What is the Chlor-Alkali Market Size?

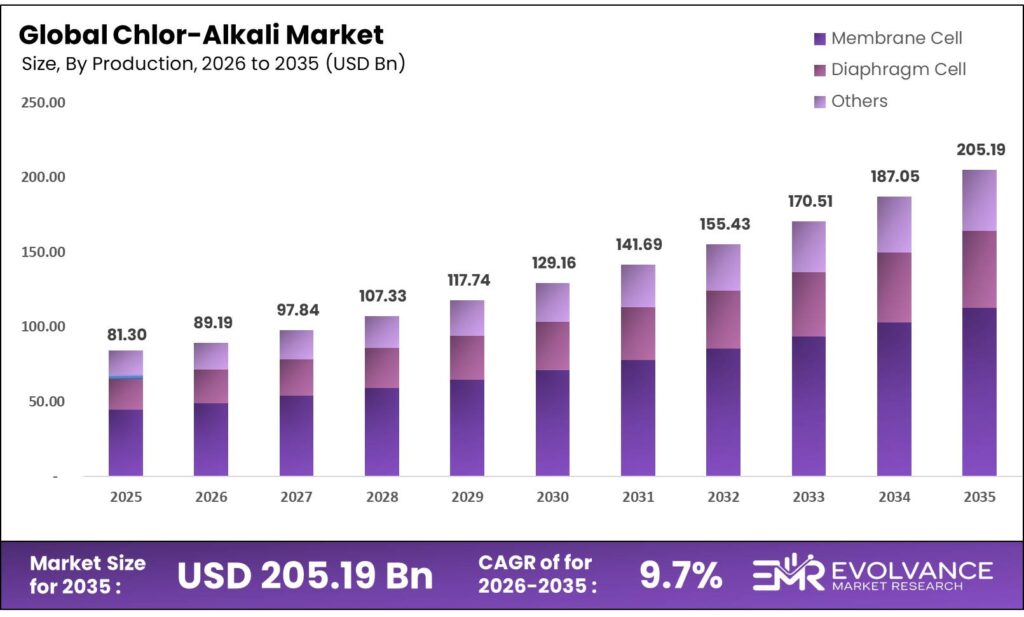

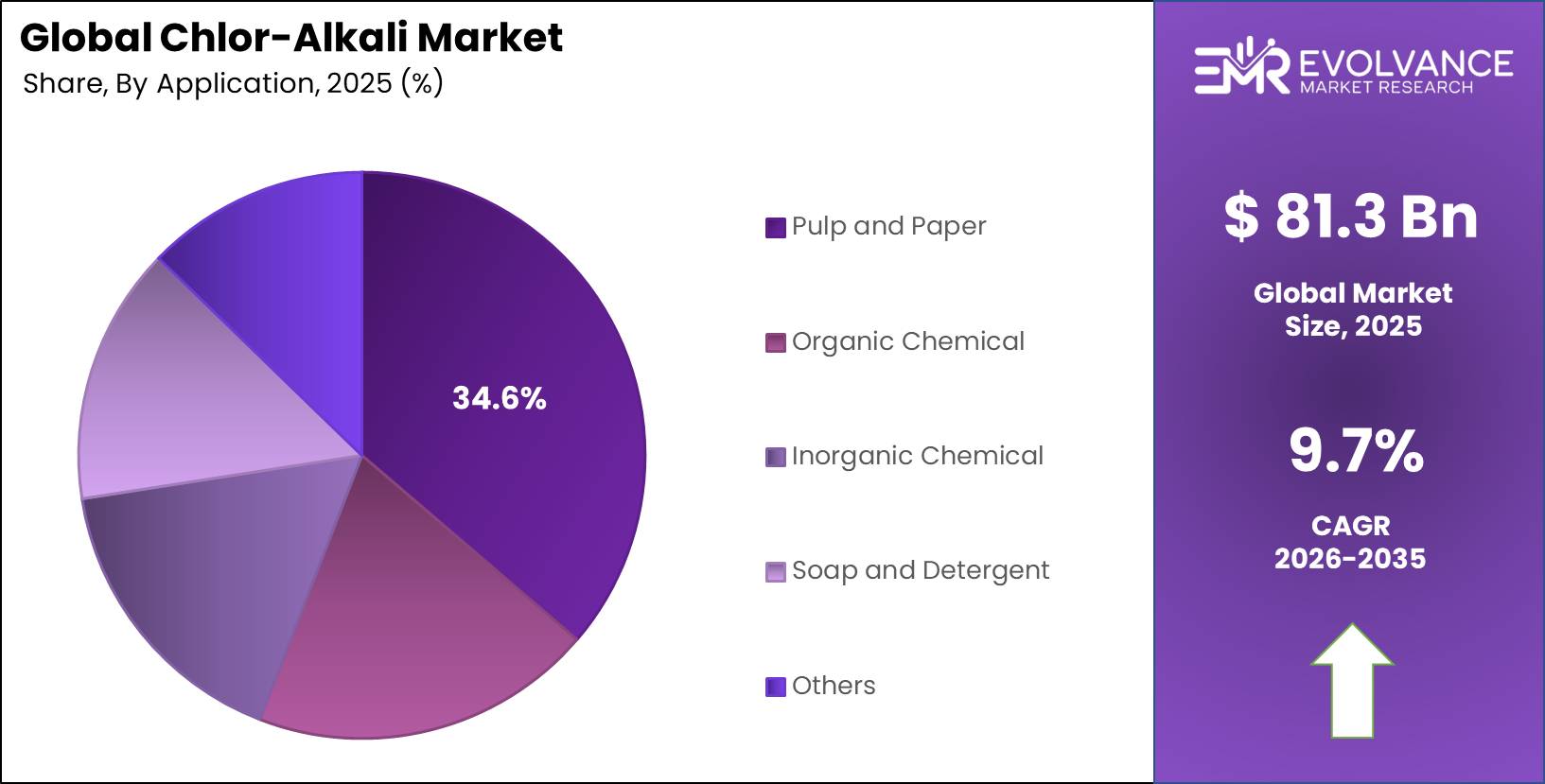

The Global Chlor-Alkali Market size is expected to be worth around USD 205.19 Billion by 2035 from USD 81.30 Billion in 2025, growing at a CAGR of 9.7% during the forecast period 2026 to 2035. This growth stems from rising demand for caustic soda in alumina refining and pulp production. Chlorine consumption in water treatment and PVC making also drives market gains across global industries.

Market Highlights

- The Global Chlor-Alkali Market valued at USD 81.30 Billion in 2025, projected to reach USD 205.19 Billion by 2035, at a CAGR of 9.7% during forecast period 2026-2035

- Asia-Pacific region dominates with 41.3% market share, valued at USD 33.3 Billion

- Caustic Soda segment dominates product category with 47.3% market share

- Membrane Cell technology leads production process segment with 61.2% share

- Pulp and Paper application holds largest share at 34.6% of total market

- Chemical Processing and Manufacturing end user segment accounts for 31.4% market share

Market Overview

Chlor-alkali products form the backbone of modern chemical making and water treatment systems worldwide. These basic chemicals include caustic soda, chlorine, and soda ash made through electrolysis of salt brine. Industries rely on these outputs for pulp making, PVC production, water cleaning, and pharma making across global markets.

The sector serves vital roles in building materials, textiles, and aluminum refining through supply of key raw inputs. Plants use three main cell types for production: membrane, diaphragm, and older mercury systems. Modern units favor membrane cells for better energy use and lower emissions in line with green rules.

About 70% of US chlorine output serves organic chemical making, with nearly 40% going to vinyl chloride for PVC production. Caustic soda splits across 30% organic chemical use and 20% inorganic chemical applications for neutralizing and scrubbing operations. The pulp and paper sector takes another 20% of sodium hydroxide for wood processing and bleaching steps in mills.

Plants cluster near end users since chlorine proves hard to store and ship at low cost. About 72% of US chlorine production occurs in Gulf Coast facilities close to chemical makers and paper mills. This proximity cuts transport costs and ensures reliable supply to high-volume industrial customers in regional manufacturing corridors.

Plants face rising power bills that affect profit margins since electrolysis needs heavy energy input for cell reactions. Makers invest in process upgrades to boost efficiency and meet tighter rules on chlorine handling and plant emissions. Digital tools now help plants track cell performance and predict upkeep needs before system failures occur.

Product Insights

Caustic Soda dominates with 47.3% due to broad industrial applications and essential role in chemical processing.

In 2025, Caustic Soda held a dominant market position in the By Product segment of Chlor-Alkali Market, with a 47.3% share. This leadership stems from wide use in alumina refining, pulp making, and organic chemical production across global industries. Plants rely on caustic soda for neutralizing acids, cleaning systems, and making soaps and detergents in daily operations.

Chlorine serves as vital input for PVC making, water treatment, and organic chemical synthesis in industrial sectors. Municipal water plants use chlorine for disinfection and sanitation to protect public health and safety standards. The pharma sector also consumes chlorine for active ingredient production and facility cleaning in controlled environments.

Soda Ash finds primary use in glass making, detergent production, and water softening across consumer and industrial markets. This product supports flat glass output for building and auto sectors while enabling soap and cleaning product making. Soda ash also helps adjust pH levels in chemical processes and wastewater treatment plant operations nationwide.

Others category includes specialty chlor-alkali outputs and co-products from electrolysis cells used in niche applications. These materials support specific industrial needs in metal processing, textile making, and food production with customized specifications. Minor products also serve regional markets with unique regulatory or technical requirements for chemical composition and purity.

Production Process Insights

Membrane Cell dominates with 61.2% due to superior energy efficiency and lower environmental impact.

In 2025, Membrane Cell held a dominant market position in the By Production Process segment of Chlor-Alkali Market, with a 61.2% share. This technology uses ion-exchange membranes to produce high-purity caustic soda with less power consumption than older methods. Modern plants favor membrane cells for meeting strict emissions rules and cutting operating costs through improved energy efficiency.

Diaphragm Cell technology remains in use at legacy plants where capital costs limit upgrades to newer membrane systems. This method produces lower-purity caustic soda that requires additional processing steps for certain end use applications. Diaphragm cells still serve regional markets with established infrastructure and stable customer bases for standard-grade chemical outputs.

Others category includes legacy mercury cell systems being phased out globally due to environmental and health concerns. Some older plants continue operations under strict regulatory oversight while planning transitions to cleaner technologies. This segment shrinks steadily as nations ban mercury processes and makers invest in modern membrane cell capacity.

Application Insights

Pulp and Paper dominates with 34.6% due to essential role in wood chip processing and bleaching operations.

In 2025, Pulp and Paper held a dominant market position in the By Application segment of Chlor-Alkali Market, with a 34.6% share. Mills use caustic soda for pulping wood chips and chlorine for bleaching paper products to meet quality standards. This sector maintains steady chlor-alkali demand through integrated supply contracts with nearby chemical plants for reliable product delivery.

Organic Chemical production consumes large volumes of chlorine for vinyl chloride, solvents, and petrochemical intermediate making. These outputs feed into PVC plants, refrigerant units, and specialty chemical facilities across industrial value chains. Organic chemical makers often locate near chlor-alkali plants to ensure steady chlorine supply for continuous process operations.

Inorganic Chemical making uses caustic soda for neutralizing acids, scrubbing emissions, and producing alumina and other base materials. This application supports metal refining, pigment making, and industrial gas production with consistent alkali demand patterns. Plants rely on predictable caustic soda quality for maintaining product specs and process control in chemical reactions.

Soap and Detergent production uses caustic soda for saponification and cleaning product formulation in consumer goods making. This sector values high-purity sodium hydroxide for meeting safety rules and product performance standards in retail markets. Detergent plants maintain steady alkali purchases through long-term supply deals with regional chlor-alkali producers for cost control.

End User Insights

Chemical Processing and Manufacturing dominates with 31.4% due to extensive use across organic and inorganic chemical production.

In 2025, Chemical Processing and Manufacturing held a dominant market position in the By End User segment of Chlor-Alkali Market, with a 31.4% share. This sector consumes chlorine for vinyl chloride, solvents, and intermediates while using caustic soda for neutralizing and chemical synthesis. Integrated chemical complexes often include chlor-alkali units to ensure reliable supply of these essential raw materials for downstream operations.

Textiles industry uses caustic soda for mercerizing cotton, scouring fabrics, and dyeing operations in garment and home textile making. Chlorine serves in bleaching and disinfection steps to meet quality and cleanliness standards for finished goods. Textile mills maintain steady alkali demand through seasonal production cycles and export-oriented output targets in global markets.

Water and Wastewater Treatment facilities rely on chlorine for disinfecting drinking water and treating sewage to protect public health. Caustic soda helps adjust pH levels and neutralize acids in treatment processes at municipal and industrial plants. This sector shows stable demand growth tied to population expansion and stricter water quality rules in developing regions.

Aluminum and Metal Processing uses caustic soda for alumina refining from bauxite ore in primary metal production operations. This application consumes large alkali volumes at smelters and refineries located near chlor-alkali plants for cost efficiency. Metal processors also use chlorine for titanium production and surface treatment in specialty alloy making operations.

Glass Manufacturing uses soda ash as flux in melting silica sand and limestone to make flat glass and containers. Caustic soda serves in glass cleaning and etching processes for specialty products and quality control steps. Glass plants maintain steady purchases tied to building construction cycles and auto industry demand for windshields and windows.

Market Segments Covered in the Report

By Product

- Caustic Soda

- Chlorine

- Soda Ash

- Others

By Production Process

- Membrane Cell

- Diaphragm Cell

- Others

By Application

- Pulp and Paper

- Organic Chemical

- Inorganic Chemical

- Soap and Detergent

- Others

By End User

- Chemical Processing and Manufacturing

- Textiles

- Water and Wastewater Treatment

- Aluminum and Metal Processing

- Glass Manufacturing

- Pharmaceuticals

- Food Processing

Chlor-Alkali Market Regional Insights

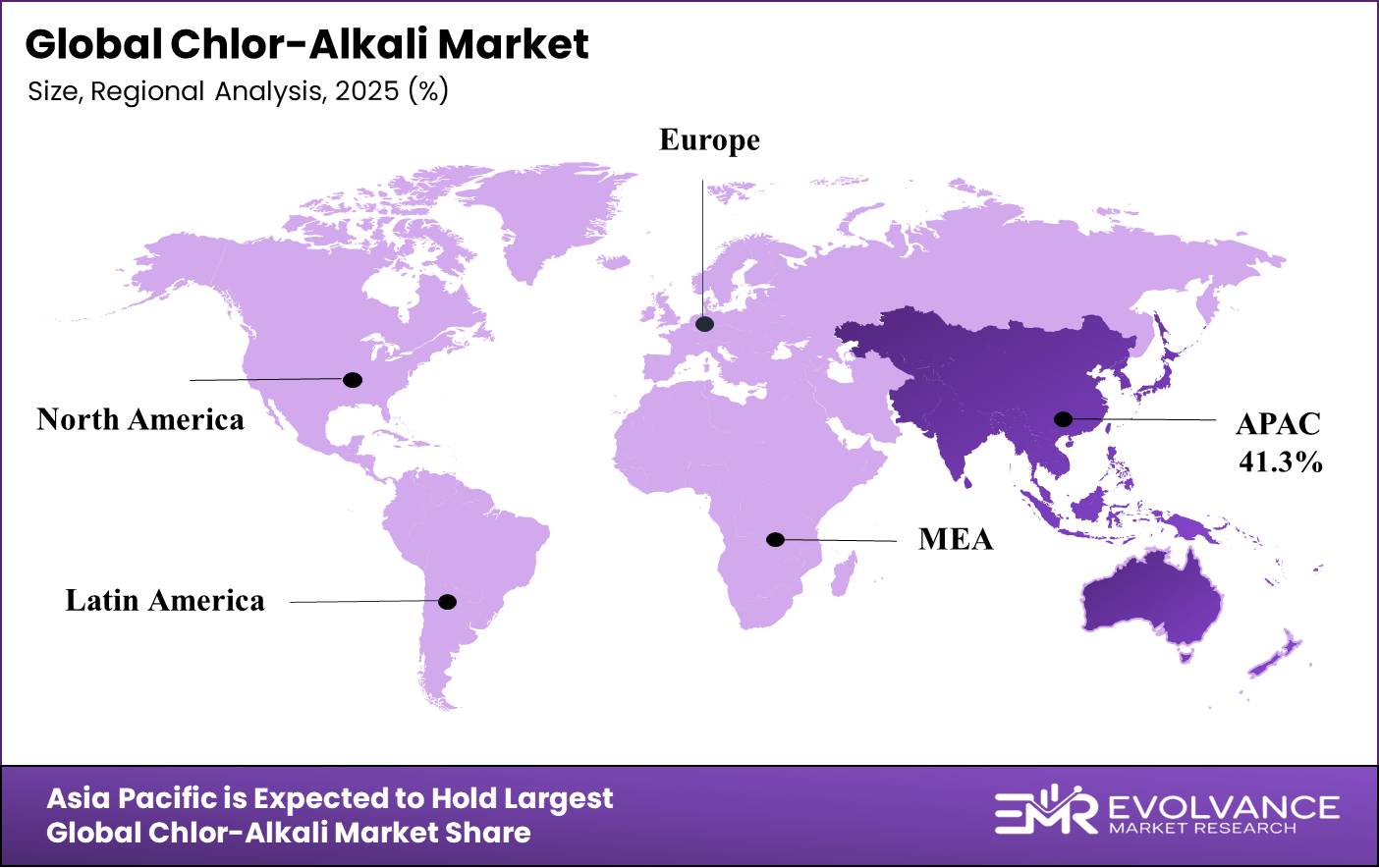

Asia-Pacific Dominates the Chlor-Alkali Market with a Market Share of 41.3%, Valued at USD 33.3 Billion

Asia-Pacific leads global chlor-alkali output with 41.3% market share worth USD 33.3 Billion through massive chemical complexes and growing industrial demand. China, India, Japan, and South Korea host large production sites serving regional pulp mills, chemical plants, and water treatment facilities. Fast urban growth and building booms drive strong PVC and caustic soda consumption across emerging Asian economies and mature markets.

North America Market Trends

North America maintains significant chlor-alkali capacity concentrated along the Gulf Coast near chemical clusters and pulp mills. The US and Canada operate advanced membrane cell plants with integrated downstream units for vinyl chloride and other derivatives. Makers focus on energy efficiency gains and capacity debottlenecking to serve stable regional demand from established industrial customers.

Europe Market Trends

Europe pursues strict environmental rules driving conversion from legacy mercury and diaphragm cells to clean membrane technology. Germany, France, and the UK host major chemical hubs consuming chlor-alkali outputs for specialty chemicals and export products. Regional makers invest in carbon footprint cuts and renewable power sourcing to meet climate targets and green chemistry standards.

Latin America Market Trends

Latin America shows steady chlor-alkali demand growth tied to infrastructure projects and expanding industrial sectors in Brazil and Mexico. Regional plants serve pulp exports, aluminum smelters, and domestic chemical making with reliable product supply and competitive pricing. Makers explore capacity additions to capture growing consumption from water treatment upgrades and building material production nationwide.

Middle East & Africa Market Trends

Middle East and Africa develop new chlor-alkali capacity leveraging low-cost power and salt resources for petrochemical integration. GCC nations invest in large-scale plants linked to PVC chains and export-oriented chemical complexes in industrial zones. South Africa maintains regional output serving mining, water treatment, and chemical sectors with stable demand from established industries.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

Global chlor-alkali rules tighten emissions limits and phase out mercury cell technology to protect worker health and the environment. The United Nations Minamata Convention on Mercury drives plant closures and conversions to membrane cells across signatory nations by 2025. This treaty affects legacy facilities worldwide and requires capital investment in cleaner production systems for regulatory compliance.

European Union regulations set strict standards for chlorine handling, storage, and transport under REACH and Seveso directives issued in 2024. These rules mandate safety upgrades, emergency response plans, and emissions monitoring at chemical plants to prevent accidents. US EPA also enforces Clean Air Act requirements on chlorine plants with periodic rule updates affecting operating permits nationwide.

Water quality rules in developing nations drive chlorine demand for municipal disinfection systems meeting WHO drinking water standards. Governments invest in treatment infrastructure and mandate chlorine use for public health protection in urban supply networks. These regulatory drivers support steady chlor-alkali consumption growth tied to sanitation improvements and population expansion in emerging economies.

Drivers

Rising Demand for Caustic Soda from Pulp & Paper and Alumina Refining Industries

Pulp and paper mills expand capacity to meet global packaging and tissue demand driving caustic soda purchases for wood processing. Alumina refineries consume large alkali volumes for bauxite ore treatment in primary aluminum making across growing industrial economies. This dual demand from two major sectors creates stable, long-term growth for chlor-alkali plants serving integrated supply chains.

Paper producers upgrade mills with advanced pulping systems requiring consistent caustic soda quality for efficient fiber processing operations. Aluminum smelters build new refineries in power-rich regions consuming steady alkali flows for metal extraction from imported ore. These capital-intensive projects support multi-year supply contracts providing revenue visibility for chlor-alkali makers planning capacity additions.

Export-oriented pulp production in Latin America and Southeast Asia drives regional caustic soda demand from new greenfield mills. Metal producers in the Middle East and Asia invest in integrated alumina-aluminum complexes with dedicated alkali supply agreements. This geographic expansion of end-use sectors creates new market opportunities for chlor-alkali plants in emerging industrial regions.

Restraints

High Energy Intensity and Volatile Power Costs Impacting Production Economics

Chlor-alkali plants consume heavy electricity for electrolysis cells making them vulnerable to power price swings affecting profit margins. Energy typically represents 30 to 40% of total production costs creating exposure to utility rate changes and fuel price volatility. Plants in regions with high power costs face competitive disadvantages compared to facilities accessing cheap hydroelectric or natural gas generation.

Fluctuating electricity prices complicate long-term supply contracts and pricing negotiations with customers seeking stable product costs. Makers invest in energy management systems and power purchase agreements to hedge against rate increases and grid instability. Some plants add onsite generation or demand response capabilities to cut costs and improve operational flexibility during peak pricing periods.

Carbon pricing and renewable energy mandates raise power costs in certain markets affecting chlor-alkali plant economics and competitiveness. Operators evaluate relocations or closures in high-cost regions while expanding capacity in areas with favorable power rates. This cost pressure drives industry consolidation and capacity shifts toward regions offering long-term energy price advantages and stable supply.

Growth Factors

Technological Advancements Accelerate Market Expansion

Advanced membrane cell technology cuts energy use by 20 to 30% compared to older diaphragm systems driving plant upgrades globally. New ion-exchange membranes last longer and produce higher-purity caustic soda reducing operating costs and maintenance downtime for modern facilities. These technical gains improve margins and enable competitive pricing in markets with multiple suppliers and price-sensitive customers.

Digital process controls and real-time monitoring boost cell efficiency and predict equipment failures before costly production losses occur. Automation systems optimize power consumption based on electricity pricing and production schedules maximizing economic returns from flexible operations. Smart manufacturing tools help plants meet tighter quality specs and environmental rules while cutting waste and energy intensity.

Integrated chlor-alkali and downstream chemical complexes capture value from both chlorine and caustic soda outputs in balanced operations. Plants producing PVC, epoxy resins, or propylene oxide consume chlorine onsite eliminating transport costs and supply risks. This vertical integration model supports new project development in regions with growing chemical demand and favorable investment climates.

Emerging Trends

Digital Transformation Reshapes Market Landscape

Chlor-alkali makers adopt advanced analytics and machine learning to optimize cell operations and predict maintenance needs with precision. Digital twins simulate plant performance under varying conditions helping operators maximize output and minimize energy consumption in real time. These tools enable proactive upkeep scheduling reducing unplanned shutdowns and extending equipment life in capital-intensive production facilities.

Cloud-based platforms connect multiple plant sites allowing centralized monitoring and performance benchmarking across regional production networks. Makers use data analytics to identify efficiency gaps and share best practices improving overall system productivity and cost competitiveness. Remote operations capabilities also support workforce optimization and safety improvements at hazardous chemical production locations with strict access controls.

Blockchain technology emerges for tracking caustic soda quality and chain of custody in pharma and food applications requiring full traceability. Smart contracts automate supply agreements and payments based on verified product delivery and quality testing results from certified labs. These digital innovations improve transparency and trust in chlor-alkali supply chains serving regulated industries with strict sourcing requirements.

Chlor-Alkali Market Key Companies Insights

Tata Chemicals Limited operates integrated soda ash and salt businesses in India with growing chlor-alkali capacity serving domestic chemical and paper sectors. The company leverages its broad product portfolio and distribution network to capture market share in emerging Asian economies. Recent investments in membrane cell technology and sustainability programs position Tata for long-term growth in environmentally conscious markets.

Occidental Petroleum Corporation runs major chlor-alkali and vinyls operations through its OxyChem division serving North American chemical and building material makers. The company maintains cost leadership through vertical integration and access to low-cost feedstocks from its energy business units. Strategic capacity additions and reliability improvements support stable market share in commodity chemical segments with cyclical demand patterns.

Formosa Plastics Corporation operates large-scale chlor-alkali plants integrated with PVC and specialty chemical production in Taiwan and international locations. The company’s global footprint and diversified product mix provide resilience against regional market volatility and trade disruptions. Formosa invests in advanced manufacturing technology and environmental compliance to meet evolving regulatory standards across its operating regions.

Hanwha Solutions Corporation combines chlor-alkali capacity with solar energy and chemical businesses creating synergies in sustainable manufacturing operations. The company focuses on energy-efficient production methods and renewable power integration to cut carbon footprint and operating costs. Strategic partnerships and technology licensing support Hanwha’s expansion in Asian markets with growing industrial chemical demand and green chemistry adoption.

Key Companies

- Tata Chemicals Limited

- Occidental Petroleum Corporation

- Formosa Plastics Corporation

- Hanwha Solutions Corporation

- AGC, Inc.

- INOVYN

- Wanhua-Borsodchem

- Dow Inc.

- Solvay SA

- Tosoh Corporation

- Olin Corporation

- Westlake Chemical Corporation

- Xinjiang Zhongtai Chemical Co. Ltd.

Recent Development

- January 2025 – Olin Corporation completed membrane cell technology upgrade at its Louisiana plant boosting caustic soda capacity by 15% with improved energy efficiency. This expansion supports growing Gulf Coast chemical demand and reduces the facility’s carbon footprint through advanced electrolysis systems.

- November 2025 – Dow Inc. announced plans to build a new 500,000 ton per year chlor-alkali plant in Texas integrated with downstream PVC production. The project will use state-of-the-art membrane cells and renewable power to meet sustainability targets while serving regional construction markets.

- September 2025 – Solvay SA invested €120 Million in upgrading European chlor-alkali facilities to phase out legacy diaphragm cells by 2026. These conversions align with EU environmental regulations and improve product purity for pharmaceutical and food-grade applications across the region.

- July 2025 – Westlake Chemical Corporation completed acquisition of a 300,000 ton chlor-alkali plant in the Southeast US expanding regional market presence. The deal strengthens Westlake’s vertically integrated vinyls business and provides raw material security for PVC operations during tight supply conditions.

- May 2025 – Tosoh Corporation launched digital monitoring platform across its Japanese chlor-alkali plants cutting energy costs by 8% through optimized operations. The smart manufacturing system uses AI to predict cell performance and schedule maintenance reducing downtime in high-utilization facilities.

- March 2025 – INOVYN signed long-term power purchase agreement for 200 MW of renewable electricity to supply Belgian chlor-alkali operations. This deal supports the company’s carbon neutrality goals and provides stable energy costs for electrolysis-intensive production processes through 2030.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 81.30 Billion |

| Forecast Revenue (2035) | USD 205.19 Billion |

| CAGR (2026-2035) | 9.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Caustic Soda, Chlorine, Soda Ash, Others), By Production Process (Membrane Cell, Diaphragm Cell, Others), By Application (Pulp and Paper, Organic Chemical, Inorganic Chemical, Soap and Detergent, Others), By End User (Chemical Processing and Manufacturing, Textiles, Water and Wastewater Treatment, Aluminum and Metal Processing, Glass Manufacturing, Pharmaceuticals, Food Processing) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Tata Chemicals Limited, Occidental Petroleum Corporation, Formosa Plastics Corporation, Hanwha Solutions Corporation, AGC, Inc., INOVYN, Wanhua-Borsodchem, Dow Inc., Solvay SA, Tosoh Corporation, Olin Corporation, Westlake Chemical Corporation, Xinjiang Zhongtai Chemical Co. Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |