What is the Goat Milk Infant Formula Market Size?

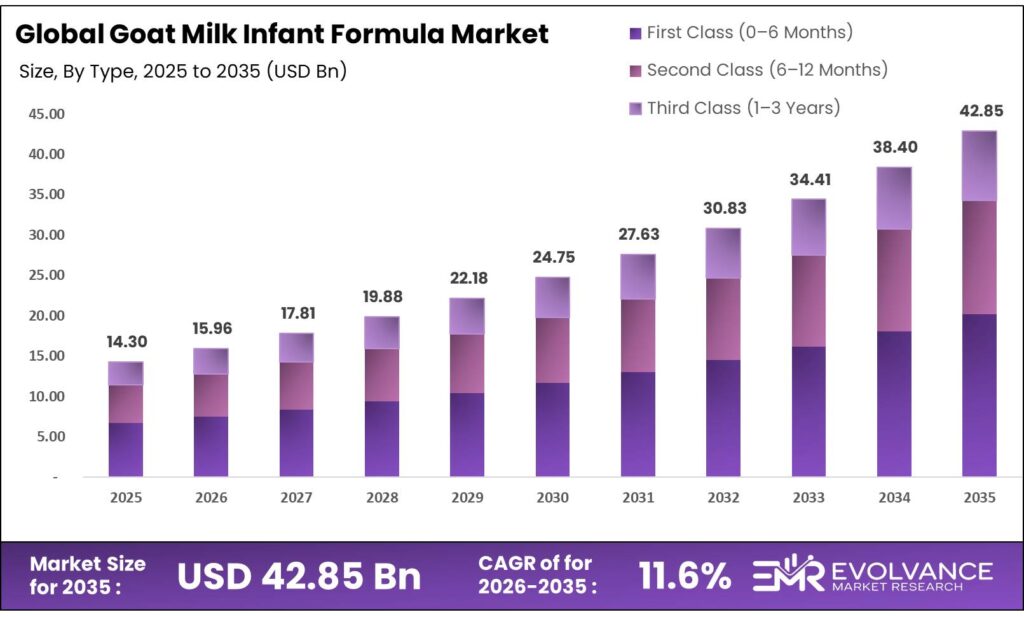

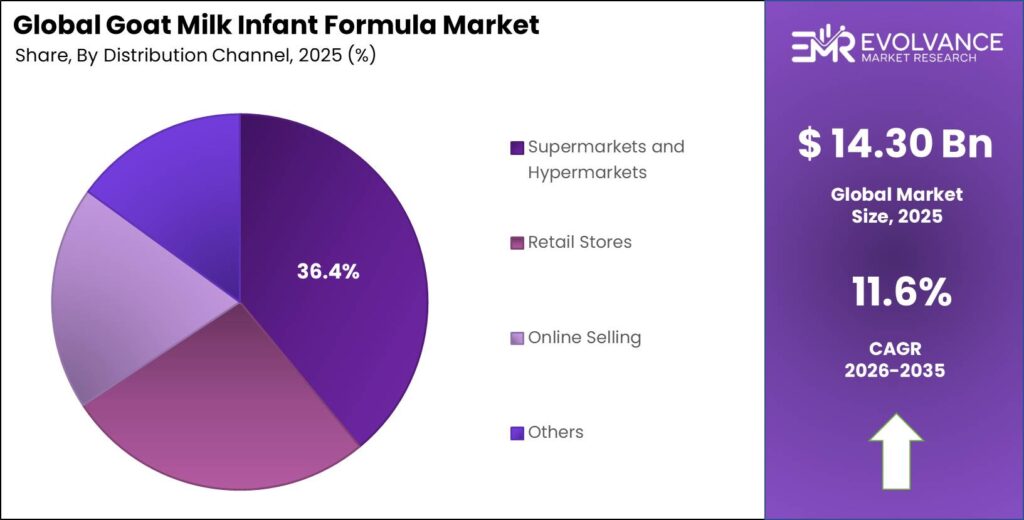

The Global Goat Milk Infant Formula Market size will be worth around USD 42.85 Billion by 2035 from USD 14.30 Billion in 2025, growing at a CAGR of 11.6% during the forecast period 2026 to 2035. Parents seeking alternatives to cow milk-based formula are choosing goat milk products for their digestibility profile, pushing spend into premium nutrition tiers. Buyers in China and the US are shifting toward imported, certified products — a pattern that lifts both volume and average selling price. Supply is tightly tied to goat milk sourcing regions, making raw material access a real constraint for brands trying to scale fast.

Market Highlights

- The Global Goat Milk Infant Formula Market valued at USD 14.30 Billion in 2025, forecast to reach USD 42.85 Billion by 2035, at a CAGR of 11.6%.

- Asia-Pacific leads all regions with a 47.3% share, valued at USD 6.7 Billion.

- Bottle Packaging dominates the packaging segment with a 67.2% share.

- First Class (0–6 Months) formula holds the largest type segment share at 44.3%.

- Supermarkets and Hypermarkets lead distribution with a 36.4% share.

Market Overview

The goat milk infant formula market covers nutritional products made from goat milk for infants aged 0 to 3 years. These formulas serve as alternatives to cow milk-based products in that Protein Hydrolysate and sold across three age-specific classes. Demand is concentrated in markets where parents prioritize clean-label, premium nutrition for newborns and toddlers.

Manufacturers develop goat milk formulas to meet strict national food safety standards in each target market. The US FDA, European food authorities, and China’s regulatory body each set distinct requirements for composition, labeling, and testing. Meeting all three regulatory frameworks is costly and time-intensive, which naturally limits the number of players who can compete globally.

According to World Bank trade data, China imported preparations for infant use valued at USD 4,294,936 thousand with a quantity of 237,914,000 kg in 2023, making it the world’s largest importer. This confirms that no brand can ignore China when planning volume strategy — the import scale dwarfs every other single-country market.

Based on data from World Bank WITS, the United States imported infant formula preparations valued at USD 353,484 thousand and exported USD 312,280 thousand worth in 2023. The US runs a net import position, which signals that domestic production does not fully meet demand — creating a real opening for certified foreign goat milk brands willing to navigate FDA compliance.

Government policy in key markets is reshaping how goat milk formula enters retail. The FDA’s voluntary recall of Crecelac and Farmalac in May 2024 showed that regulatory enforcement is active, not passive. Brands with full compliance and independent certification hold a real edge — non-compliant products face removal from shelves and lost consumer trust.

Type Insights

First Class (0–6 Months) dominates with 44.3% due to highest parental spend at birth stage.

In 2025, First Class (0–6 Months) held a dominant market position in the By Type segment of the Goat Milk Infant Formula Market, with a 44.3% share. Parents make their most critical and emotional nutrition decisions in the first six months of life. This creates strong brand loyalty that carries forward into later stages — making Stage 1 the highest-leverage entry point for any formula brand. Kabrita’s 2024 FDA-compliant US launch targeted this segment directly, achieving the European brand ranking on Amazon within one year, which confirms that first-mover positioning in Stage 1 drives outsized commercial returns.

Second Class (6–12 Months) serves as a follow-on stage where brand continuity from Stage 1 drives most purchase decisions. Parents who establish trust with a brand in the first six months rarely switch at the follow-on stage. This loyalty dynamic makes Stage 2 revenue largely a function of Stage 1 acquisition success, rather than a standalone competitive battle. Vendors who win the first purchase effectively secure the second.

Third Class (1–3 Years) covers toddler formula, a segment where retail visibility and on-shelf positioning matter more than in the infant stages. Toddlers are mobile, families are less anxious, and repeat purchase is driven more by price and convenience than health urgency. However, premium brands that entered at Stage 1 can still retain buyers here through brand trust built during the high-stakes early months.

Packaging Type Insights

Bottle Packaging dominates with 67.2% due to airtight preservation and consumer familiarity.

In 2025, Bottle Packaging held a dominant market position in the By Packaging Type segment of the Goat Milk Infant Formula Market, with a 67.2% share. Tin and hard-shell bottle formats preserve powder quality over longer shelf lives, which is critical for imported premium products shipped across long supply chains. Parents also associate sealed bottle packaging with quality assurance — a perception that aligns with the premium positioning most goat milk brands actively cultivate.

Tetra Packaging offers a lighter, lower-cost format suited to ready-to-use liquid formulas and follow-on products. While its share trails bottle formats significantly, Tetra is gaining ground in markets where convenience is a higher priority than premium perception. Urban working parents in Asia-Pacific represent the clearest near-term demand pool for Tetra-format goat milk formula.

Distribution Channel Insights

Supermarkets and Hypermarkets dominate with 36.4% due to parent preference for in-person product evaluation.

In 2025, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the Goat Milk Infant Formula Market, with a 36.4% share. Parents buying infant formula for the first time strongly prefer physical retail — they read labels, compare products, and seek in-store advice. Kabrita’s nationwide rollout at Whole Foods Market and Sprouts Farmers Market in 2025 demonstrates that premium goat milk brands are actively targeting this channel to build credibility alongside online presence.

Retail Stores serve local markets where convenience and price sensitivity are higher than in premium specialty channels. These outlets are critical in second-tier cities and regional markets across Asia-Pacific and Latin America. For brands expanding internationally, entry through local retail chains often precedes or replaces the premium channel strategy used in the US and Europe.

Online Selling is the fastest-scaling channel for goat milk infant formula, as shown by Oli6’s 115% year-on-year sales rise during China’s Double 11 festival in 2024. Cross-border e-commerce gives international brands direct access to Chinese parents without a physical retail presence, cutting the time and cost of traditional market entry. For premium brands with certification stories to tell, the online channel is where that narrative converts to purchase.

Others includes pharmacies, specialty health stores, and direct-to-consumer models. This channel is smaller by volume but high in trust value — pharmacy placements signal medical credibility, which matters especially for parents whose infants have digestive sensitivities and are specifically seeking goat milk alternatives.

Market Segments Covered in the Report

By Type

- First Class (0–6 Months)

- Second Class (6–12 Months)

- Third Class (1–3 Years)

By Packaging Type

- Bottle Packaging

- Tetra Packaging

By Distribution Channel

- Supermarkets and Hypermarkets

- Retail Stores

- Online Selling

- Others

Goat Milk Infant Formula Market Regional Insights

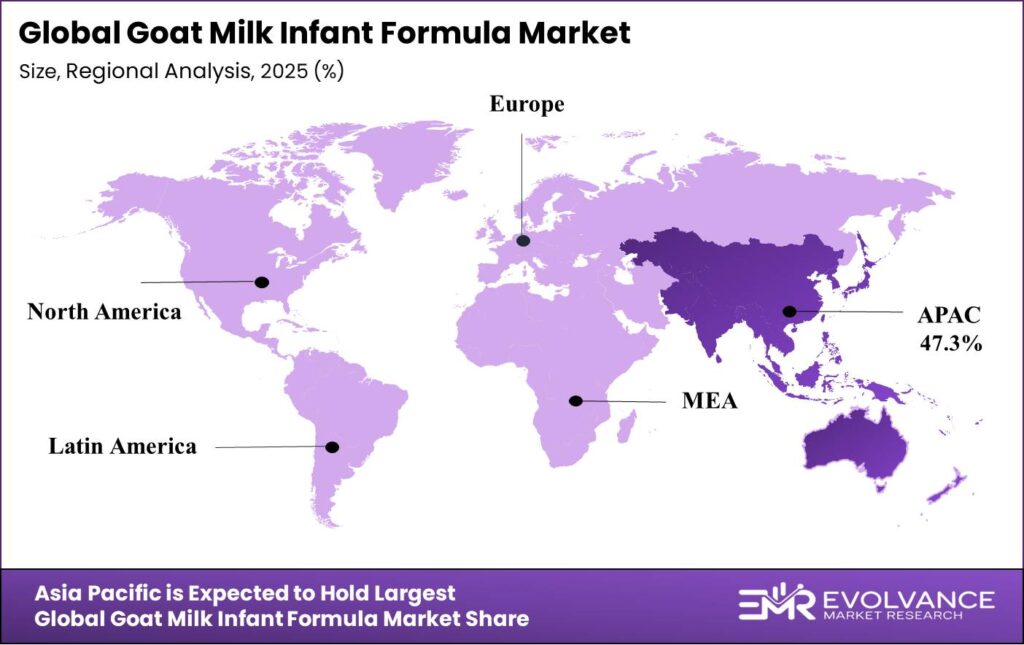

Asia-Pacific Dominates the Goat Milk Infant Formula Market with a Market Share of 47.3%, Valued at USD 6.7 Billion

Asia-Pacific holds a 47.3% share worth USD 6.7 Billion, driven by China’s position as the world’s largest importer of infant formula. China’s top import sources in 2023 were the EU (USD 2.56 Billion), Netherlands (USD 1.67 Billion), and New Zealand (USD 752 Million). Ausnutria’s goat milk revenue reaching RMB 1,865 Million with a 30.4% China market share confirms that the region is both the largest and most competitive arena for goat milk formula globally.

North America Market Trends

North America is the most structurally complex market for goat milk formula entry, given the FDA’s multi-year clinical review requirement before US market clearance. Kabrita’s January 2024 FDA-compliant launch and its achievement of the European brand ranking on Amazon within one year show that regulatory compliance converts directly into first-mover commercial advantage. US infant formula imports totaled USD 353,484 thousand in 2023, with Ireland as the largest single source.

Europe Market Trends

Europe is the primary sourcing and certification hub for premium goat milk formula exported globally. Kabrita’s formula became the first to earn Clean Label Project’s First 1,000 Day Promise, Pesticide Free, and Purity certifications — a standard built on European heritage spanning 75+ years and more than 90 quality checks. European brands carry outsized credibility in Asian and US markets, giving them pricing power that local producers cannot easily match.

Latin America Market Trends

Latin America is an emerging growth region for goat milk formula, where rising middle-class incomes and awareness of premium infant nutrition are beginning to shift purchase behavior away from standard cow milk products. Brazil and Mexico lead regional demand. Distribution is primarily through local retail and pharmacy chains. International brands entering this region face the challenge of price positioning in markets where premium products require stronger consumer education to justify the cost gap.

Middle East and Africa Market Trends

Middle East and Africa represent an early-stage market for goat milk formula, with demand concentrated in GCC countries where high incomes support premium infant nutrition spending. Goat farming is culturally embedded in parts of this region, which creates both familiarity with goat-derived products and potential for local production partnerships. Import channels currently dominate supply, with European and New Zealand brands leading product availability in GCC retail.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The US FDA completed its multi-year clinical testing and full review process for goat milk infant formula before granting market entry clearance. This process sets a high bar — only brands that meet all composition and safety specs can sell legally in the US. The result is a market protected from low-quality entrants but also slower to open for new legitimate brands seeking access.

In May 2024, the FDA published a voluntary recall of Crecelac and Farmalac powdered goat milk infant formulas. The recall confirmed that the FDA actively enforces compliance and does not allow unregistered products to remain on shelves. For compliant brands, this enforcement action strengthens their competitive position by removing non-compliant rivals from the market.

Kabrita became the first and only brand to achieve Clean Label Project’s First 1,000 Day Promise, Pesticide Free, and Purity certifications as of June 27, 2024. While these are independent third-party certifications rather than government mandates, they function as de facto standards in the premium US channel. Retailers like Whole Foods Market use such certifications as shelf-entry criteria, making them commercially binding for brands targeting premium distribution.

In Europe, goat milk formula is regulated under EU Commission rules on infant formula composition. European standards require strict nutrient profiles and prohibit unauthorized additives. These rules align with the standards promoted by Kabrita’s 75+ years of European heritage and 90+ quality checks, which it uses as proof of compliance in its US marketing and certification campaigns.

Goat Milk Infant Formula Market Dynamics

Drivers

FDA Compliance Clearance and Retail Expansion Drive US Market Entry for Goat Milk Formula Brands

Kabrita’s January 2024 FDA-compliant launch marked the first time a European goat milk formula met all US FDA requirements for infant use. This clearance removed the single largest barrier to US market entry for premium goat milk brands. The commercial outcome was fast — Kabrita became the European brand on Amazon within one year, showing that regulatory clearance directly converts to sales velocity.

Following FDA approval, Kabrita achieved nationwide availability at Whole Foods Market and Sprouts Farmers Market. This brick-and-mortar rollout matters because premium specialty retail is where US parents discover and trial new formula brands. Physical shelf presence in these chains validates product quality in a way that online-only presence cannot replicate for first-time buyers.

Moreover, Ausnutria’s goat milk infant formula revenue reached RMB 1,865 Million with a 3.1% year-on-year gain and China market share rising 2.8 percentage points to 30.4% by end-June 2025. This shows that the largest goat milk market in the world is still consolidating around a small number of dominant brands. Vendors with early distribution depth and market share in China hold a structural advantage that late entrants will find expensive to overcome.

Restraints

Multi-Year FDA Review Process and Voluntary Recalls Raise Entry Barriers and Compliance Costs

The FDA requires a full multi-year clinical testing and review process before any goat milk infant formula can enter the US market legally. This timeline adds years and millions in testing costs before a single unit is sold. For smaller brands and new market entrants, this barrier is effectively prohibitive without significant outside investment or a partnership with an established regulatory affairs team.

The May 2024 voluntary recall of Crecelac and Farmalac powdered goat milk infant formulas illustrates how quickly non-compliant products are removed from the market. Recalls damage brand reputation and erode retailer trust — effects that persist well beyond the recall event itself. A single compliance failure can cost a brand years of market-building effort.

Additionally, compliance costs do not end at approval. Ongoing testing, label verification, and periodic regulatory updates require continuous investment. Brands operating across multiple markets — the US, EU, and China simultaneously — face compounding compliance costs that compress margins, particularly for mid-size players without the scale to absorb these expenses efficiently.

Growth Factors

China’s Import Dependency and Ausnutria’s Market Share Create Platform for Accelerated International Growth

China imported infant formula preparations worth USD 4,294,936 thousand in 2023, with the EU supplying USD 2.56 Billion and New Zealand contributing USD 752 Million. This import dependency gives compliant international brands a structural entry route that does not require local manufacturing. Brands with EU origin and clean-label credentials are particularly well-placed to capture share in China’s premium import segment.

Ausnutria’s 84% dominance of China’s imported goat milk formula segment, combined with its 30.4% overall China market share, shows that the top players in this market benefit from compounding scale advantages. Each percentage point of share gained translates into greater retailer negotiating power and higher brand recall during purchase decisions. Competitors seeking to enter China must build against this entrenched position.

Furthermore, Bubs Australia received GRAS confirmation for whole goat milk powder use at up to 20% w/w in non-exempt infant formula. This regulatory milestone opens a new formulation pathway that competitors have not yet used at scale. Brands that move quickly to incorporate this approved ingredient can differentiate their product against the existing field before the approach becomes standard practice.

Emerging Trends

Cross-Border E-Commerce and Purity Certifications Reshape How Premium Goat Milk Brands Build Global Scale

Oli6’s goat milk infant formula achieved 115% year-on-year sales growth during China’s Double 11 festival in 2024, driven entirely by cross-border e-commerce. This result proves that international brands can build meaningful revenue in China without physical retail infrastructure. The platform shifts distribution power from traditional import agents to brand-controlled digital channels, cutting costs while accelerating reach.

Kabrita’s achievement of the Clean Label Project’s First 1,000 Day Promise, Pesticide Free, and Purity certifications on June 27, 2024 established a new benchmark for premium product claims. These certifications are now a competitive requirement for brands targeting health-conscious US parents and premium retail buyers. Brands without independent purity testing will struggle to enter or hold shelf space in the channels where goat milk formula commands the highest prices.

Additionally, ongoing FDA enforcement actions — including the May 2024 recall of Crecelac and Farmalac — are accelerating market consolidation around certified, compliant brands. As unregistered products exit the market, compliant brands absorb their volume. This regulatory-driven consolidation is creating a narrowing window during which well-positioned brands can gain share at lower competitive cost before the market fully consolidates.

Key Companies Insights

AUSNUTRIA holds a commanding position in the goat milk formula space, with goat milk revenue reaching RMB 1,865 Million and a 30.4% overall China market share by end-June 2025. Its 84% dominance in China’s imported goat milk segment shows deep retail penetration built over years. Ausnutria’s scale gives it procurement and distribution leverage that smaller brands cannot replicate quickly, making it the benchmark competitor in the Asia-Pacific region.

Kabrita executed the most significant regulatory and commercial milestone in the US market in 2024 by launching the first and only European goat milk infant formula fully meeting all FDA requirements. Within one year of launch, it became the European formula brand on Amazon. Its nationwide rollout at Whole Foods Market and Sprouts in 2025, combined with Clean Label Project certifications achieved in June 2024, has established Kabrita as the premium standard for goat milk formula in the US premium channel.

Oli6 demonstrated the highest growth rate in the tracked period, with 115% year-on-year sales growth during China’s Double 11 festival in 2024. This performance was entirely cross-border e-commerce driven, showing that Oli6 has built a strong direct digital relationship with Chinese consumers without relying on traditional import distribution. This model is capital-light and fast-moving, giving Oli6 flexibility that brands tied to physical retail cannot match at the same speed.

Danone brings global infant nutrition manufacturing scale and established regulatory expertise across multiple markets. As a major player with broad distribution infrastructure, Danone can serve the goat milk formula segment alongside its core portfolio without incurring the full market entry costs that smaller specialists face. Its challenge is that premium goat milk positioning requires a distinct brand story, and parent companies with wide portfolios must work harder to communicate the specific credibility that dedicated goat milk brands project by design.

Key Players

- AUSNUTRIA

- Little Bundle

- Danalac

- MT. CAPRA

- Oli6

- Formuland Inc.

- AoGoat Milk Infant Formulaoa Nutrients

- Nannycare Ltd.

- Orient EuroPharma Co., Ltd.

- Dairy Goat Co-operative (N.Z.) Limited

- Danone

- Bubs Organic, LLC.

- Kabrita

Recent Development

- In 2025 – Kabrita achieved nationwide US availability at Whole Foods Market and Sprouts Farmers Market, marking a major brick-and-mortar milestone for the brand’s US expansion strategy.

- In 2025 – Ausnutria reported goat milk infant formula revenue of RMB 1,865 Million, up 3.1% year-on-year, with China market share rising 2.8% to 30.4%.

- In 2025 – Kabrita became the first and only goat milk infant formula to achieve Clean Label Project’s First 1,000 Day Promise, Pesticide Free, and Purity certifications simultaneously.

- In 2025 – The FDA published a voluntary recall of Crecelac and Farmalac powdered goat milk infant formulas, removing non-compliant products and strengthening the position of certified brands.

- In 2025 – Oli6 goat milk infant formula achieved 115% year-on-year sales growth in China during the Double 11 festival, driven entirely by cross-border e-commerce performance.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 14.30 Billion |

| Forecast Revenue (2035) | USD 42.85 Billion |

| CAGR (2026-2035) | 11.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (First Class 0–6 Months, Second Class 6–12 Months, Third Class 1–3 Years), By Distribution Channel (Supermarkets and Hypermarkets, Retail Stores, Online Selling, Others), By Packaging Type (Bottle Packaging, Tetra Packaging) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | AUSNUTRIA, Little Bundle, Danalac, MT. CAPRA, Oli6, Formuland Inc., AoGoat Milk Infant Formulaoa Nutrients, Nannycare Ltd., Orient EuroPharma Co. Ltd., Dairy Goat Co-operative (N.Z.) Limited, Danone, Bubs Organic LLC., Kabrita |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |