What is the Specialty Polymer Market Size?

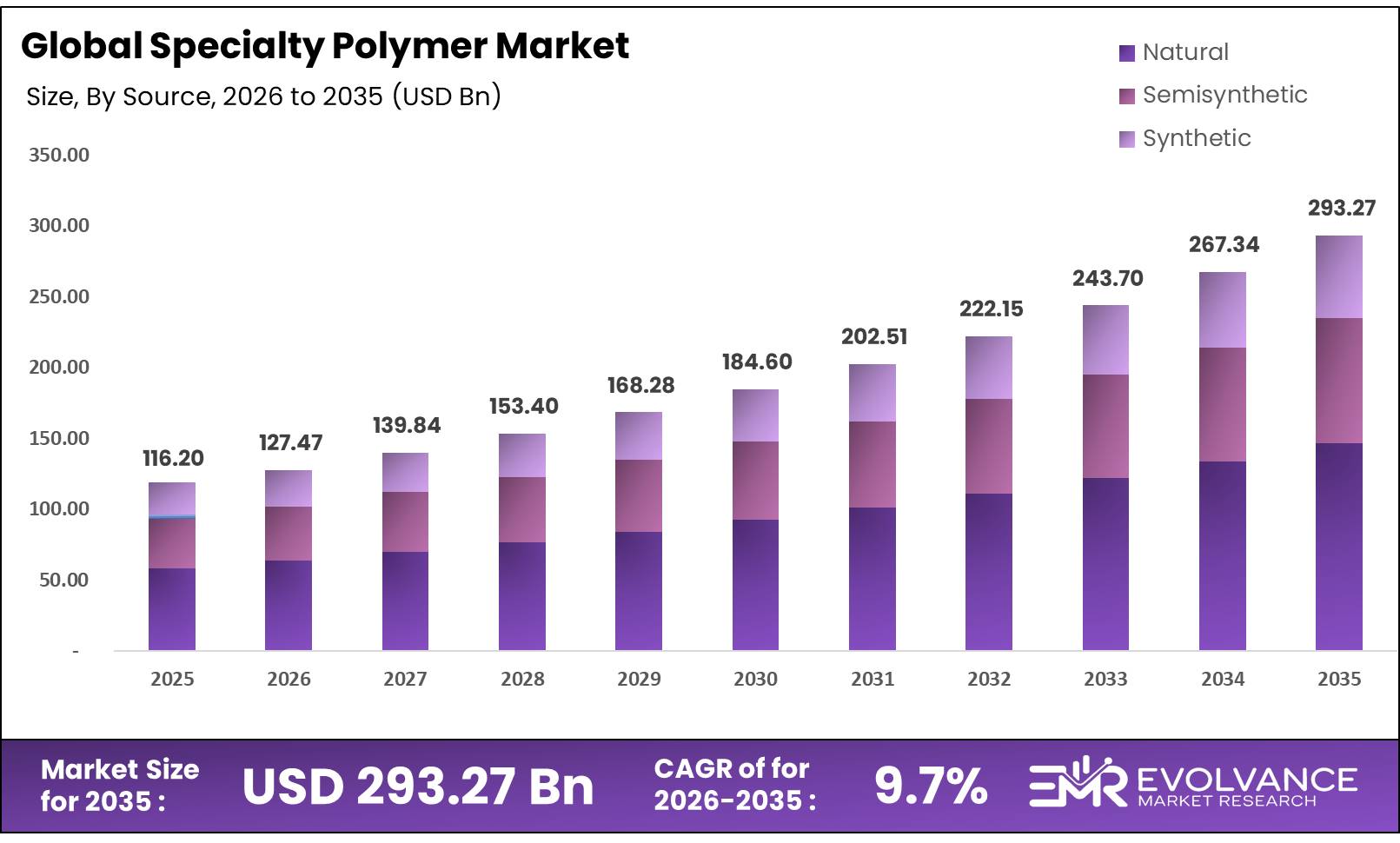

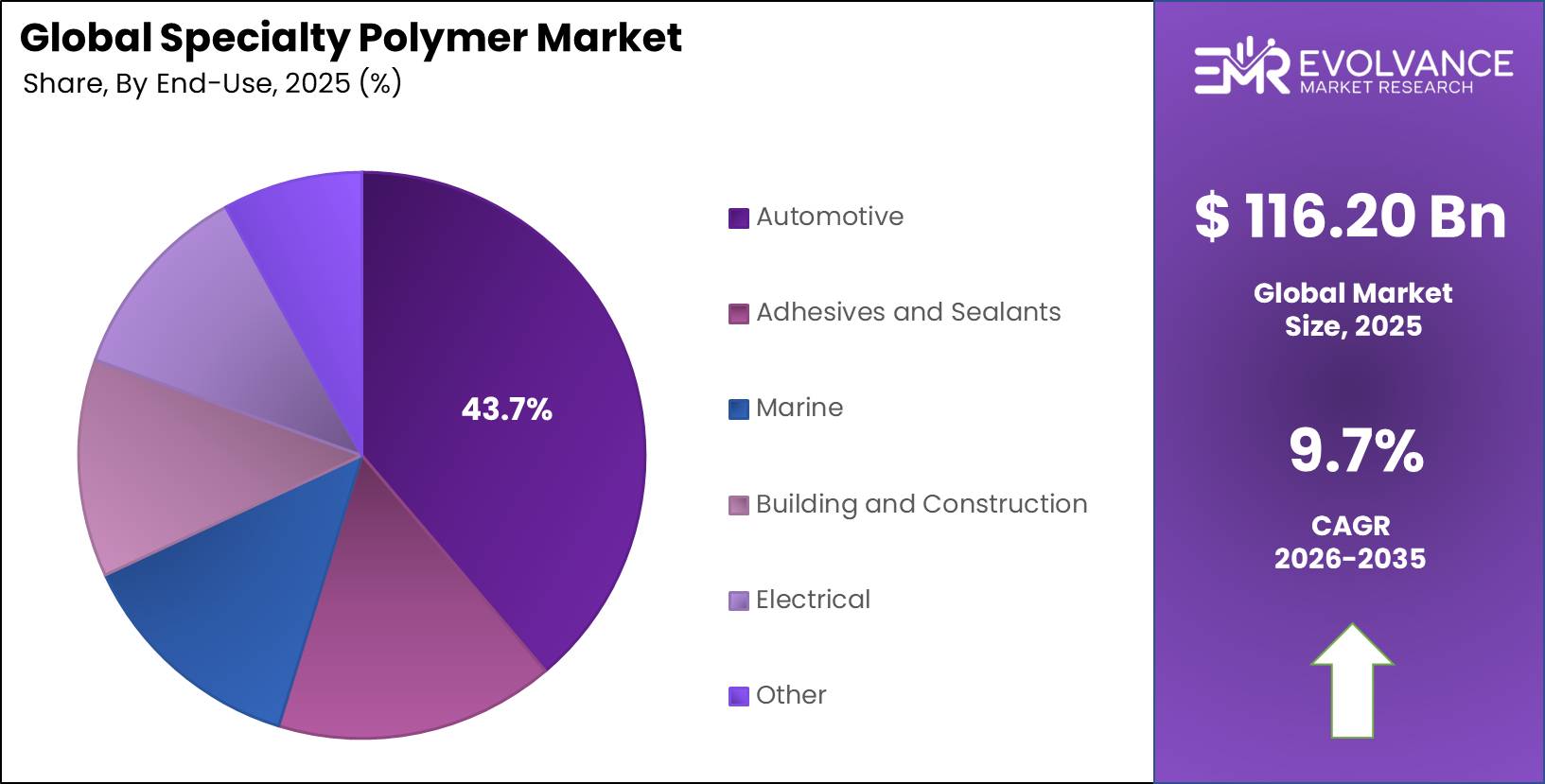

The Global Specialty Polymer Market size will be worth around USD 293.27 Billion by 2035 from USD 116.20 Billion in 2025, growing at a CAGR of 9.7% during the forecast period 2026 to 2035. Rising demand for lightweight, high-performance materials in electric vehicles and aerospace drives this strong growth. Expanding use in medical devices, advanced electronics, and green building projects further supports market gains across all major regions.

Market Highlights

- The Global Specialty Polymer Market is projected to grow from USD 116.2 billion in 2025 to USD 293.2 billion by 2035, registering a CAGR of 9.7%.

- Specialty Elastomers lead the product type segment with a dominant share of 47.5%, driven by high-performance applications.

- Natural sources dominate the source segment, accounting for 51.4% of total market share.

- Injection Molding is the leading processing technology, holding 38.7% of the market due to efficiency and scalability.

- Automotive is the largest end-use segment, contributing 43.7% of overall demand.

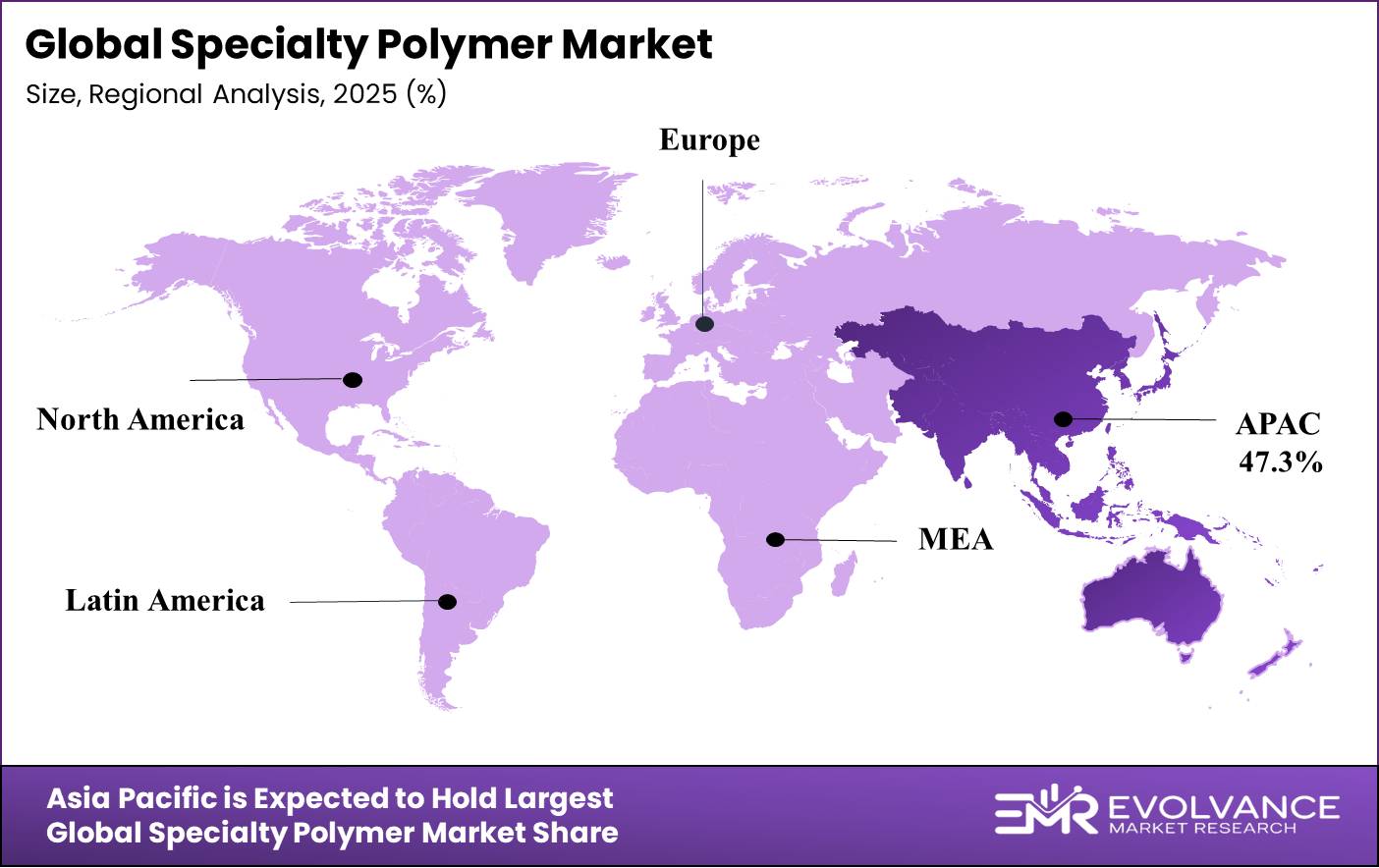

- Asia Pacific is the dominant regional market with a share of 47.3%, valued at USD 54.9 billion.

Market Overview

The specialty polymer market covers a broad range of high-performance materials designed for specific end-use needs. These polymers offer superior thermal, chemical, and mechanical properties compared to standard materials. Industries such as automotive, aerospace, electronics, and healthcare rely on them to meet demanding performance and safety standards.

Specialty polymers serve as key building blocks in modern engineering. They replace metals and conventional materials in many products, cutting weight while improving strength and durability. As design requirements grow more complex, demand for engineered polymer solutions continues to rise across both mature and emerging markets globally.

Arkema S.A., the company posted total sales of €9.5 billion in calendar year 2024, with specialty materials including specialty polymers contributing across Asia, North America, and other key regions. This reflects the scale of commercial activity and ongoing investment in high-performance polymer solutions across global markets.

Evonik Industries AG, the company recorded total revenue of €15.2 billion in fiscal year 2024, which covers its specialty additives and polymer segments. This confirms the strong commercial base that major chemical producers maintain in specialty materials, supporting continued growth and product investment across the forecast period.

The medical sector shows strong growth potential for specialty polymers. Implantable devices, drug delivery systems, and surgical tools all require biocompatible, sterilizable polymer grades. As healthcare systems expand in developing nations, demand for polymer-based medical components will grow at a fast pace over the next decade.

Bio-based and sustainable polymers are gaining traction as companies aim to cut their carbon footprint. Producers are investing in circular economy models and closed-loop recovery systems to meet stricter environmental rules. This shift opens new revenue streams while helping firms align with global sustainability goals and green procurement policies.

Product Type Insights

Specialty Elastomers dominates with 47.5% due to its flexibility, durability, and high-performance application demand.

In 2025, Specialty Elastomers held a dominant market position in the By Product Type segment of the Specialty Polymer Market, with a 47.5% share. These materials offer outstanding flexibility, heat resistance, and sealing performance. Automotive, aerospace, and industrial sectors drive high demand for elastomers in gaskets, hoses, vibration dampers, and protective coatings.

Specialty Thermoplastics represent a fast-growing segment driven by their recyclability and ease of processing. These materials serve a wide range of end uses including connectors, housings, and structural components in electronics and automotive. Their ability to be reprocessed makes them attractive as sustainability requirements grow tighter across major end-use industries.

Specialty Thermosets deliver excellent chemical resistance and dimensional stability in demanding environments. They are widely used in aerospace composites, electrical laminates, and industrial coatings where permanent cross-linked structures are needed. Growing aerospace and wind energy sectors continue to drive steady demand for thermoset-based polymer solutions globally.

Biodegradable Polymers are gaining ground as brands and regulators push for greener packaging and disposable medical products. These materials break down naturally, reducing plastic waste in landfills and oceans. Government bans on single-use plastics and rising consumer awareness continue to accelerate the shift toward biodegradable polymer grades worldwide.

Source Insights

Natural dominates with 51.4% owing to rising preference for renewable and eco-friendly polymer sources.

In 2025, Synthetic polymers held the leading position in the By Source segment of the Specialty Polymer Market, with a 51.4% share. Derived from petrochemical feedstocks, these polymers offer precise, repeatable performance across a wide range of applications. High-volume industries such as automotive, electronics, and construction rely on synthetic grades for consistent quality at commercial scale.

Natural polymers, including rubber, cellulose, and starch-based materials, serve niche markets where biocompatibility and sustainability are key. They find use in medical, food packaging, and textile applications. As interest in bio-based solutions grows, natural polymer variants are being engineered to match synthetic performance levels in selected uses.

Semisynthetic polymers blend natural and synthetic chemistry to achieve tailored properties. They are commonly used in pharmaceutical coatings, specialty films, and textile finishing. Semisynthetic grades allow producers to balance sustainability credentials with the processing reliability needed for high-volume industrial and consumer product applications.

Processing Technology Insights

Injection Molding dominates with 38.7% due to its efficiency, precision, and high-volume production capability.

In 2025, Injection Molding held a dominant market position in the By Processing Technology Analysis segment of Specialty Polymer Market, with a 38.7% share. Its dominance is driven by mass production efficiency, design flexibility, and suitability for complex, high-precision polymer components.

Extrusion is a widely used process for producing pipes, films, sheets, and profiles from specialty polymer compounds. It suits continuous production of building, packaging, and wire coating products. Advances in twin-screw extrusion systems allow producers to blend multiple polymer grades and additives with better control and output consistency.

3D Printing and Additive Manufacturing is one of the fastest-growing processing segments in the specialty polymer space. It enables on-demand production of complex, custom parts in aerospace, medical, and industrial sectors. As polymer feedstock quality for additive systems improves, adoption rates in both prototyping and end-use part production are rising steadily.

Thermoforming and other processes including compression molding, rotational molding, and blow molding serve specific end markets where sheet forming or hollow structures are needed. These technologies support packaging, tanks, automotive interiors, and protective covers. Continued advances in polymer grades compatible with these processes are expanding their commercial range.

End Use Insights

Automotive dominates with 43.7% driven by lightweighting trends and demand for high-performance materials.

In 2025, Automotive held a dominant position in the By End Use segment of the Specialty Polymer Market, with a 43.7% share. Automakers replace metal parts with high-performance polymers to cut vehicle weight and improve fuel efficiency. Electric vehicle platforms accelerate this trend by requiring heat-resistant and electrically insulating polymer components in battery systems and powertrains.

Electrical applications represent a major and growing end-use category for specialty polymers. High-dielectric materials, flame-retardant housings, and heat-resistant insulation support advanced electronics, power systems, and semiconductor packaging. Rapid expansion of data centers, 5G networks, and EV charging infrastructure is driving sustained demand for polymer solutions in this segment.

Building and Construction uses specialty polymers in pipes, membranes, adhesives, and thermal insulation products. These materials offer corrosion resistance, durability, and low maintenance in harsh environments. Growing infrastructure investment in Asia Pacific and the Middle East is fueling demand for polymer-based construction products with long service life and high load performance.

Adhesives and Sealants and Marine applications together form a significant share of specialty polymer end use. Marine coatings, hull materials, and offshore components rely on polymers with outstanding resistance to saltwater, UV, and biofouling. Growth in renewable offshore energy and shipbuilding activity in Asia continues to create new market pull in this segment.

Market Segments Covered in the Report

By Product Type

- Specialty Elastomers

- Fluoroelastomers

- Fluorosilicone Rubber

- Liquid Silicone Rubber

- Natural Rubber

- Others

- Specialty Thermoplastics

- Polyolefins

- Polyimides

- Vinylic Polymer

- Polyphenyles

- Others

- Specialty Thermosets

- Epoxy

- Polyester

- Vinyl Ester

- Polyimides

- Others

- Biodegradable Polymers

- Liquid Crystal Polymers

- Others

By Source

- Natural

- Semisynthetic

- Synthetic

By Processing Technology

- Injection Molding

- Compression Molding

- Rotational Molding

- Extrusion

- Blow Molding

- Thermoforming

- 3D Printing and Additive Manufacturing

By End Use

- Automotive

- Adhesives and Sealants

- Marine

- Building and Construction

- Electrical

- Other

Regional Insights

Asia Pacific Dominates the Specialty Polymer Market with a Market Share of 47.3%, Valued at USD 54.9 Billion

Asia Pacific leads the global Specialty Polymer Market with a 47.3% share valued at USD 54.9 Billion. China, Japan, South Korea, and India anchor this regional dominance through large-scale chemical production, advanced electronics manufacturing, and fast-growing automotive sectors. In 2024, China exported USD 2.77 billion of propylene polymers, reflecting the region’s deep production and trade base in specialty polymer materials.

North America Trends

North America holds a strong position in the global specialty polymer space, led by the United States. The region benefits from advanced aerospace, defense, and medical device industries that demand high-performance polymer grades. Strong R&D activity, access to petrochemical feedstocks, and growing EV production continue to drive steady demand for specialty polymer solutions across industrial and consumer end markets.

Europe Specialty Trends

Europe focuses on sustainable and high-performance polymer development, driven by strict EU environmental rules and carbon reduction targets. Germany, France, and the UK lead regional consumption across automotive, construction, and electronics sectors. The EU’s circular economy policies push producers toward recyclable and bio-based polymer alternatives, creating new growth areas for specialty materials across both established and emerging European markets.

Latin America Market Trends

Latin America shows steady market growth, led by Brazil and Mexico as the key consuming nations. Expanding automotive assembly, construction activity, and food packaging demand drive polymer consumption in the region. Foreign investment in manufacturing and rising middle-class purchasing power are accelerating the use of specialty materials across automotive, consumer goods, and infrastructure development projects throughout the region.

Middle East and Africa Market Trends

The Middle East and Africa region presents growing investment opportunities for specialty polymer producers and distributors. GCC nations are diversifying from oil exports by building downstream chemical and polymer production capacity. Infrastructure mega-projects across Saudi Arabia, UAE, and South Africa require durable, corrosion-resistant polymer components. These demand drivers position the region as an emerging growth market over the forecast period.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The EU’s REACH regulation continues to shape specialty polymer production and trade in Europe. Updated guidance issued in 2024 tightens restrictions on substances of very high concern (SVHC) used in polymer processing. Producers must demonstrate compliance with registration, evaluation, and authorization requirements, raising the compliance bar for both domestic producers and importers supplying the European market.

In 2025, the US EPA updated its Toxic Substances Control Act (TSCA) rules to expand reporting and review requirements for new polymer chemistries. Companies launching novel specialty polymer grades must now submit more detailed environmental and health risk data before commercial release. This adds time and cost to product launches but also raises quality and safety standards across the North American market.

Asian governments are also tightening polymer-related rules. China’s GB standards for polymer materials in food contact, medical devices, and electrical insulation were revised in 2024, aligning more closely with international norms. These changes require producers to retest and requalify existing product lines, adding compliance costs but also creating differentiation opportunities for producers with advanced quality management systems already in place.

Emerging Trends

Nanotechnology, Circular Economy Models, and OEM Partnerships Redefine the Specialty Polymer Landscape

Nanotechnology is reshaping specialty polymer performance by enabling precise control of mechanical and thermal properties at the molecular level. Nano-fillers such as carbon nanotubes and graphene enhance strength, conductivity, and barrier performance without adding significant weight. Producers integrating nanocomposite technology into their product lines gain a clear edge in demanding automotive, aerospace, and electronics applications.

High-temperature resistant polymers are seeing rising adoption in automotive under-the-hood systems as engine and powertrain designs evolve. Electric vehicles require polymer insulation and components that perform reliably at elevated thermal loads near battery packs and power electronics. Grades such as PEEK, PPS, and specialty polyimides are gaining specification wins as automakers redesign thermal management systems for next-generation platforms.

Strategic partnerships between polymer producers and original equipment makers are accelerating the development of custom material solutions. These co-development programs let producers align polymer grade design with exact performance targets set by OEM customers. At the same time, producers are building closed-loop recovery programs to reclaim and reprocess used polymer components, advancing circular economy goals while creating new cost-efficient supply models.

Drivers

Surging Demand for Lightweight, High-Performance Polymer Materials Powers Market Expansion

Aerospace and electric vehicle makers actively replace metal parts with specialty polymers to cut weight and improve energy efficiency. High-performance polymer grades deliver the thermal and mechanical properties needed in battery housings, structural panels, and under-the-hood components. This shift is accelerating as automakers face tighter emission targets and range requirements across global vehicle platforms.

Advanced electronics and semiconductor production create strong pull for specialty polymers with precise dielectric and thermal properties. Chip packaging, printed circuit boards, and high-frequency communication components rely on engineered polymer grades for performance and reliability. As global semiconductor capacity expands, especially in Asia and North America, demand for these advanced polymer materials grows in parallel.

Medical device makers are increasing their use of specialty polymers in implants, surgical tools, and diagnostic equipment. These applications require biocompatible, sterilizable, and chemically stable materials that meet strict regulatory standards. Growing healthcare spending in Asia, the Middle East, and Latin America is expanding the addressable market for medical-grade specialty polymer solutions globally.

Restraints

Volatile Feedstock Prices and Environmental Rules Create Headwinds for Market Growth

Specialty polymer producers depend heavily on petrochemical feedstocks such as ethylene, propylene, and benzene. Sharp price swings in crude oil and natural gas disrupt production cost planning and squeeze profit margins. Manufacturers struggle to pass on all cost increases to customers in competitive markets, leading to reduced investment in new grades and capacity expansion during high-price periods.

Strict environmental rules on polymer processing and waste disposal raise compliance costs for producers in Europe, North America, and Asia. Regulations limit the use of certain additives, solvents, and processing aids, requiring reformulation of established product lines. Smaller producers with limited R&D resources face the greatest burden, as meeting evolving standards demands both technical expertise and capital spending on cleaner process technologies.

High capital needs for advanced polymerization technology limit market entry and expansion for mid-size and smaller producers. Building or upgrading plants for high-performance fluoropolymers, liquid crystal polymers, and specialty thermosets requires hundreds of millions in investment. Limited recycling systems for thermosets and fluoropolymers add to end-of-life cost concerns, reducing long-term appeal for some buyers with circular economy commitments.

Growth Factors

Sustainability, 5G Expansion, and Additive Manufacturing Open New Growth Paths for Specialty Polymers

Bio-based specialty polymers are attracting growing interest from manufacturers seeking to cut carbon emissions and meet green procurement standards. Producers are investing in plant-derived feedstocks and closed-loop recovery systems to develop sustainable alternatives to petroleum-based grades. These bio-circular materials command premium pricing in automotive, packaging, and medical applications where environmental credentials are a key buying factor.

The global rollout of 5G networks and advanced communication systems is driving fast-growing demand for high-dielectric, low-loss polymer materials. Antennas, base stations, and high-speed data cables all require specialty polymer grades that perform reliably at millimeter-wave frequencies. This segment will see strong volume growth as 5G infrastructure buildout accelerates through 2030 across Asia, North America, and Europe.

Additive manufacturing is opening new application windows for specialty polymers in aerospace, medical, and industrial tooling sectors. High-performance polymer filaments and powders for 3D printing are replacing traditional materials in low-volume, complex parts. As printer resolution and material quality improve, producers who develop certified polymer feedstocks for additive systems will capture premium margins and long-term supply agreements with key OEM customers.

Key Companies Insights

In the evolving landscape of the Specialty Polymer Market in 2025, several key players continue to shape innovation, sustainability, and competitive positioning.

Arkema S.A. is a global leader in specialty materials, posting total sales of €9.5 billion in 2024 across operations in 55 countries and 157 production plants. The company’s portfolio covers specialty polyamides, fluoropolymers, and performance resins under brands such as Rilsan. In January 2026, Arkema brought online a new Rilsan Clear production unit in Singapore, tripling global transparent polyamide capacity through a USD 20 million investment.

Dow Inc. holds a strong global position in specialty and performance polymers, serving automotive, packaging, infrastructure, and consumer markets. The company invests heavily in sustainable polymer solutions, including bio-based and recyclable grades aligned with circular economy goals. Dow’s broad product range and deep customer relationships in North America, Europe, and Asia Pacific make it a key supplier to high-growth end-use segments worldwide.

BASF SE brings one of the widest specialty polymer portfolios in the industry, covering engineering plastics, polyurethanes, and high-performance resins. The company serves automotive, electronics, construction, and agricultural end markets with tailored material solutions. BASF’s global R&D network allows it to co-develop polymer grades with major OEM customers, supporting faster product qualification and specification wins across key growth applications.

Evonik Industries AG reported total revenue of €15.2 billion in fiscal year 2024, with specialty additives and polymer materials forming a core part of its business mix. The company focuses on high-margin niches including specialty polyamides, silicones, and functional polymer additives for healthcare and advanced industries. Evonik’s strong IP base and application engineering capabilities support its position as a premium partner to technically demanding customers.

Key Companies

- Arkema S.A.

- Dow Inc.

- Clariant AG

- BASF SE

- 3M Company

- Evonik Industries AG

- Solvay S.A.

- Croda International Plc

- Specialty Polymers, Inc.

- PolyOne Corporation (now Avient Corporation)

Recent Development

- January 2026 – Arkema S.A. started up its new Rilsan Clear production unit in Singapore, tripling global transparent polyamide capacity. The USD 20 million facility on Jurong Island strengthens the company’s specialty polymer footprint in Asia Pacific.

- July 2025 – Arkema S.A. expanded PA-11 (Rilsan) production capacity by 50% at its Singapore plant on Jurong Island. This expansion supports growing demand for bio-circular specialty polymers across key sectors in the Asia Pacific region.

- May 2024 – Arkema S.A. confirmed total sales of €9.5 billion for calendar year 2024, with specialty materials contributing strong volumes across Asia, North America, and other regions. The results reflect broad commercial momentum across its advanced polymer product lines.

- FY 2024 – Evonik Industries AG posted total revenue of €15.2 billion for fiscal year 2024, with adjusted EBITDA of approximately €2.065 billion. Performance in specialty additives and polymer segments contributed to the company’s overall financial results for the period.

- FY 2023-24 – Ester Industries Limited reported consolidated revenue of ₹1,090 crores for fiscal year 2023-24. The company’s specialty polymers division posted revenue of ₹99.5 crores, compared to ₹197.5 crores in the prior year, reflecting a shift in product mix and market conditions.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 116.2 Billion |

| Forecast Revenue (2035) | USD 293.2 Billion |

| CAGR (2026-2035) | 9.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2021-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Competitive Landscape, Recent Developments, New Trends, Revenue Forecast |

| Segments Covered | By Product Type (Specialty Elastomers (Fluoroelastomers, Fluorosilicone Rubber, Liquid Silicone Rubber, Natural Rubber, Others), Specialty Thermoplastics (Polyolefins, Polyimides, Vinylic Polymer, Polyphenyles, Others), Specialty Thermosets (Epoxy, Polyester, Vinyl Ester, Polyimides, Others), Biodegradable Polymers, Liquid Crystal Polymers, Others), By Source (Natural, Semisynthetic, Synthetic), By Processing Technology (Injection Molding, Compression Molding, Rotational Molding, Extrusion, Blow Molding, Thermoforming, 3D Printing and Additive Manufacturing), By End Use (Automotive, Adhesives and Sealants, Marine, Building and Construction, Electrical, Other) |

| Regional Analysis | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Competitive Landscape | Arkema S.A., Dow Inc., Clariant AG, BASF SE, 3M Company, Evonik Industries AG, Solvay S.A., Croda International Plc, Specialty Polymers, Inc., PolyOne Corporation (now Avient Corporation) |