What is the Potassium-ion Battery Market Size?

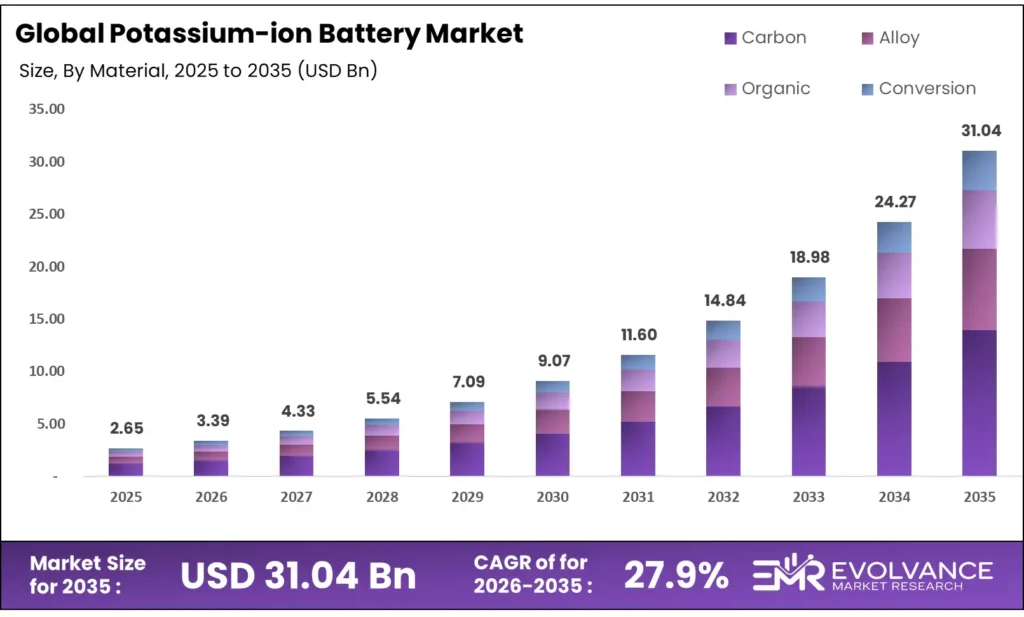

The Global Potassium-ion Battery Market size will be worth around USD 31.04 Billion by 2035 from USD 2.65 Billion in 2025, growing at a CAGR of 27.9% during the forecast period 2026 to 2035. Cathode breakthroughs and hard carbon anode scale-up are pulling this market from lab stage into early commercial reality. Enterprise buyers in grid storage are shifting spend toward non-lithium options as battery prices fall to USD 80-90/kWh. Supply chain risk tied to electrolyte compatibility remains a near-term constraint that vendors must resolve before wide deployment.

Market Highlights

- Global Potassium-ion Battery Market valued at USD 2.65 Billion in 2025, forecast to reach USD 31.04 Billion by 2035 at a CAGR of 27.9%.

- North America leads all regions with a 45.3% market share, valued at USD 1.2 Billion.

- Rechargeable batteries dominate By Battery Type with a 61.2% share.

- Prismatic cell format leads By Cell Format with a 47.5% share.

- Carbon anode material holds the top position in By Anode Material with a 42.3% share.

- The >10 MW–50 MW capacity band leads By Capacity with a 49.1% share.

- Consumer Electronics leads By Application with a 41.6% share.

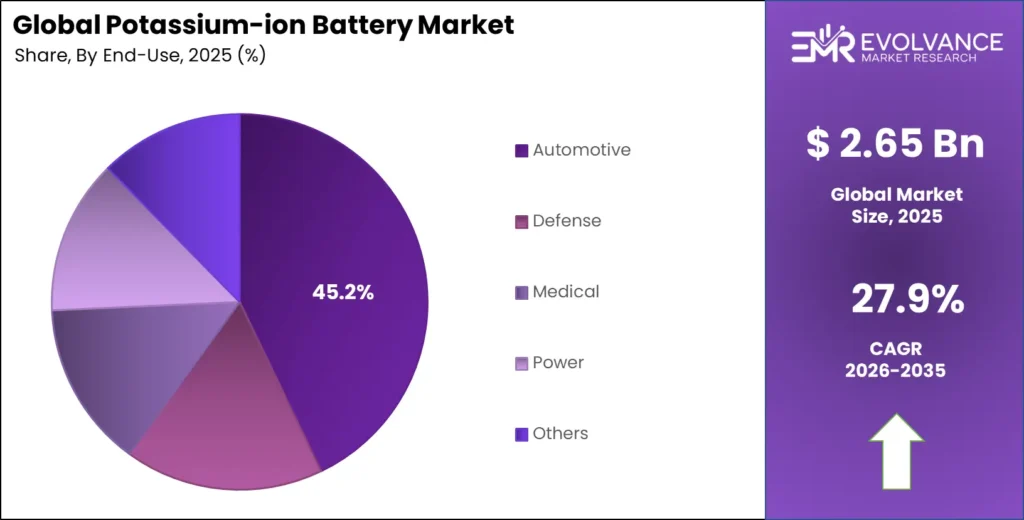

- Automotive leads By End-use with a 45.2% share.

Market Overview

Potassium-ion batteries (KIBs) store energy by moving potassium ions between anode and cathode. They use abundant, low-cost potassium — not scarce lithium — as the active ion. This cost advantage is the market’s core appeal. Vendors and researchers are targeting grid storage and low-cost consumer devices as the first commercial entry points.

The technology shares structural traits with lithium-ion cells. Manufacturers can adapt existing lithium-ion production lines with modest changes. This lowers the barrier to entry for battery makers already operating at scale. However, KIBs still trail lithium-ion on energy density — a gap that determines which applications adopt first.

Grid storage and stationary energy systems are the clearest near-term opportunity. The 2024 EU Critical Raw Materials Act raised strategic interest in potassium as a supply chain alternative to lithium. India’s Ministry of New and Renewable Energy launched KIB storage pilots in 2024, testing viability in renewable integration projects. These government signals tell investors that policy tailwinds are forming before the market scales.

According to the IEA, global EV battery demand reached 750 GWh in 2023, a 40% year-over-year rise, and was on track to surpass 1 TWh in 2025. This scale tells us the addressable base for alternative chemistries is large and expanding fast — KIB developers do not need to displace lithium-ion to build a significant business.

Based on data from Oxford Energy, the U.S. invested approximately USD 2.6 Billion in domestic mineral projects in 2024 while USD 43.6 Billion went toward battery production — a ratio that shows infrastructure investment far outpaces upstream supply. For KIB, this means the commercial window depends less on mining scale and more on proving cell performance at the factory level.

Battery Type Insights

Rechargeable batteries dominate with 61.2% due to grid and EV cycle-life demand.

In 2025, Rechargeable batteries held a dominant market position in the By Battery Type segment of the Potassium-ion Battery Market, with a 61.2% share. Buyers in grid storage and automotive applications need cells that deliver thousands of charge cycles. A 2024 peer-reviewed study published in Nature Energy confirmed over 2,000 stable cycles for potassium-ion cells — directly validating rechargeable KIB viability for these high-cycle-demand buyers. This data point closes a key credibility gap that had kept enterprise procurement teams cautious.

Non-rechargeable batteries serve single-use and low-power device segments where cost per use — not cycle life — drives buying decisions. Medical sensors, remote monitoring hardware, and low-drain consumer items are natural fits. This segment holds smaller share but carries stable demand because it faces no cycle-life performance hurdle. KIB’s cost advantage over lithium primaries is a clear sell in price-sensitive categories.

Cell Format Insights

Prismatic format dominates with 47.5% due to structural fit with automotive and stationary storage pack designs.

In 2025, Prismatic cells held a dominant market position in the By Cell Format segment of the Potassium-ion Battery Market, with a 47.5% share. Automotive OEMs and grid storage integrators prefer prismatic formats because they pack efficiently into flat modules and simplify thermal management. In August 2024, Group1 launched the world’s first commercial KIB in 18650 cylindrical format — but the prismatic format’s lead reflects where procurement volumes are anchored in existing energy storage systems.

Cylindrical cells are the format of choice for consumer electronics and portable tools. The 18650 standard is deeply embedded in supply chains. Group1’s commercial KIB launch in cylindrical format shows that vendors are targeting this segment first, where tooling and production lines already exist. Early commercial traction here can fund the R&D needed to push into larger format markets.

Pouch cells offer the highest energy density per unit weight and are favored in compact, weight-sensitive applications. Wearable devices, drones, and thin portable devices drive pouch demand. For KIB, pouch format development lags behind because electrolyte sealing and swelling management are harder to solve — but research teams targeting dendrite-free anodes via artificial SEI engineering are laying the groundwork for pouch adoption.

Anode Material Insights

Carbon anodes dominate with 42.3% due to maturity, low cost, and compatibility with potassium-ion chemistry.

In 2025, Carbon anodes held a dominant market position in the By Anode Material segment of the Potassium-ion Battery Market, with a 42.3% share. Hard carbon is the most tested and produced anode material for KIBs. Shanxi Guorun expanded industrial-scale hard carbon production in 2024 specifically targeting KIB commercialization — a direct supply chain signal that carbon anode supply is being built ahead of cell-level demand to reduce a key bottleneck.

Alloy anodes offer higher theoretical capacity than carbon but suffer from volume expansion during cycling. Research is active but alloy anodes are not yet production-ready for KIB at scale. Buyers who need higher energy density will watch this space, but adoption depends on solving mechanical degradation — a problem that materials scientists have not yet resolved commercially.

Conversion anodes rely on chemical reactions rather than intercalation. They deliver high initial capacity but degrade faster. Academic groups are publishing on conversion materials, but the performance gap versus carbon makes commercial adoption unlikely in the near term. This segment remains in the research phase and will not compete for share until cycle stability improves substantially.

Organic anodes are the earliest stage option. They offer unique structural flexibility and potential for bio-derived production. However, organic anodes for KIB are at proof-of-concept stage. Their value proposition — low cost and green sourcing — aligns with ESG-driven procurement trends, but they need years of development before matching carbon anode performance standards.

Capacity Insights

The >10 MW–50 MW band dominates with 49.1% due to utility-scale pilot and early commercial project sizing.

In 2025, the >10 MW–50 MW capacity range held a dominant market position in the By Capacity segment of the Potassium-ion Battery Market, with a 49.1% share. Grid operators and utilities are commissioning storage projects in this range as they test alternative chemistries at meaningful scale without committing to hundred-megawatt deployments.

The International Renewable Energy Agency’s 2024 cost modeling showed non-lithium storage options could offer price advantages in post-2025 deployments — giving utility buyers a financial justification to pilot KIB in this mid-range capacity tier.

Up to 10 MW capacity systems serve commercial and industrial buyers who need on-site storage for demand management or backup power. These are typically smaller facilities, data centers, or manufacturing plants. This tier is where first-mover KIB vendors are most likely to win early contracts because the capital commitment is lower and the performance bar is easier to clear.

>50 MW–100 MW represents utility-scale storage with serious grid stabilization roles. Projects in this band require demonstrated reliability data that KIB cannot yet fully provide. However, as pilot projects in the >10 MW–50 MW tier generate performance records, procurement teams will gain the confidence to move into this larger tier by the late forecast period.

>100 MW is the domain of national grid operators and large-scale renewable energy parks. These projects have long procurement cycles and demand proven technology with multi-year track records. KIB will not compete in this tier until well into the 2030s. Vendors should not target this segment now — but winning >10 MW–50 MW contracts today builds the reference portfolio needed to reach it.

Application Insights

Consumer Electronics dominates with 41.6% due to high unit volumes and tolerance for lower energy density.

In 2025, Consumer Electronics held a dominant market position in the By Application segment of the Potassium-ion Battery Market, with a 41.6% share. Smartphones, tablets, laptops, and wearables run on batteries where cost per cell matters more than maximum energy density.

KIB’s cost advantage over lithium-ion aligns directly with the cost pressure consumer electronics OEMs face. Battery prices fell to approximately USD 80-90/kWh in 2024 due to lithium-ion overcapacity — and KIB developers must price below this benchmark to displace incumbents even in cost-sensitive segments.

Electric Vehicles represent the largest long-term revenue opportunity but the hardest near-term application. EV buyers and OEMs demand high energy density, fast charging, and proven cycle life. Data from Argonne National Laboratory in 2024 confirmed KIB’s lower gravimetric energy density versus commercial lithium-ion — a gap that must close before automakers seriously evaluate KIB for mainstream vehicles. EV adoption of KIB is a later-decade story.

Energy Storage Systems for grid and industrial use are the most strategically aligned application for KIB’s cost profile. Stationary storage does not penalize weight, removing KIB’s main weakness. The Stanford University and U.S. battery startup collaboration in 2024 targeting fast-charging KIB cells below 15-minute charge time directly enhances this application’s commercial readiness.

Portable Devices include power tools, medical equipment, and rugged field instruments. These buyers prioritize reliability and cost over peak energy density. This segment gives KIB vendors a path to commercial revenue while energy density improvements continue. Early wins in portable devices fund ongoing R&D without requiring full performance parity with lithium-ion.

Power Grids require the most rigorous performance standards of any application. KIB’s long-cycle stability — now confirmed above 2,000 cycles — makes grid applications viable for vendor discussions, even if full commercial deployment is years away. Vendors who engage grid operators now will be positioned when procurement decisions accelerate post-2027.

End-use Insights

Automotive end-use dominates with 45.2% due to the scale of EV investment and battery supply chain activity.

In 2025, Automotive held a dominant market position in the By End-use segment of the Potassium-ion Battery Market, with a 45.2% share. Auto manufacturers and their Tier 1 suppliers are investing in next-generation battery research to reduce lithium dependency. CATL, which holds a 37.9% global EV battery share and operates 646 GWh of annual production capacity, has the financial base — including RMB 97 Billion in operating cash flow in 2024 — to fund alternative chemistry pilot lines including KIB.

Defense end-users are evaluating KIB for field power systems where supply chain independence and thermal stability matter more than energy density. Group1’s November 2025 MOU with Michigan Potash and Salt Company specifically targeted defense applications, recognizing that military buyers pay premium prices for proven supply chain security. This is one of the first commercial deals to explicitly link KIB to defense procurement.

Medical devices require long shelf life, stable discharge curves, and regulatory compliance. KIB’s cost advantage is secondary here — reliability and safety certifications drive procurement. However, non-rechargeable KIB variants could compete in implantable and wearable medical sensors where replacing a lithium primary cell with a lower-cost potassium alternative delivers a clear economic case without performance compromise.

Power utilities and energy companies are the end-users most aligned with KIB’s grid storage potential. China Datang Corporation’s inauguration of a 100 MWh sodium-ion storage project in Hubei Province in June 2024 — a closely related alternative chemistry — shows that Asian utilities are actively commissioning non-lithium grid storage. KIB developers can use this market momentum as a template for their own utility engagement strategies.

Others covers telecommunications backup, data center UPS, and agricultural energy systems. Group1’s November 2025 MOU targeted data center UPS specifically — a segment with nearly USD 7 Trillion in projected capital spending by 2030. Positioning KIB as a UPS solution for data centers gives vendors access to one of the fastest-spending infrastructure categories in the global economy.

Market Segments Covered in the Report

By Battery Type

- Rechargeable

- Non-rechargeable

By Cell Format

- Prismatic

- Cylindrical

- Pouch

By Anode Material

- Carbon

- Alloy

- Conversion

- Organic

By Capacity

- Up to 10 MW

- >10 MW–50 MW

- >50 MW–100 MW

- >100 MW

By Application

- Consumer Electronics

- Electric Vehicles

- Energy Storage Systems

- Portable Devices

- Power Grids

- Others

By End-use

- Automotive

- Defense

- Medical

- Power

- Others

Potassium-ion Battery Market Regional Insights

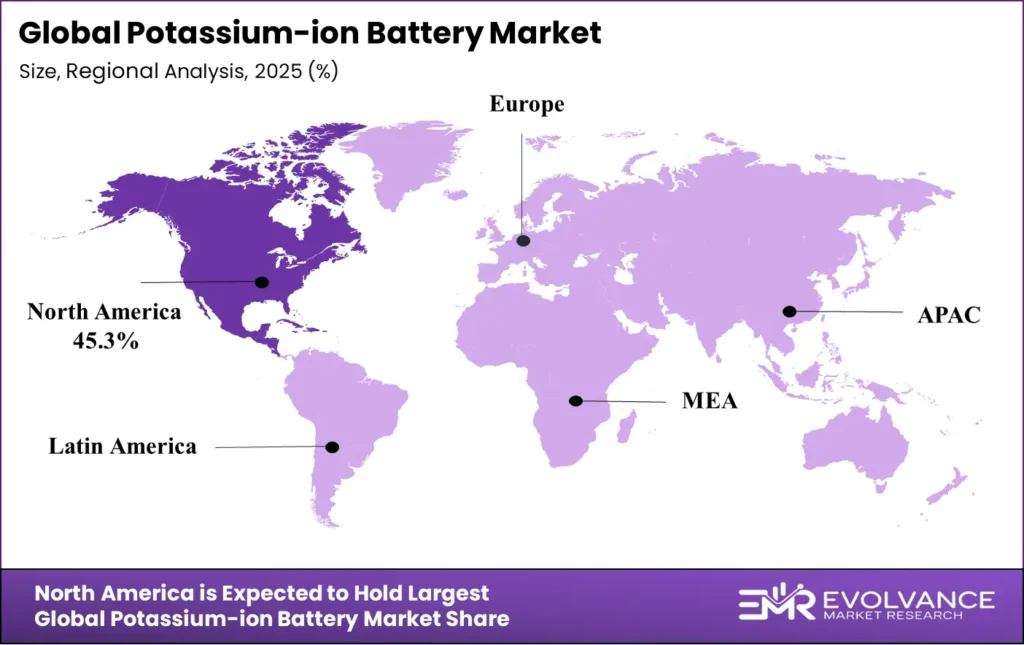

North America Dominates the Potassium-ion Battery Market with a Market Share of 45.3%, Valued at USD 1.2 Billion

North America holds a 45.3% share valued at USD 1.2 Billion in 2025. The U.S. federal government’s USD 43.6 Billion battery production investment and the DOE’s KIB-specific funding — including USD 2.6 Million to Project K — have created a funded research pipeline that no other region matches at this stage. This policy-backed infrastructure gives U.S. startups like Group1 a commercialization advantage that Europe and Asia have not yet replicated for KIB specifically.

Europe Potassium-ion Battery Market Trends

Europe’s position is defined by the 2024 EU Critical Raw Materials Act, which made potassium-rich alternatives a strategic procurement priority. Sweden’s Altris AB, backed by Clarios International and Volvo Cars Tech Fund, received SEK 150 Million in Series B1 funding in 2024 plus SEK 77 Million from the Swedish Energy Agency — confirming that European institutional capital is backing next-generation battery chemistry at the pilot plant level.

Asia Pacific Potassium-ion Battery Market Trends

Asia Pacific is the most active region for alternative battery production investment. China planned 48 alternative battery storage projects in 2024 with combined capacity of 254.7 GWh and total investment of CNY 126.77 Billion. The Chinese Academy of Sciences published a 160 Wh/kg KIB prototype result in 2024. South Korea and China together led global KIB patent filings in 2024, per WIPO data — signaling where deep R&D investment is concentrated.

Latin America Potassium-ion Battery Market Trends

Latin America is an emerging region for KIB in the context of renewable energy build-out. Brazil and Mexico are expanding solar and wind capacity, creating demand for low-cost stationary storage. Potassium is abundant in Latin American mineral deposits, giving the region a potential supply chain advantage if local battery production develops. However, no significant KIB-specific investment has been confirmed in the region as of the current data period.

Middle East & Africa Potassium-ion Battery Market Trends

The Middle East and Africa region is investing in energy diversification through large-scale solar projects. GCC countries are funding grid modernization, and off-grid storage in Sub-Saharan Africa represents a cost-sensitive segment where KIB’s price advantage matters most. However, the region lacks local battery manufacturing, and technology adoption will depend on imports from Asia and Europe until domestic production capacity is established.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The 2024 EU Critical Raw Materials Act directly targets supply chain security for battery minerals. The Act classifies potassium among resources of strategic interest — giving KIB a regulatory endorsement that lithium-based chemistries cannot claim as a differentiator. European battery makers now have a policy mandate to explore KIB as part of their supply chain risk reduction strategy.

In the United States, the 2024 DOE Long-Duration Storage funding expansion included support for alternative-ion chemistries. This funding round allocated capital toward non-lithium battery research, with KIB systems explicitly included. Federal R&D support of this kind reduces commercial risk for early-stage KIB developers and attracts private capital alongside government grants.

India’s Ministry of New and Renewable Energy launched KIB pilot storage programs in 2024, providing government support for grid-scale tests. India’s regulatory push reflects its dual goal of expanding renewables and reducing import dependence on lithium. These pilots, if successful, will generate the real-world performance data that accelerates procurement decisions across the Asia Pacific region.

China’s battery industry operates under national industrial policy that directs capital toward domestic production of all battery chemistries. The 2024 planned investment of CNY 126.77 Billion across 48 alternative battery projects reflects a state-backed approach to building production infrastructure before market demand fully materializes — a strategy that gives Chinese KIB producers a cost and scale advantage over western competitors.

Potassium-ion Battery Market Dynamics

Drivers

Cathode Cycle-Life Breakthroughs and Federal Funding Accelerate KIB Commercial Readiness

The 2024 Nature Energy publication confirming over 2,000 stable cycles for potassium-ion cells removed the most cited technical objection from enterprise buyers. Cycle life has been the primary reason grid storage procurement teams excluded KIB from shortlists. This result changes the conversation from “if KIB can work” to “when it will be cost-competitive.”

The U.S. DOE’s 2024 Long-Duration Storage funding expansion added KIB to its list of supported alternative-ion chemistries. Federal backing at this stage does two things: it validates the technology for private investors, and it funds the trial projects that generate commercial reference data. Both outcomes pull the commercialization timeline forward by reducing financial risk for early adopters.

Moreover, the Chinese Academy of Sciences reported a KIB prototype achieving 160 Wh/kg energy density in 2024 — a level comparable to LFP lithium-ion, which dominates grid storage globally. When a KIB cell matches LFP on energy density while offering a cost-of-materials advantage, the procurement calculus for grid storage operators shifts decisively. This benchmark is the single most important data point for the market’s near-term growth trajectory.

Restraints

Lower Energy Density and Electrolyte Instability Limit Early Adoption in High-Performance Applications

Argonne National Laboratory’s 2024 comparative data confirmed that KIB cells deliver lower gravimetric energy density than commercial lithium-ion benchmarks. For EV buyers who require maximum range per kilogram, this is not a marginal gap — it is a disqualifying one. Until KIB closes this gap, the automotive segment — the market’s largest end-use at 45.2% — remains largely inaccessible to KIB vendors.

A 2024 study in the Journal of Power Sources identified accelerated degradation in high-voltage potassium cells linked to electrolyte incompatibility. High-voltage operation is required for many grid and automotive applications. Electrolyte formulation that survives high-voltage cycling without decomposing is an unsolved materials science problem — and one that limits how broadly KIB can be deployed until resolved.

Consequently, vendors face a difficult near-term positioning challenge. They must prove commercial viability in lower-voltage, lower-density applications — consumer electronics and stationary backup — while simultaneously funding research to solve the high-voltage electrolyte problem. Companies that cannot fund both tracks in parallel risk losing market share to sodium-ion alternatives, which face similar but further-advanced commercialization paths.

Growth Factors

Supply Chain Policy Shifts and Academic-Industry Collaboration Open New Revenue Channels for KIB

The EU Critical Raw Materials Act of 2024 created a policy environment where using potassium — a non-critical, abundantly available mineral — signals supply chain intelligence to regulators and investors. European battery manufacturers who adopt KIB can credibly claim reduced supply chain risk. This regulatory advantage translates directly into procurement preference among sustainability-focused buyers and ESG-driven institutional investors.

The Stanford University and U.S. battery startup collaboration announced in 2024 targets KIB cells capable of charging in under 15 minutes. Fast-charging is a market-defining capability that unlocks EV and consumer electronics applications simultaneously. If this collaboration delivers a validated result before 2027, it will shift KIB from a niche grid storage option into a serious competitor for mass-market battery applications.

Additionally, Reliance New Energy Solar completed its acquisition of Faradion Limited in October 2024 for approximately USD 169 Million. Faradion’s IP portfolio covers sodium and potassium-ion chemistry. Reliance’s capital base — backed by one of Asia’s largest conglomerates — gives this technology platform the scale-up funding that pure startup operations cannot access. This deal signals that large industrial groups now see non-lithium battery IP as a strategic asset worth acquiring at premium valuations.

Emerging Trends

Patent Activity and Grid-Scale Discussion Signal KIB’s Transition from Research to Commercial Pipeline

The World Intellectual Property Organization’s 2024 database recorded a rise in KIB patent filings concentrated in China and South Korea. Patent clusters in these countries have historically preceded commercial production timelines by three to five years. The current filing surge suggests that large Asian manufacturers are building IP positions ahead of KIB production scale-up — a pattern that mirrors early lithium-ion and sodium-ion development trajectories.

The Electrochemical Society’s 2024 annual meeting featured dedicated KIB technical sessions, a milestone that reflects the field’s progression from fringe research to a recognized sub-discipline. Bloomberg Energy coverage in 2024 highlighted KIB among battery alternatives gaining attention as the industry diversifies beyond lithium and sodium. Media coverage of this quality draws institutional investor attention and accelerates funding conversations.

Furthermore, peer-reviewed research in Advanced Energy Materials reported dendrite-free potassium metal anodes using artificial SEI engineering in 2024. Dendrite formation has been a core safety concern blocking potassium metal anode adoption. Solving it via SEI engineering opens a pathway to much higher energy density than carbon anodes provide — a development that, if reproducible at scale, could make KIB competitive with NMC lithium-ion for the first time.

Key Companies Insights

CATL commands a 37.9% global EV battery share and operates 646 GWh of annual production capacity — the largest globally. Its 2024 R&D spend of RMB 18.607 Billion (~USD 2.58 Billion) leads all global battery makers, and its energy storage battery systems revenue grew 34.32% year-over-year in 2024. With RMB 300 Billion in cash reserves, CATL has the capital to fund KIB pilot lines without disrupting its core lithium-ion business. Its interest in alternative chemistries is a natural hedge against long-term lithium price risk.

Group1 (Austin, Texas) is the most advanced KIB pure-play in commercial terms. It launched the world’s first commercial KIB in 18650 cylindrical format in August 2024, achieving 160-180 Wh/kg — matching LFP performance. Its technology derives from Nobel Laureate Prof. John Goodenough’s lab at UT Austin. With USD 7.5 Million in total funding through 2024, Group1 operates lean but carries the first-mover advantage of a commercial product in a field where all other players are still at prototype or research stage.

Altris AB (Uppsala, Sweden) focuses on Prussian White cathode chemistry applicable to both sodium-ion and potassium-ion cells. It raised a total of approximately USD 40 Million through 2025, backed by Clarios International, Maersk Growth, and Volvo Cars Tech Fund. Its Ferrum production facility in Sandviken produces 2,000 metric tonnes of Fennac cathode material annually — enough for up to 1 GWh of cells per year. This production infrastructure positions Altris as Europe’s most credible non-lithium cathode supplier.

HiNa Battery (China), founded in 2017, holds 249 total patents — including 101 invention patents — and is the leading commercialized sodium-ion battery maker in China. Its technical expertise in non-lithium intercalation chemistry transfers directly to KIB development. HiNa Battery’s involvement in China Datang’s 100 MWh sodium-ion grid storage project in Hubei Province — the world’s largest at launch — demonstrates that HiNa can execute at grid scale, a capability KIB entrants are working toward.

Key Companies

- CATL

- Group1

- Altris AB

- HiNa Battery Technology

- Faradion Limited (Reliance New Energy Solar)

- Project K Energy, Inc.

- Shanxi Guorun New Energy Technology

- Stanford University

- Michigan Potash and Salt Company

- Ningbo Ronbay New Energy Technology Co., Ltd.

- Zhejiang Huayou Cobalt Co., Ltd.

- A123 Systems LLC

- Farasis Energy Inc.

- Sungrow Power Supply Co., Ltd.

- Tianjin Lishen Battery Joint‑Stock Co., Ltd.

- C4V

Recent Development

- November 2025 — Group1 signed a strategic MOU with Michigan Potash and Salt Company to build a U.S. potassium-to-battery supply chain. The partnership targets data center UPS and defense applications, with the data center segment representing nearly USD 7 Trillion in projected capital spending by 2030.

- October 2024 — Reliance New Energy Solar completed its full acquisition of Faradion Limited for approximately USD 169 Million total enterprise and growth investment. The deal transferred Faradion’s sodium and potassium-ion battery IP portfolio to one of Asia’s largest industrial groups, signaling major corporate interest in KIB technology assets.

- March 2025 — CATL reported that its energy storage battery systems revenue in 2024 reached RMB 57.29 Billion, a 34.32% year-over-year rise, making it CATL’s fastest-growing segment. Net profit rose 15.01% to RMB 50.745 Billion, funded by manufacturing efficiency gains and lower raw material costs.

- August 2024 — Group1 launched the world’s first commercial potassium-ion battery in 18650 cylindrical format at the Beyond Lithium Conference at Oak Ridge National Laboratory. The cell achieves 160-180 Wh/kg, matching LFP lithium-ion performance at a potassium-based cost structure.

- October 2024 — Altris AB closed a SEK 150 Million (~USD 14.5 Million) Series B1 funding round backed by Clarios International, Maersk Growth, and Volvo Cars Tech Fund, plus an additional SEK 80.75 Million follow-on from InnoEnergy, to finalize its Swedish pilot production facility.

- January 2024 — Altris AB received SEK 77 Million in grant funding from the Swedish Energy Agency to build a pilot plant for sodium-ion cells in Uppsala under Sweden’s Industrial Leap and NextGenerationEU programs. The facility’s Prussian White cathode process is directly applicable to potassium-ion cell production.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.65 Billion |

| Forecast Revenue (2035) | USD 31.04 Billion |

| CAGR (2026-2035) | 27.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Battery Type (Rechargeable, Non-rechargeable), By Cell Format (Prismatic, Cylindrical, Pouch), By Anode Material (Carbon, Alloy, Conversion, Organic), By Capacity (Up to 10 MW, >10 MW–50 MW, >50 MW–100 MW, >100 MW), By Application (Consumer Electronics, Electric Vehicles, Energy Storage Systems, Portable Devices, Power Grids, Others), By End-use (Automotive, Defense, Medical, Power, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | CATL, Group1, Altris AB, HiNa Battery Technology, Faradion Limited (Reliance New Energy Solar), Project K Energy, Inc., Shanxi Guorun New Energy Technology, Stanford University (Battery Research Division), Michigan Potash and Salt Company, Ningbo Ronbay New Energy Technology Co., Ltd., Zhejiang Huayou Cobalt Co., Ltd., A123 Systems LLC, Farasis Energy Inc., Sungrow Power Supply Co., Ltd., Tianjin Lishen Battery Joint‑Stock Co., Ltd., C4V |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |