selling News Global 100, Company SEC Filings, Brand Annual Reports |