What is the Digital Twin in Manufacturing Market Size?

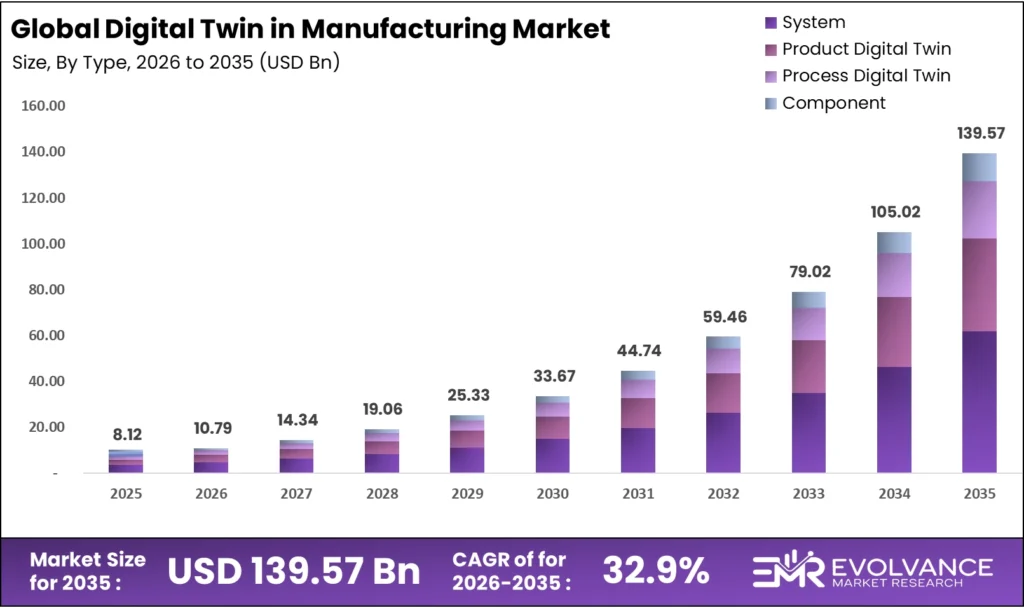

The global digital twin in manufacturing market size will be worth around USD 139.57 billion by 2035 from USD 8.12 billion in 2025, growing at a CAGR of 32.9% during the forecast period 2026 to 2035. System-level twins and on-premise deployments capture the first wave of enterprise spend as factories prioritize full-line simulation. Large manufacturers in automotive and aerospace lead procurement, while SMEs face integration cost barriers that slow adoption. Software platform consolidation among top vendors is raising switching costs and compressing margins for smaller specialists.

Market Highlights

- The Digital Twin in Manufacturing Market will grow from USD 8.12 Billion in 2025 to USD 139.57 Billion by 2035, at a CAGR of 32.9%.

- System Digital Twin leads the Type segment with 44.2% share, reflecting factory-wide simulation demand over component-level tools.

- On-Premise deployment dominates with 73.8% share, driven by data sovereignty requirements in regulated manufacturing environments.

- Large Enterprises hold 72.2% share, supported by multi-site rollouts and dedicated digital transformation budgets exceeding billions annually.

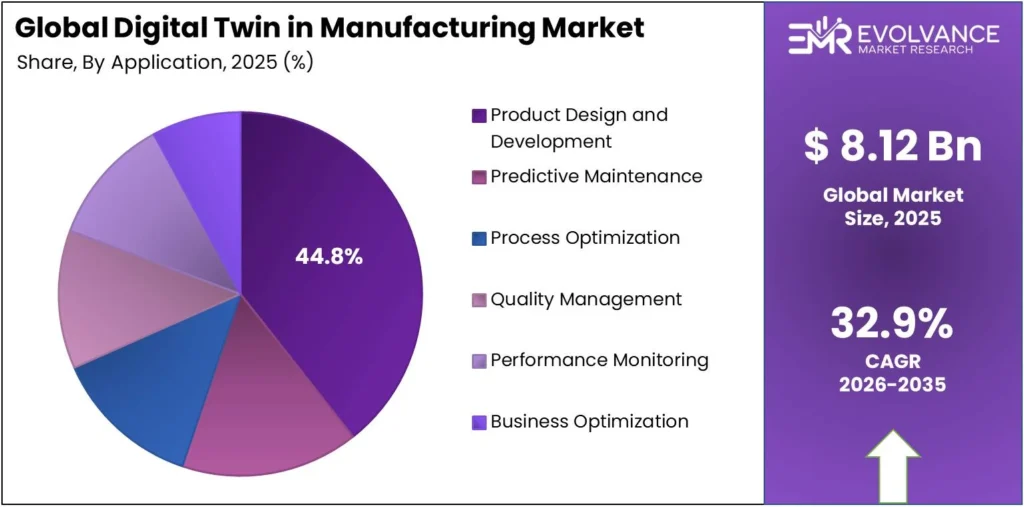

- Product Design and Development leads applications at 44.8%, as manufacturers use virtual prototyping to cut physical testing costs and speed time-to-market.

- Discrete Manufacturing dominates process types with 46.9% share, led by high-volume automotive and electronics assembly lines.

- Software is the leading component at 66.15%, with platform revenues from Siemens and Dassault Systèmes outpacing hardware spend by a wide margin.

- Automotive & Transportation leads end-user verticals with 25.6% share, driven by EV platform transitions requiring factory-level simulation before capital commitment.

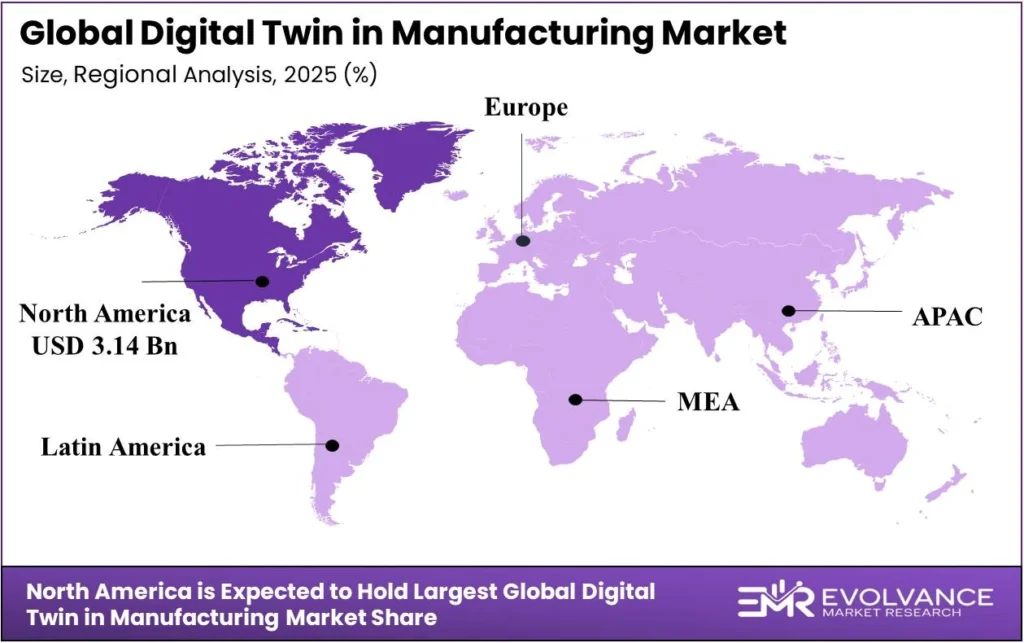

- North America leads all regions with 37.8% share, valued at USD 3.14 Billion in 2025, backed by federal Advanced and Intelligent Manufacturing funding and dense vendor concentration.

Market Overview

The Digital Twin in Manufacturing Market covers software, hardware, and services that create real-time virtual replicas of physical production assets, processes, and systems. These replicas allow factories to simulate, monitor, and improve operations without stopping live production. In 2025, the market is valued at USD 8.12 Billion, with system-level twins holding the largest share at 44.2%.

Manufacturers apply digital twins across the full production lifecycle — from product design through predictive maintenance and quality control. The technology cuts physical prototyping costs, shortens time-to-market, and enables process changes without downtime. Software accounts for 66.15% of total spend, confirming that factories treat digital twin rollouts as software investments rather than infrastructure projects.

Government programs are pushing adoption at a policy level. The SMART USA Institute launched its first funding round in June 2025, allocating $50 million for digital twin projects in semiconductor manufacturing. This public investment reduces adoption risk for private manufacturers and sets technology standards that shape vendor roadmaps for the next decade.

According to BMW Group, connecting more than 30 global production sites via virtual factory tools reduced production planning costs by up to 30%. This gain — achieved without new physical assets — shows that digital twin ROI is measurable and fast. For investors, it confirms that automotive majors are shifting from pilots to full-scale multi-site rollouts.

As reported by the Digital Catapult, the £37.6 million UK Digital Twin Centre in Belfast targets 230 new manufacturing jobs. This links public investment directly to workforce creation. Governments now treat digital twin capability as a national industrial asset — shaping procurement policy and compliance standards across the forecast period.

Digital Twin in Manufacturing Market Segmentation Analysis

Type Analysis

System Digital Twin dominates with 44.2% due to factory-wide simulation demand over point solutions.

In 2025, System Digital Twin held a dominant position in the By Type segment of the Digital Twin in Manufacturing Market, with a 44.2% share. System twins replicate entire production lines or facilities, giving operators end-to-end visibility across linked machines and logistics. At CES 2026, Siemens unveiled Digital Twin Composer on the Xcelerator Marketplace — a direct response to demand for integrated, system-level twin environments.

Product Digital Twin serves engineering teams that need virtual prototypes before committing to physical tooling. These twins simulate material behavior, stress, and performance under real operating conditions. According to Siemens AG, software revenue reached €6,286 million, up 24% in FY2024, driven by PLM and EDA tools that underpin product twin creation — confirming this as one of the fastest-scaling categories in the market.

Process Digital Twin maps production workflows, material flows, and scheduling logic in virtual form. Manufacturers test layout changes, identify bottlenecks, and run shift scenarios without halting output. According to NVIDIA, Omniverse enables simulations running 1,200x faster than conventional CAE tools, making process twin iteration viable at production cadence rather than once-per-quarter planning cycles.

Component Digital Twin focuses on individual parts, sensors, or actuators — building failure models and lifecycle data for targeted maintenance. Component twins are often the entry point for manufacturers new to digital twin technology, requiring less data integration than system-level rollouts. Their share stays smaller because standalone component monitoring delivers limited cross-line impact compared to system or process twins.

Deployment Mode Analysis

On-Premise deployment dominates with 73.8% due to data sovereignty rules in regulated industries.

In 2025, On-Premise held a dominant position in the By Deployment Mode segment of the Digital Twin in Manufacturing Market, with a 73.8% share. Aerospace, defense, and semiconductor manufacturers operating under strict data rules cannot route production IP through external cloud environments. This compliance constraint locks the majority of spend into on-premise setups, giving vendors with strong local deployment capability a structural edge.

Cloud deployment gains traction among manufacturers prioritizing rollout speed and multi-site connectivity. Volkswagen Group, which extended its AWS Digital Production Platform contract for 5 years and committed $1 billion to North American digitalization, shows how hyperscale cloud partnerships are becoming the preferred model for global OEMs managing 115 production sites worldwide.

Hybrid deployment splits sensitive process data on-premise while pushing analytics and simulation workloads to cloud infrastructure. This model lets manufacturers meet compliance requirements without giving up cloud scalability. Hybrid setups are most common in chemical and energy production, where process data is regulated but performance modeling benefits from elastic compute resources.

Enterprise Size Analysis

Large Enterprises dominate with 72.2% due to multi-site rollout scale and dedicated transformation budgets.

In 2025, Large Enterprises held a dominant position in the By Enterprise Size segment of the Digital Twin in Manufacturing Market, with a 72.2% share. Global manufacturers with hundreds of production sites can absorb the upfront integration cost of full digital twin rollouts. As per PTC Inc., ARR reached $2.25 billion, up 14% in FY2024, confirming that enterprise-grade subscription demand is large and durable.

Small and Medium Enterprises (SMEs) represent the largest untapped growth pool in the market. SMEs face higher per-unit integration costs, limited IT capability, and longer payback periods than large manufacturers. Cloud-native and modular platforms are reducing entry barriers, but SME adoption will not close the gap with large enterprises within the 2026–2035 forecast period.

Application Analysis

Product Design and Development dominates with 44.8% due to virtual prototyping cost savings at scale.

In 2025, Product Design and Development held a dominant position in the By Application segment of the Digital Twin in Manufacturing Market, with a 44.8% share. Engineers run thousands of design iterations in simulation before building a single physical prototype. BMW Group reduced collision test time from 4 weeks to 3 days using virtual factory tools — validating ROI of design-stage digital twins at production scale.

Predictive Maintenance uses live sensor data from equipment to forecast failures before they happen. Manufacturers in oil and gas, energy, and chemicals deploy these twins to avoid unplanned downtime, which costs millions per hour in continuous-process environments. The TwinThread Advisor generative AI assistant, previewed in October 2025, integrates directly into industrial digital twin platforms to automate anomaly detection and maintenance scheduling.

Process Optimization twins model production scheduling, material routing, and machine sequencing to maximize throughput. Manufacturers test shift changes, supplier lead time shifts, and demand swings without disrupting live output. Process optimization is the second-largest application by adoption rate among discrete manufacturers in 2025.

Quality Management twins monitor dimensional accuracy, surface finish, and defect rates across batches in real time. Linking sensor data from inspection systems to a virtual quality model lets manufacturers trace defects to root causes within minutes. This application is most advanced in semiconductor and precision electronics production.

Performance Monitoring gives operators continuous visibility into equipment use, energy draw, and output rates across production lines. These twins function as a persistent operational dashboard rather than a planning tool. Integration with ERP and MES systems is the main technical requirement that slows broader rollout in 2025.

Business Optimization extends digital twin logic beyond the factory floor to supply chain, demand planning, and capital allocation. Industrial circular economy digital platforms are emerging within this application as manufacturers connect twin data to material recovery workflows, remanufacturing scheduling, and end-of-life routing decisions. This application is early-stage but expanding as manufacturers recognize that factory simulation data can feed enterprise planning models. Deep data linkage between operational and commercial systems remains the primary barrier to near-term adoption.

Manufacturing Process Type Analysis

Discrete Manufacturing dominates with 46.9% due to high-volume, configurable production complexity.

In 2025, Discrete Manufacturing held a dominant position in the By Manufacturing Process Type segment of the Digital Twin in Manufacturing Market, with a 46.9% share. Automotive, aerospace, and electronics producers — who build countable units in complex assembly sequences — get the most value from system and process twins. BMW Group produces 2.5 million vehicles per year with 99% customized before production — a variant complexity only digital twin simulation can manage cost-effectively.

Process Manufacturing covers continuous production of chemicals, pharmaceuticals, food, and metals where output is measured in volume or weight. Digital twins here focus on reactor modeling, yield improvement, and safety monitoring. Vendor adoption in this segment is led by Honeywell and ABB, whose process control software already embeds digital twin functions at the platform level.

Hybrid Manufacturing combines discrete assembly with continuous processing — common in semiconductor fabrication and specialty chemicals. Digital twin tools for hybrid environments must merge simulation models from both process types, creating higher integration complexity and longer rollout timelines. This technical barrier keeps hybrid manufacturing as the smallest of the three segments through 2035.

Component Analysis

Software dominates with 66.15% due to platform-led vendor strategies and recurring revenue models.

In 2025, Software held a dominant position in the By Component segment of the Digital Twin in Manufacturing Market, with a 66.15% share. Platform vendors like Siemens, Dassault Systèmes, and PTC earn the majority of revenue through licenses and subscriptions. Based on data from Dassault Systèmes, the 3DEXPERIENCE platform grew 22% in Q4 2024, confirming that recurring software revenue is the primary value capture mechanism in this industry.

Services include setup, linking, training, and managed services that help manufacturers deploy and run digital twin environments. As rollout complexity grows with system-level twins, professional services revenue scales alongside it. Siemens AG invests €180 million annually in training and €237 million in workforce education focused on digital twins, IoT, and AI — directly building the services ecosystem that supports its software platform.

Hardware covers sensors, edge computing nodes, and industrial PCs that feed real-time data into digital twin software. Hardware’s share is smallest because most manufacturers already have installed sensor setups that can connect to twin platforms. Incremental hardware spending is modest compared to software licensing costs at comparable rollout scale.

End-User Industry Analysis

Automotive & Transportation dominates with 25.6% due to EV transitions requiring factory-scale simulation.

In 2025, Automotive & Transportation which includes Digital Twin in Automotive Manufacturing, held a dominant position in the By End-User Industry segment of the Digital Twin in Manufacturing Market, with a 25.6% share. EV platform transitions force automakers to redesign production lines at a pace that physical trial-and-error cannot support. BMW Group is investing €650 million in its Munich plant EV transition, with virtual factory twins central to validating line changes before capital is committed.

Aerospace & Defense adopts digital twins for structural simulation, lifecycle management, and maintenance of complex, long-lived assets. Regulatory certification requirements make physical testing mandatory, but twins reduce the number of physical test cycles needed. Defense contractors use twins for platform sustainment across decades-long asset lives, where simulation data reduces costly physical inspections.

Electronics & Semiconductors use digital twins to model chip fabrication, PCB assembly, and test processes where nanometer-scale precision makes physical trial-and-error unacceptably costly. The SMART USA Institute’s $50 million semiconductor digital twin fund in June 2025 directly targets this segment’s technical complexity and national supply chain priority.

Oil & Gas deploys twins for upstream asset monitoring, pipeline integrity, and refinery process improvement. The high cost of unplanned shutdowns — often millions per day — makes predictive maintenance twins highly valuable in this vertical. Offshore platforms are among the most advanced deployments, where physical inspection access is dangerous and expensive.

Energy & Utilities uses digital twins to manage grid assets, power plant operations, and renewable energy sites. Findings from GE Vernova, with $34.9 billion in FY2024 revenue and Electrification segment up 18%, show that grid operators are actively investing in digital tools to manage complex, distributed energy systems at scale.

Healthcare & Life Sciences applies digital twin tools to pharmaceutical production, medical device manufacturing, and sterile fill-finish operations. FDA and EMA validation requirements give twins a compliance and traceability role beyond pure efficiency — making them a regulatory asset. Adoption is rising as drug manufacturers face more complex multi-product facility demands.

Consumer Goods manufacturers use digital twins for packaging line improvement, demand-driven scheduling, and sustainability reporting on energy and material use. Adoption lags other verticals because product complexity and regulatory pressure are both lighter. However, falling platform costs are strengthening the cost efficiency case for mid-size consumer goods producers through 2030.

Market Segments Covered in the Report

By Type

- System Digital Twin

- Product Digital Twin

- Process Digital Twin

- Component Digital Twin

By Deployment Mode

- On-Premise

- Cloud

- Hybrid

By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

By Application

- Product Design and Development

- Predictive Maintenance

- Process Optimization

- Quality Management

- Performance Monitoring

- Business Optimization

By Manufacturing Process Type

- Discrete Manufacturing

- Process Manufacturing

- Hybrid Manufacturing

By Component

- Software

- Services

- Hardware

By End-User Industry

- Automotive & Transportation

- Aerospace & Defense

- Electronics & Semiconductors

- Oil & Gas

- Energy & Utilities

- Healthcare & Life Sciences

- Consumer Goods

Digital Twin in Manufacturing Market Regional Insights

North America Dominates the Digital Twin in Manufacturing Market with a Market Share of 37.8%, Valued at USD 3.14 Billion

North America holds 37.8% of the global Digital Twin in Manufacturing Market, valued at USD 3.14 Billion in 2025. The United States concentrates the world’s leading digital twin platform vendors — Siemens, PTC, Microsoft, and GE Vernova — alongside federal programs like the SMART USA Institute’s $50 million semiconductor fund. This vendor density and public investment create a self-reinforcing adoption environment that no other region matches in 2025.

Europe Digital Twin in Manufacturing Market Trends

Europe’s digital twin manufacturing sector is anchored by Germany’s €150 million Manufacturing-X program and the UK’s £37.6 million Digital Twin Centre in Belfast. Germany installed 28,400 industrial robots in 2024, generating sensor data that feeds directly into twin platforms. These government programs reduce adoption risk for European manufacturers and signal policy-level commitment to digital factory infrastructure through the late 2020s.

Asia Pacific Digital Twin in Manufacturing Market Trends

Asia Pacific is building digital twin adoption through national manufacturing modernization programs. Japan’s Ministry of Economy, Trade and Industry released its Smart Manufacturing Development Guideline in June 2024, with smart factory adoption reaching 35.2% that year. China’s domestic cloud providers — Alibaba Cloud, Huawei, and Tencent — are building manufacturing-specific twin platforms that compete on price and local data residency against Western vendors.

Latin America Digital Twin in Manufacturing Market Trends

Latin America’s digital twin adoption centers on Brazil and Mexico, where automotive assembly and agribusiness processing create demand for discrete and process manufacturing twins. OEMs with Mexican production sites are extending global digital twin platforms to North American assembly lines as part of broader nearshoring investments. Regional adoption lags due to limited local vendor ecosystems and slower capital deployment cycles through 2028.

Middle East & Africa Digital Twin in Manufacturing Market Trends

Middle East and Africa digital twin investment concentrates in energy, oil and gas, and large-scale infrastructure across the GCC. Saudi Arabia’s Vision 2030 industrial programs include smart factory targets that create demand for process twins in petrochemical and metals production. South Africa’s manufacturing base is adopting digital twin tools in mining and automotive sectors, though adoption scale stays smaller than GCC rollouts through 2027.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The European Union’s Machinery Regulation (EU) 2023/1230, taking full effect in January 2027, requires digital documentation of machine safety behavior — a requirement that digital twin simulation fulfills directly. Manufacturers selling into EU markets must begin compliance planning now, making digital twin adoption a regulatory necessity rather than an optional efficiency upgrade for this segment.

The U.S. CHIPS and Science Act, enacted in 2022 and actively funded through 2025 and beyond, includes manufacturing technology provisions that back digital twin use in semiconductor fabrication. The SMART USA Institute, operating under this framework, allocated $50 million in June 2025 for digital twin innovation in chip manufacturing — translating federal law directly into funded technology programs.

The U.S. Cybersecurity and Infrastructure Security Agency (CISA) issued its 2024 Industrial Control Systems Advisory, flagging cybersecurity risks in connected manufacturing environments including digital twin-linked factories. Compliance with CISA guidance shapes procurement and architecture decisions for U.S. defense and critical infrastructure manufacturers adopting digital twin platforms at scale.

Japan’s Ministry of Economy, Trade and Industry released the Smart Manufacturing Development Guideline in June 2024, setting interoperability and data standards for smart factory rollouts. This guideline formalizes data exchange expectations between supply chain partners — creating a de facto compliance standard for manufacturers supplying Japanese OEMs and Tier 1 industrial buyers.

Digital Twin in Manufacturing Market Dynamics

Drivers

Platform Consolidation and Major Acquisitions Concentrate Digital Twin Capability Among Leading Vendors

Siemens AG announced a €10 billion acquisition of Altair Engineering, expanding its industrial simulation and digital twin portfolio well beyond its existing Xcelerator platform. This deal signals that top vendors are building capability through acquisition rather than organic development alone. Smaller specialists face a shrinking competitive window as the technical baseline for the entire industry rises with each major deal.

Microsoft integrated industrial AI into Azure Digital Twins to improve factory simulation and predictive modeling. This move positions Azure not just as cloud infrastructure but as an active digital twin application platform — competing directly with Siemens and PTC for application-layer revenue. For manufacturers, more capable off-the-shelf tools are available, but deeper vendor lock-in follows as AI features embed in cloud-native twin environments.

As reported by the Germany Trade and Invest agency, Germany’s robotics market reached €16.0 billion in turnover in 2024, with 28,400 industrial robot installations. This scale of automated equipment generates the real-time sensor data that feeds digital twin platforms — making Germany’s manufacturing base one of the most data-rich twin adoption environments in the world.

Restraints

Cybersecurity Vulnerabilities and Legacy System Gaps Slow Digital Twin Rollouts Among Risk-Averse Manufacturers

The 2024 CISA Industrial Control Systems Advisory flagged specific attack vectors in connected manufacturing environments where digital twin platforms share real-time data with production systems. This guidance forces security audits, architecture reviews, and potential redesigns for factories already mid-rollout — adding cost and time to programs that procurement teams had already approved and budgeted.

Interoperability between legacy manufacturing systems and modern digital twin platforms remains a technical barrier that Gartner analysts flagged in their manufacturing technology research. Most industrial facilities run equipment from multiple generations and vendors — none designed to share data in standard formats. Building the data bridges needed for accurate twin modeling can cost more than the twin platform itself for older facilities.

Even the largest manufacturers face capital constraints at rollout scale. Volkswagen Group, with €324.7 billion in 2024 revenue, committed $1 billion to North American digitalization — yet that figure covers 115 global production sites. For mid-size manufacturers without comparable balance sheets, the per-site investment required for full digital twin rollout remains a structural brake on adoption rates through the near term.

Growth Factors

EV Investment, Cloud Platform Partnerships, and Government Programs Open New Revenue Pools for Digital Twin Vendors

BMW Group is investing €650 million in its Munich plant EV transition, with virtual factory planning central to validating that capital deployment. When a manufacturer redesigns an entire production line for a new vehicle platform, digital twin simulation is the most cost-effective way to test the new layout before physical construction begins. BMW’s investment directly funds new digital twin tool adoption at one of Europe’s highest-output facilities.

Amazon Web Services expanded its industrial digital twin tools through enhanced AWS IoT TwinMaker integrations, giving manufacturers pre-built connectors to common industrial data sources. This cuts rollout time and reduces the professional services cost that represents a significant share of total digital twin budgets. Rockwell Automation also partnered with Microsoft to integrate generative AI with factory digital twins — combining Rockwell’s installed automation base with Microsoft’s AI tools to open new cross-sell revenue streams.

The European Commission’s 2024 Industry 5.0 programs promote human-centric digital twin adoption across advanced manufacturing sectors in member states. These programs provide co-funding for manufacturers adopting twin technologies in production, reducing the risk-adjusted cost of adoption. For vendors with EU market exposure, Industry 5.0 funding creates a pull-based demand channel that operates independently of enterprise IT budget cycles.

Emerging Trends

Generative AI Embedded in Digital Twin Platforms Shifts Buyer Expectations Toward Autonomous Factory Simulation

At Hannover Messe 2024, multiple automation vendors announced generative AI integrations into their digital twin platforms — marking a shift from static simulation to AI-driven scenario creation. Manufacturers can now ask a digital twin to propose process changes, not just model them. Buyers evaluating platforms in 2025 and beyond will treat AI-native features as a baseline requirement rather than a premium add-on.

Cloud-native digital twin rollouts on Microsoft Azure and Amazon Web Services are replacing on-premise-first strategies for new manufacturing sites and greenfield plants. Data from NVIDIA shows 252+ enterprise Omniverse deployments — a platform built for real-time 3D simulation of factory environments. These deployments confirm that cloud-based, GPU-accelerated twin environments are operationally proven at enterprise scale as of 2025.

NVIDIA announced its Mega Blueprint for industrial robot fleet digital twins at CES 2025, enabling manufacturers to simulate entire robot fleets in real time before physical setup. Automotive manufacturers building EV-specific assembly lines are the primary early adopters, using these tools to validate robot placement and throughput before a single bolt is turned. Early movers gain line commissioning speed that translates directly to production launch timing advantage over competitors.

Digital Twin in Manufacturing Market Key Companies Insights

Siemens AG holds a structural edge in this market through the Xcelerator software platform, a €9 billion Digital Industries order backlog, and a planned €10 billion Altair Engineering acquisition that adds deep simulation capability to its existing PLM and twin portfolio. Its software revenue of €6,286 million in FY2024 — up 24% — shows the market rewarding its platform-led strategy. Annual €237 million workforce education investment builds the customer skill base its tools require at scale.

Dassault Systèmes sets itself apart through the 3DEXPERIENCE platform, which grew 22% in Q4 2024 and serves 370,000 customers across 150+ countries. Its strength in life sciences and aerospace — industries with complex regulatory validation needs — creates a defensible position where competitors cannot simply compete on price alone. FY2024 operating cash flow of €1.66 billion gives Dassault financial flexibility to extend its platform into AI-native simulation without needing partner capital.

PTC Inc. built its competitive position on a recurring revenue model: 93% of its $2.30 billion FY2024 revenue was recurring, with ARR at $2.25 billion — up 14%. Its acquisition of pure-systems for $93.5 million expanded PLM and digital thread capability, making PTC more attractive for manufacturers managing complex multi-variant product families. Its base of 30,000+ manufacturing customers creates cross-sell opportunities that pure-play digital twin startups cannot match.

GE Vernova operates at the intersection of physical industrial assets and digital monitoring, with $34.9 billion in FY2024 revenue and $44.1 billion in orders confirming strong forward demand. Its Electrification segment — up 18% in 2024 — places GE Vernova directly in the energy transition market where grid digital twins are becoming an operational requirement. Free cash flow of $1.7 billion funds continued software development without relying on equity markets for capital.

Key players

- Siemens AG

- Dassault Systèmes

- Microsoft Corporation

- GE Vernova / GE Digital

- PTC Inc.

- ANSYS Inc.

- ABB Ltd.

- Amazon Web Services (AWS)

- IBM Corporation

- SAP SE

- Hexagon AB

- Rockwell Automation

- Autodesk Inc.

- AVEVA Group (Schneider Electric)

- Bentley Systems

- NVIDIA

- Honeywell

- Bosch Software Innovations

- Oracle Corporation

- Capgemini

- Accenture

- FANUC

- Huawei

- Alibaba Cloud

- Tencent

Recent Development

- January 2026 – TwinThread released Perfect Centerline, an AI-powered manufacturing optimization solution using real-time data analytics and digital-twin-enabled insights to standardize operations and improve production consistency across manufacturing lines.

- January 2025 – Taiwanese startup MetAI raised a $4 million seed round led by NVIDIA, with participation from multiple strategic and venture investors, to build AI-powered digital twins for industrial applications.

- May 2024 – EthonAI secured a $16.5 million funding round led by Index Ventures, validating investor appetite for specialized AI tools built on top of digital twin data layers in manufacturing environments.

- April 2025 – PerfCam research on digital twinning for production lines using 3D and vision models was published, advancing the case for computer-vision-driven digital twins in factory quality monitoring and inspection workflows.

- 2024 – ANSYS agreed to an acquisition by Synopsys for $35 billion, the largest deal in simulation software history, combining ANSYS’s physics simulation tools with Synopsys’s semiconductor and systems design platform.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 8.12 Billion |

| Forecast Revenue (2035) | USD 139.57 Billion |

| CAGR (2026-2035) | 32.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (System, Product Digital Twin, Process Digital Twin, Component), By Deployment Mode (On-Premise, Cloud, Hybrid), By Enterprise Size (Large Enterprises, SMEs), By Application (Product Design and Development, Predictive Maintenance, Process Optimization, Quality Management, Performance Monitoring, Business Optimization), By Manufacturing Process Type (Discrete Manufacturing, Process Manufacturing, Hybrid Manufacturing), By Component (Software, Services, Hardware), By End-User Industry (Automotive & Transportation, Aerospace & Defense, Electronics & Semiconductors, Oil & Gas, Energy & Utilities, Healthcare & Life Sciences, Consumer Goods) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Siemens AG, Dassault Systèmes, Microsoft Corporation, GE Vernova / GE Digital, PTC Inc., ANSYS Inc., ABB Ltd., Amazon Web Services (AWS), IBM Corporation, SAP SE, Hexagon AB, Rockwell Automation, Autodesk Inc., AVEVA Group (Schneider Electric), Bentley Systems, NVIDIA, Honeywell, Bosch Software Innovations, Oracle Corporation, Capgemini, Accenture, FANUC, Huawei, Alibaba Cloud, Tencent |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |